The upcoming interim budget for FY25, to be presented on February 1, is expected to forgo major announcements, saving them for the full budget after the Lok Sabha elections. The government will likely maintain its fiscal correction & consolidation path, avoiding populist measures despite the general election. What is the interim budget? It is a partial budget presented to the current government which isn’t complete since general elections are around the corner. A full budget will be presented after the elections. So, let’s deep dive into the Interim budget for 2024 and see what we can expect the Finance Minister, Nirmala Sitharaman to present on 1st of February to the parliament. We will also look at the fiscal gap, India’s poor consumption issue, expected boost for defence and railways sectors and how budgets have impacted stock markets.

Fiscal Consolidation: A Key Theme For The Interim Budget

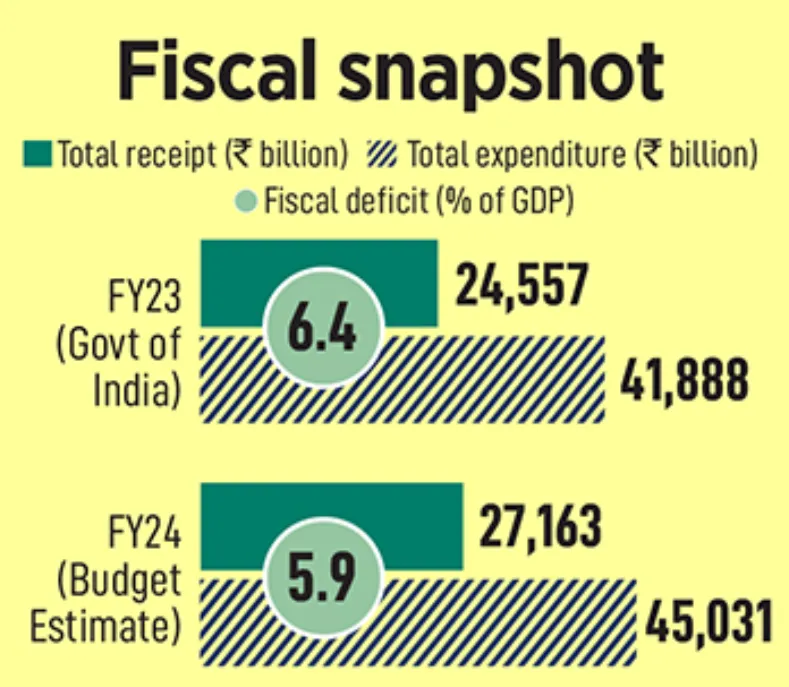

The Government of India is expected to maintain its fiscal consolidation trajectory in the upcoming interim budget to be presented on February 1, despite the approaching general elections. This commitment to fiscal prudence is reflected in the government's aim to reduce the fiscal deficit to 5.9% in FY24, as part of a broader strategy to narrow the gap to 5.3% and 4.5% in FY25 and FY26, respectively.

Despite potential pressures from election dynamics, financial analysts anticipate the government will meet its fiscal targets. Nirmala Sitharaman has indicated that the upcoming budget will be a vote on account, primarily focused on government expenditure until the post-election government is formed, precluding any major financial announcements.

Investors expect the budget to continue promoting investment-driven growth, with a projected 10% increase in capital expenditure, reaching Rs 10.2 lakh crore. This increase is more modest compared to the over 20% hikes observed in the last two years. The government's strategy emphasizes capital expenditure-led growth over expenditure cuts.

Attention is also likely to be given to the rural economy, which has not fully recovered. The government may implement measures to invigorate investment in rural areas and expand the scope of Production Linked Incentive (PLI) schemes, potentially benefiting sectors such as chemicals. This balanced approach between fiscal discipline and targeted spending is aimed at ensuring sustained economic growth while staying on the path of fiscal consolidation.

Looking At The Fiscal Gap

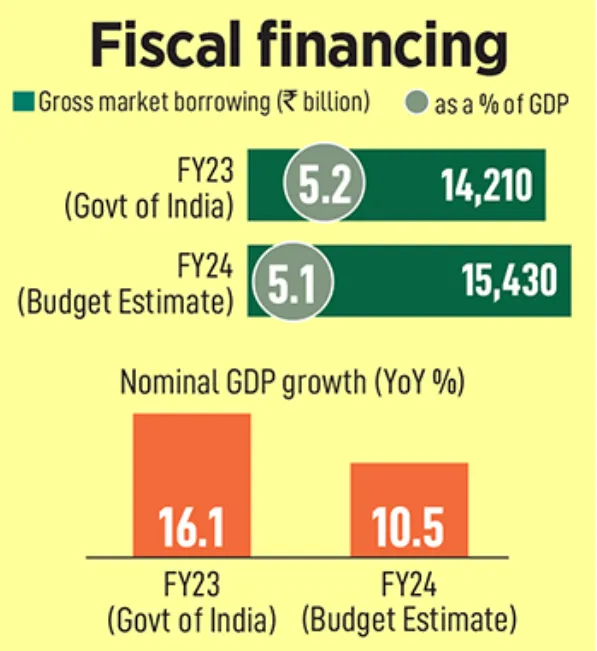

India's fiscal dynamics show a promising trend, with the government's coffers benefiting from higher than anticipated tax and non-tax revenues, including dividends from RBI and increased profitability of public sector undertakings. This influx of revenue is set to counterbalance the divestment proceeds' shortfall and the spike in subsidy bills and other revenue expenditures. The government appears to be on a solid path to meet its fiscal deficit targets of 5.9% for FY24 and 5.3% for FY25. Market estimates suggest that gross market borrowing will hold steady at approximately Rs 15.2 lakh crore in FY25.

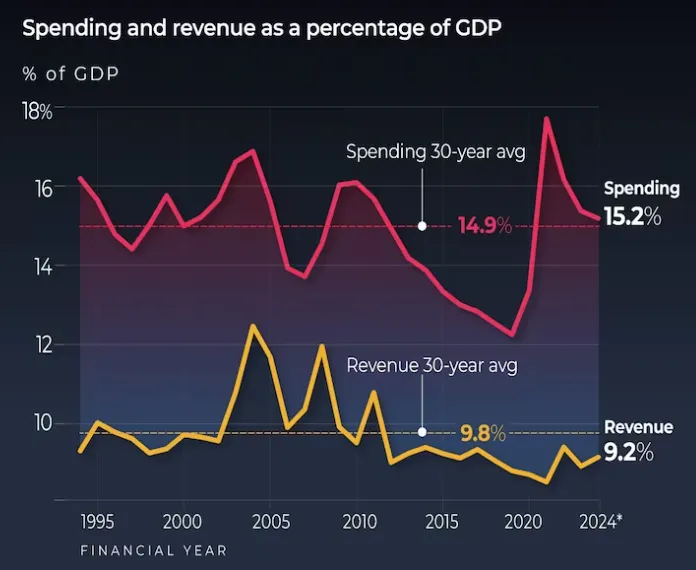

The anticipated revenue for this year is projected at 9.2% of the GDP, which is in line with the 30-year average of 9.8%. Meanwhile, expenditure is on a downtrend from the peak of 17.7% during the pandemic to a projected 15.2%, suggesting a recovery trajectory towards pre-pandemic levels.

The surge in tax revenues, which are currently 0.3% of GDP above the budgeted figures, is expected to cover increased subsidies and potential special packages that may be announced on budget day. Post-election, a normalization in current expenditure and a sustained high level of capital expenditure are anticipated.

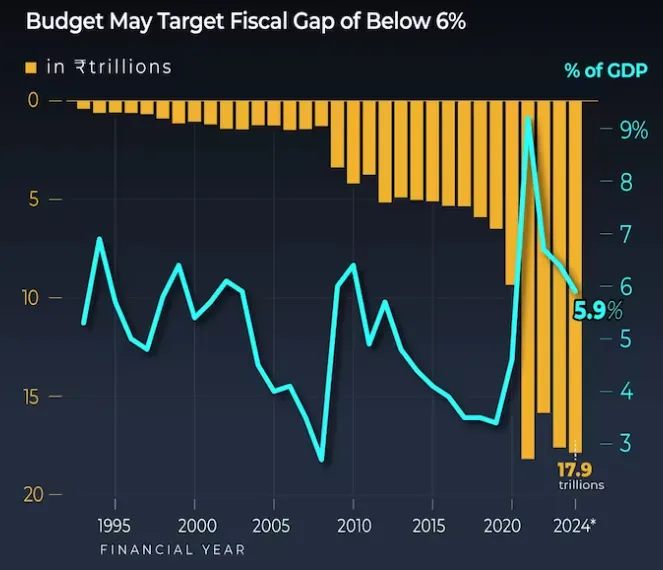

The fiscal deficit, a crucial indicator of fiscal health, has exhibited fluctuations, peaking at 9.2% in 2021. However, it is projected to contract to 5.9% by the FY24 budget estimate. This trend is indicative of a tactical approach to managing borrowing and recovery efforts. Despite lower-than-anticipated nominal GDP growth, the government is expected to meet its Rs 17.9 trillion fiscal deficit target for FY24, with the deficit reaching Rs 9.06 trillion by November 2023, which stands at 50.7% of the annual target.

How Does The Indian Government Finance The Fiscal Deficit?

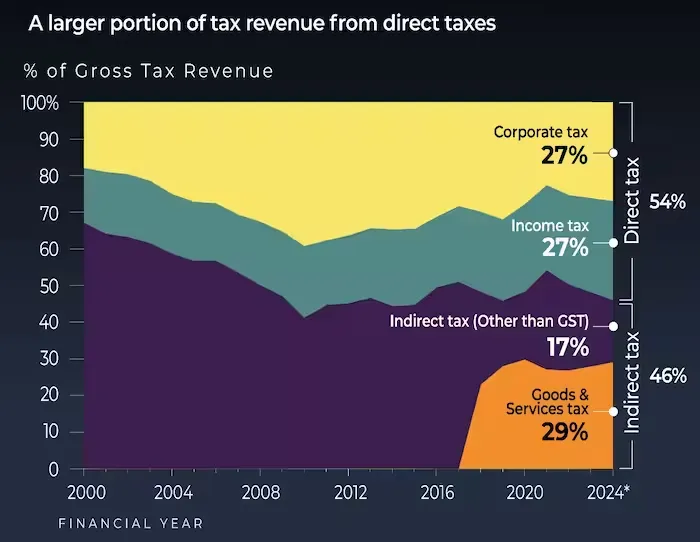

From April to November, the Indian government has used only 50.7% of the budgeted fiscal deficit for the current year, which is significantly less than the typical median usage of around 75%. This has been made possible largely by strong corporate and income tax collections, which have already reached 80% of the budgeted direct tax collection target of Rs 18.23 lakh crore.

India's GST collections have significantly exceeded expectations, with the FY24 monthly rate reaching Rs 1.66 lakh crore, a substantial increase from Rs 98,000 crore in FY19. This surge is anticipated to push Central GST collections beyond the budget estimate of Rs 8.1 lakh crore by approximately Rs 10,000 crore for the current fiscal year. Strong tax revenue has softened the blow from lower-than-projected excise and customs duties. Despite falling short of the divestment target by Rs 51,000 crore, this is consistent with a historical pattern where divestment proceeds typically do not meet budget estimates.

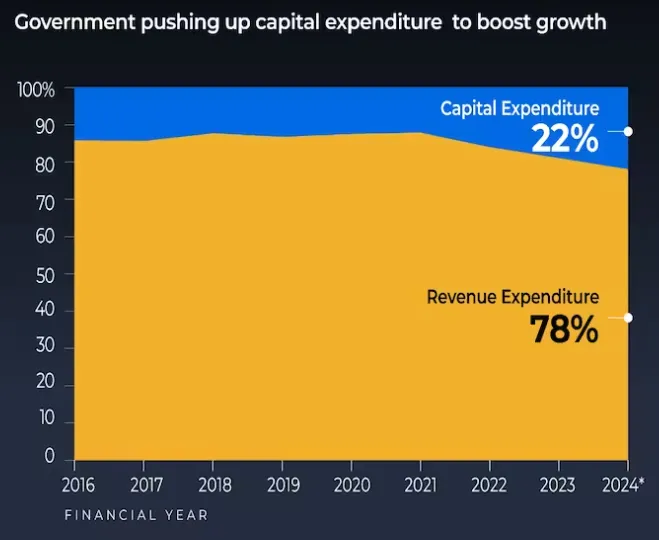

Analysts project that tax revenue will surpass expectations by Rs 69,300 crore, with non-tax revenue also exceeding by Rs 48,300 crore. However, spending has increased, notably due to a significant rise in interest expenses and subsidy bills. The latter has grown due to extended free grain programs and reduced cooking gas prices, contributing to a projected rise in subsidy expenditures to Rs 4.25 lakh crore in FY25. Capital expenditure, which accounts for 15% of total spending, has been instrumental in India's fiscal strategy. It has increased from 1.6% of GDP in FY21 to 2.8% in FY24, demonstrating the government's commitment to capital expenditure-driven growth.

Market borrowings have been the principal method of financing around 65% of the fiscal deficit over the last decade. It is important for the government to roll back pandemic-era stimulus measures, especially given India's high public debt relative to other emerging markets and the increased international focus on Indian bonds. India's public debt has escalated from just over 51% of GDP in FY20 to over 80%, presenting a challenge for fiscal consolidation.

What To Expect From The Interim Budget 2024?

The scale of the Union Budget relative to India's GDP saw an expansion during the pandemic, a time characterized by the government's efforts to clear subsidy dues and enhance fiscal transparency. However, the trend is reversing, and the budget for FY24 is set to contract to 14.9% of GDP. This reduction signifies a deliberate move towards pre-pandemic fiscal patterns, reflecting the government's strategic withdrawal from the expansive fiscal stance necessitated by the pandemic's economic disruptions. This shift towards a smaller budget proportionate to GDP aligns with the broader objectives of fiscal consolidation and sustainable economic management.

In the fiscal year 2023, India experienced a significant post-pandemic economic recovery, with the tax-to-GDP ratio reaching 11.1%, surpassing the pre-pandemic figure of 10.9% in FY19. Despite this recovery, forecasts suggest that this ratio will stabilize and is not expected to surpass the FY18 peak of 11.3% in FY24. The Union Budget's proportion to GDP expanded during the pandemic due to subsidy dues clearance and increased fiscal transparency. However, it's now contracting, with the 2024 Budget estimated at 14.9% of GDP, signalling a return to pre-pandemic norms.

Central tax collections have shown remarkable growth, surging by 33.7% in FY22 and revised upwards by 10.3% for FY23. However, this rapid growth is showing signs of slowing down, indicated by a reduction in tax buoyancy and a drop in non-tax receipts. These trends point towards a possible recalibration of India's fiscal strategy, emphasizing sustainable growth over short-term gains.

On the expenditure side, the government's strategy is increasingly focused on capital expenditure. There's a planned 37% increase to Rs 10 trillion in FY24 for capital expenditure, reflecting the government's intent to bolster long-term asset creation over immediate revenue expenditure, which has seen only a modest rise.

According to the Controller General of Accounts, as of November 2023, the Centre has spent Rs 26.52 trillion, which is 58.9% of the budget estimate for FY24, allocating Rs 20.66 trillion for revenue and Rs 5.85 trillion for capital expenditures. This budget allocation underscores the government's commitment to enhancing the country's infrastructure and productive capacity to foster economic growth and stability.

More Food Subsidies Amid Rising MSP Costs

India's interim Budget for 2024-25 is set to increase food subsidies to Rs 2.2 trillion, a 10% hike from this year. The rise accommodates a 7% increase in the wheat MSP (minimum support price) and upcoming hikes in paddy MSP. Food Corporation of India provides 5kg of free grains to 801 million beneficiaries amounting to over 55 million tonnes of wheat and rice. The shift to a completely free grain supply as of January 2023 has led to a 3-4% increase in costs. The food subsidy bill surged in FY22 and FY23 due to a scheme that amplified the provision of subsidized food grains, which has since been discontinued.

The FCI anticipates food security expenses of Rs 1.55 trillion for FY25, up from Rs 1.36 trillion for the current fiscal year. An additional Rs 65,000 crore is expected to be allocated to states with decentralized procurement systems. With the extension of PMGKAY for five years until 2028, the scheme is projected to cost the exchequer about Rs 11.8 trillion, considering an annual 7-8% increase in MSP for key crops, as well as other expenses like transportation and storage. So far, the finance ministry has disbursed Rs 0.96 trillion for food subsidy expenses to the FCI in the current fiscal, which channels 70% of the subsidy funds. Notably, for the first time in many years, the FCI has operated without short-term credit for its operational expenses due to the timely release of subsidy funds.

How Can the Indian Government Boost Private Consumption?

Private consumption, a crucial component of India's economy, accounted for 57% of the GDP in 2023-24. However, growth in private final consumption expenditure is anticipated to drop to a three-year low of 4.4% this year from 7.5% last year, indicating uneven recovery post-pandemic. There's potential for recovery, especially as the gap between rural and urban demand narrows. Factors such as decreasing inflation, improved rural terms of trade, and better labor demand conditions could bolster private consumption. But so far, a 'K-shaped' recovery aptly describes this, where demand for premium goods by the upper class surpasses that of the mass-market segment.

Retail & FMCG Sectors Under Stress

Retail consumption has been showing signs of stress. India's leading retailers have cut down on store expansions in FY24, opening 44% fewer stores compared to the previous year, as they shift focus to profitability amid subdued consumption, particularly in the rural and mass segments. The retail sector makes up about 10% of GDP. Despite its potential to reach $2 trillion by 2032, the sector is witnessing reduced spending in the mass market, evident during recent festive and wedding seasons. Inflation has particularly hit rural and semi-urban areas, dampening demand for traditional wedding purchases like jewelry and appliances.

Consumption in smaller towns and rural areas has been declining for the past six to eight quarters. While premium product sales continue among the wealthier demographics, overall retail sales grew only by 7% in October and November 2023, even during the festive season. Lifestyle and apparel demand remains low despite significant discounts, and the FMCG sector, indicative of rural economic health, is also experiencing a demand slump. Rural challenges are compounded by factors such as high unemployment, demand for NREGS jobs, and alternative spending avenues, contributing to the sluggish FMCG market growth.

Can the Budget Help Boost Private Consumption?

To address the retail sector's slowdown, tax concessions could invigorate consumer sentiment and spur spending. Reducing taxes could enhance disposable income, thereby boosting retail consumption. The budget can balance investment incentives with measures that encourage consumer spending, particularly in rural areas. Job creation initiatives could vitalize the consumption-driven economy, which is essential for sustained, inclusive growth.

The government could consider tax cuts or expand cash-disbursing schemes to increase spending, especially at the lower income spectrum. Another potential measure is to lower excise duty on petrol and diesel, which would have a broad consumption-stimulating effect due to the inelastic demand for fuel. A fuel tax cut could significantly raise disposable income, as even households without private vehicles are affected by public transport costs.

Given the pressing issue of subdued consumption, it is anticipated that the government will incorporate solutions into the interim budget, rather than postponing action until the full budget post elections. Such fiscal interventions could be a decisive step toward reinvigorating the market and addressing the challenges faced by the FMCG sector and the broader economy.

Why Is Consumption Important For India?

India’s private consumption is projected to match China’s 2022 nominal consumption by FY34, reaching $12 trillion, or 67.7% of China's 2022 nominal GDP. The shift towards discretionary spending could accelerate if income growth outpaces current trends.

Discretionary consumption in India is expected to triple to $2 trillion by 2030, according to Barclays, with private consumption forming a larger portion of the economy (58%) than in many large consumer-led economies. India's demographic trends, particularly the growth in the 25-45 age group, further enhance its consumption potential.

However, this consumption growth is not without risks. Barclays warns of potential macroeconomic stability issues and emphasizes the need for a balance, such as increasing exports and growing domestic manufacturing. For instance, higher exports can offset import growth, maintaining macroeconomic stability. Improving domestic financing to support manufacturing expansion is also crucial. A marginal drop in consumption propensity could notably impact the savings pool.

Major Boost Anticipated for Railways and Defense Sectors

Similar to the previous budget, the government’s focus on infrastructure, railways and defense sectors is likely to be strong. For railways, a substantial increase in capital expenditure is projected, likely over 20%, primarily driven by expansions in Dedicated Freight Corridor, rolling stock, and High-Speed Rail networks as outlined in the National Rail Plan. In railways, the emphasis is expected to shift towards new initiatives such as rolling stock enhancement, safety measures, and new track laying. This focus marks a shift from the previous decade’s emphasis on electrification. The sector is also likely to see increased private sector participation in comparison to past trends.

The defense sector is also set to see a rise in capital outlay with stock market experts anticipating a 12-15% year-on-year growth with a focus on R&D, UAV/drones, and anti-drone systems. The increase is partly due to ongoing major system projects, with a positive medium to long-term outlook anticipated due to continued government orders.

Interested in learning more about the Railways & Defense sectors? Read our Complete Guide to Indian Railway Sector and Top Railway Stocks in India 2024 & Best Defence Stocks to Buy in India Today

India's Sovereign Bonds Attract Global Interest Ahead of Index Inclusion

Global funds are increasingly investing in India's sovereign bonds, spurred by the country's upcoming addition to global debt indexes. This trend is bolstering demand for the near-record government borrowing anticipated in the coming fiscal year. According to a Bloomberg report, India is expected to aim for a gross borrowing of about $183 billion for the fiscal year starting April 1, slightly lower than the current fiscal's 15.43 trillion rupees. The surge in interest from global funds, exceeding 500 billion rupees, has followed JPMorgan announcement in September to include India in its benchmark emerging-market index.

Currently, foreigners own about 2% of India's sovereign debt market. The official inclusion of Indian government bonds in JPMorgan's index is set for June, and Bloomberg Index Services is also considering adding the debt to its EM bond index from September. Economists, including those from Standard Chartered, anticipate that foreign investor inflows of $20 billion will significantly impact the demand dynamics for FY25. These inflows are expected to pick up pace once the inclusion becomes effective in June. This increase in demand for government debt is timely, especially considering the Reserve Bank of India's high-interest rate policy.

Impact Of Budget On Stock Markets

As India anticipates relief on the tax front against the backdrop of high inflation and the 2024 general elections, expectations are for the Budget to sustain its course towards a $5 trillion economy with little deviation from fiscal targets. Historical analysis indicates that the markets have often reacted negatively on Budget day and one month post-announcement, with losses recorded six times in the last decade. The market reactions have been moderate on Budget day, with 8 out of 10 years showing gains or losses within 2%. Similarly, one-month post-Budget movements have been within 6% for 7 out of the last 10 years.

2013: The market dipped by around 2% on Budget day, marking the poorest performance since 2009.

2014: With a new government in power, the market saw a slight 0.2% dip on Budget day.

2015: The Budget led to a 0.7% gain, followed by a 4.6% drop in the following month.

2016: Despite a 0.6% Budget day loss, the Nifty soared by over 10% the following month, the highest since 2011.

2017: Shifting the Budget presentation to February 1, the Nifty gained 1.8% on the day, the best performance of the decade.

2018: Post-GST implementation, the Nifty fell 0.2% on Budget day and 6% over the next month.

2019: Nirmala Sitharaman's first Budget saw a 1.1% loss on the day and an 8% drop in the following month.

2020: The market responded negatively again, with a 2.5% decline on Budget day.

2021: The Budget received a strong positive response, with a 4.7% gain, the highest since 1999.

2022: A 1.4% rise on Budget day was followed by a 4.5% decrease in the next month.

Join Our Youtube Channel

Join our Telegram Channel to get daily morning market updates. Subscribe to our Youtube Channel to learn about all things investing, understand sector performance, get key insights into new topics like concentrated portfolio, quantitative investing and more!

Other interesting articles to explore:

- Union Budget 2024 Impact on Stock Market

- Budget 2024: Indian Economy Growth With Government Interventions

- How Does The Budget Impact Your Equity Investing Strategy? Capital Gain Changes & Sector Analysis

- Top Sectors to Invest in After the Interim Budget

- Q3 Earnings - How Are Indian Companies Performing? What To Expect From Different Sectors

- Interest Rate Cut Expectations In 2024 For India How To Maximize Returns Based On Your Diversification Ratio? Looking at Large Caps, Mid Caps & Small Caps

- Stock Market Predictions For 2024

- 2023 Recap: Indian Stock Market Performance, Indian Economy & Wright Portfolios Performance in 2023

- Four Years of Wright Momentum: Mastering the Art of Building a Successful Momentum Strategy

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox