by Sonam Srivastava, Akashdeep Bhateja

Published On Sept. 2, 2023

"Compounding is the 8th wonder of the world" and we do hear about it more than enough in financial publications. But compounding your wealth consistently is the only answer if you want to realise your dreams of financial freedom.

How do you make a winning portfolio that can grow your wealth consistently and at low risk? We find the answer to this question in multi factor strategies. Let's dig into some financial data as we answer this.

When constructing a portfolio, careful considerations are needed for various factors to achieve balance between risk and return. Let’s have a look at them.

One must define their goals for investments. They can be capital appreciation, income generation, wealth preservation. Defining an objective is important because it will guide select assets accordingly. Capital appreciation is an aggressive growth approach, you invest more in stocks with higher returns even when they come at higher volatility. For short-term goals, a bigger portion might be put into stable assets like high-quality bonds and cash equivalents.

The assets in a higher-risk portfolio tend to be riskier, while a lower-risk portfolio might have more conservative choices. The main goal of a modest risk profile is to protect capital, so its assets are a mix of both risky and safe stocks.

Spread your investments across different assets within each asset class, sectors, industries, and geographical areas. Diversification can help lower risk by keeping you from spending too much money on any purchase.

You should consider how long you want to keep your investments. When you have a shorter time horizon, you need to make more stable decisions than when you have a longer time horizon, which usually gives you more room to take risks and grow.

Market conditions influence asset allocation decisions. For example, buyers might put more money into stocks when the market is going up. They might put more money into bonds or cash when the market is going down. Risk management is based on making changes to asset allocation based on how the market is doing.

Every investment has costs. Taxes can sting the most out of all the expenses and take the biggest bite out of your returns. Different investment types generate varying tax consequences, so make sure your investments are tax-efficient, especially in tax-advantaged accounts like IRAs

Other things to consider are costs, fees, cash needs, etc. Putting together a portfolio is a personal process, and the best portfolio for one person might not work for another. Make sure your investment choices fit your needs and goals, and check in on your portfolio often and make changes as needed to stay on track with your finances.

Factor investing , which is also called smart beta or factor-based investing, is the process of putting together investment portfolios that focus on certain factors that have historically been linked to better returns or lower risk. These factors have a long-term effect on results that goes beyond what traditional market beta can explain. The figure shows some common strategies that investors use to build their portfolios.

Investing choices are often made based on these strategies. For example, keeping track of a company's finances, such as its debt level, revenue growth, etc., or using ratios like the P/E or P/B ratios. There are many other investing strategies, like low-volatility strategies, which focus on buying assets whose prices have been less volatile in the past. Small-cap factor strategy is a way to invest in smaller companies with lower market value, which tend to do better over the long term than large-cap stocks because they have more room to grow.

When using factor investing strategies , it's important to think about your financial goals, how comfortable you are with risk, and how long you want to invest for. Factor-based portfolios can help increase returns and lower risk, but they can also fail when certain factors aren't popular. Also, you need to do a lot of study and analysis to make sure that the factors you choose match your investment goals and beliefs about the market.

In the previous sections, we talked about the most important things to think about when building a portfolio and the different ways to build a portfolio using factor investing. Now, let's talk about how factor investing can be used to put together a stock portfolio.

Using factor investing to build a stock portfolio requires a methodical approach based on a clear understanding of your financial goals, factor selection, and a disciplined process for building the portfolio. If you follow these steps and keep an eye out, you can use factor-based methods to help you reach your financial goals. Investing in factors may take time but can pay off big in the long run.

The answer is no. In the last decade, even with a couple of major bull markets, the large cap equity index would have given you a CAGR of less than 10%, bonds and gold would have given you a much lower return and mid caps would have given the highest 12% CAGR.

FMCG, Financial Services & Banks have given almost 15% returns in the last decade but the single sector strategies are quite high risk and prone to drawdowns.

We hear so many success stories from great small & medium cap stock pickers who pick up mutli-baggers. We know expert trend followers who ride the bull wave and deliver exemplary returns. We know proponents of quality stock picking who have delivered consistent compounding. There are many such themes or factors that out-perform passive strategies.

As a quant researcher, I look at these unique ways of investing as "factor based" investing strategies. Any portfolio's performance can be largely explained using well known themes. Any portfolio has its outperformance coming from one or more of these factors - growth, quality, value, momentum , low volatility, dividend yield, small cap premium etc.

This is not something that is unheard of. NSE publishes well known indices based on these themes since the last few years and they are increasingly gaining popularity in India.

At Wright Research we do not use the NSE indices but create our own factor portfolios on these themes. So strictly based on our models (which have a proprietary element) the factor portfolios have given up to 20% returns in the last decade, with momentum, quality & low volatility factors leading the pack.

No they do not. While there are times like the recent past when there is no stopping the momentum factor, we have seen times when the low volatility, dividend yield or even value factor has out performed the momentum factor.

So our answer to growing your wealth consistently year on year is to have a tactical combination of factors as your investing strategy. If you can define rules that help invest in the appropriate factor at the appropriate times you can reach your wealth goals!

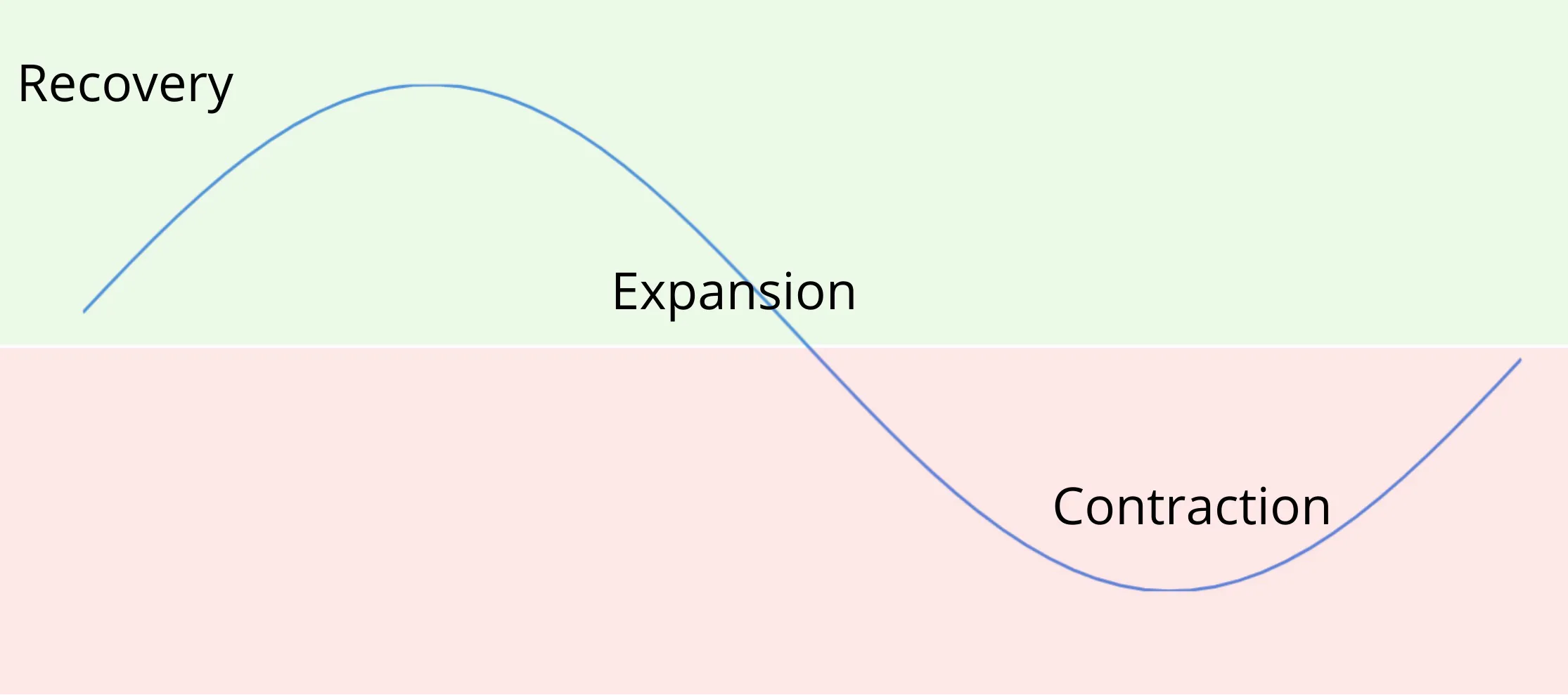

Markets and the economy go through phases. The business cycle, which reflects the fluctuations of activity in an economy, can be a critical determinant of equity sector performance over the intermediate term. The performance of economically sensitive assets such as stocks tends to be the strongest during the early phase of the business cycle when growth is rising at an accelerating rate, then moderates through the other phases until returns generally decline during a recession.

Just as we see cyclical and defensive sectors give performance sensitive to the business cycle, factor performances are also heavily dependent on market cycles. In an accelerating growth phase Momentum or Size factors outperform while in a slow growth phase quality stocks outperform. In a late phase of the cycle it might be prudent to focus on low volatility while in a recessionary phase asset allocation instead of factor allocation might come to the rescue!

At Wright Research, we research and forecast the business cycle and give the portfolio recommendation based on a tactical combination of factors. We rebalance our 20-25 stock portfolio monthly and keep our turnover low while being dynamic in our factor choices.

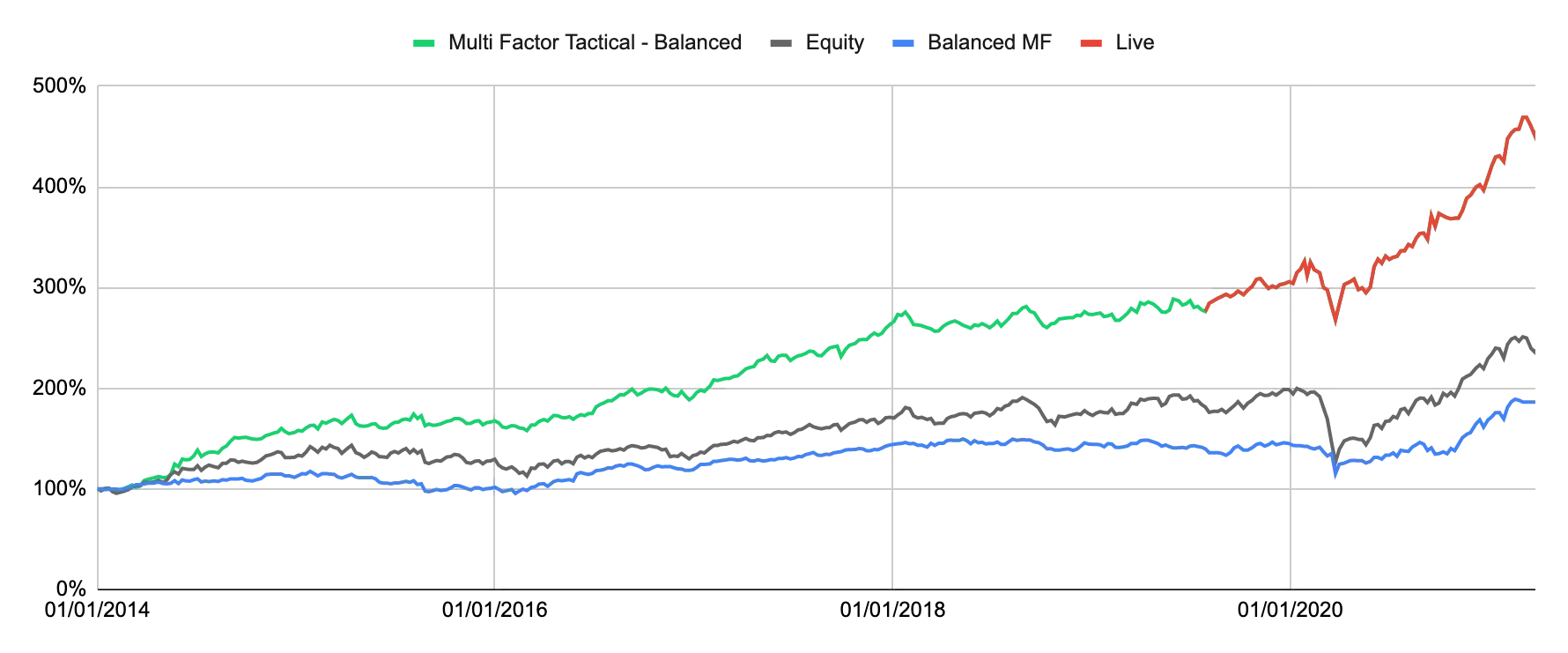

Our multi factor approach outperforms all single factor portfolios listed on the NSE

Our multi factor strategy has been running live for for over 4 years now years. We have given a compounded annual growth rate of 37.2% during our time live at a risk of 13.8% and a drawdown of only 18% when the market went down almost 40%.

Here are the key performance metrics of the Balanced Portfolio against its benchmark, the Multicap Index -

Our multi factor portfolio has been outperforming the index continually and consistently over the last 4 years. The latest performance numbers of our featured Balanced Multi Factor stack like this:

Over a 3 year horizon, ₹1 Lac invested would have become -

Here's the performance of the Balanced Multifactor portfolio across different periods -

Our performance is purely led by factor modelling and tactical factor selection using regime modelling. Our strategy is transparent, explainable and most importantly consistent. Factor investing is based on decades of research and has a very sound mathematical basis. We aim to use our focused research to identify and utilise India specific factors that can deliver a diversified and consistent outperformance for our investors.Explore the Balanced Multifactor Smallcase & Momentum Smallcase.

Check out the Complete guide to Factor Investing & Wright Balanced Multifactor Portfolio.

1. What is factor investing, and how can it help in building a winning portfolio?

Factor investing targets specific factors like growth or value that have historically produced higher returns. At Wright Research, we use a multi-factor approach to optimize performance.

2. How do I start building an investment portfolio from scratch?

Start by defining your investment goals, assessing your risk tolerance, and diversifying your assets. Keep track of market conditions and tax implications to adapt your strategy.

3. What are the key factors to consider in portfolio management?

Key factors include investment goals, risk tolerance, diversification, time horizon, market conditions, and tax implications.

4. Can factor investing be applied to stock portfolio construction?

Yes, you can build a stock portfolio focused on specific factors like growth, value, or low volatility, aligned with your investment goals.

5. Are there specific factors to consider when selecting stocks for a factor investing portfolio?

Look for stocks that align with the factors you've chosen, such as those exhibiting strong growth, value, or low volatility. At Wright Research, we tailor factor selection to business cycles for optimal performance.

Written by Sonam Srivastava, Akashdeep Bhateja

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart