Factor investing is an investment technique where securities are chosen based on specific attributes that have been identified as key drivers of returns. To put it in simple terms, consider an investor who chooses stocks that are undervalued; in this case, they are investing based on 'value' as a factor.

Think back to the days when planning a vacation was a chore, involving lengthy phone calls with travel agents and patiently awaiting their arrangements. Plus, they charged hefty fees since they were the gatekeepers to crucial booking information. Nowadays, this information is readily available to anyone instantly. Travel platforms have streamlined the process of finding ideal accommodations and flights, making it quicker, cost-effective, and efficient.

Just as the travel industry has evolved, advances in technology have reduced the investment costs for individuals. For years, active fund managers employed analysts to identify stocks with high potential for better performance. As an investor, this expertise came at a premium. These active managers often aimed for higher performance by concentrating on securities that displayed specific traits, such as superior quality earnings, reduced volatility, or stocks that seemed undervalued compared to their fundamental data. In-depth research over the years has identified certain characteristics that help in predicting differences in expected returns. Factor Investing is an investment style that leverages these traits to build efficient and affordable portfolios.

What are the different types of factors?

Factor investing is an approach that targets securities with distinct attributes such as value, quality, momentum, size, and minimum volatility. These traits, known as factors, are enduring and well-studied features that help investors decipher variations in anticipated returns. Professional investors have used factors as a means to strive for better performance for a long time, and with the advent of Exchange Traded Funds (ETFs), Robo advisory, Quantitative strategies these factor strategies are now accessible to all investors.

There are two main categories of factors: Macroeconomic and Style factors. Macroeconomic factors, although not directly connected to financial assets, can significantly impact their prices. These can include elements such as GDP growth, interest rates, and inflation.

On the contrary, Style factors are directly related to the risks and returns within the asset classes and include attributes such as value, quality, size, momentum, and others. For instance, momentum is a single factor often used in portfolio construction, resulting in many funds being based on this single factor or others like value or quality. Click here to learn more about the different types of investing factors .

Factor | Objective |

Value | Invests in stocks that are lower cost relative to their peers |

Quality | Invests in companies with strong financials relative to similar cost peers |

Momentum | Invests in stocks that are outperforming and reduce exposure to stocks that are underperforming |

Size | Invest in smaller, and more nimble companies |

Minimum Volatility | Invest in stocks that collectively have lower volatility than the broad market |

What is Multi-factor investing?

Multi-factor investing is another concept, a perfect example of where an investing strategy uses multiple factors instead of focusing on a single factor. For instance, a fund based on smallcaps, value and low volatility is a multi-factor investing strategy. Such a fund would only include smallcap stocks that are undervalued and exhibit lower price variations over time.

The factor investing approach uses these identified attributes to create cost-effective and efficient portfolios. Wright Research, for instance, relies on five factors among others — value, quality, momentum, size, and minimum volatility — that have consistently demonstrated resilience across different periods, markets, and asset classes, backed by a solid economic rationale.

When did factor investing start?

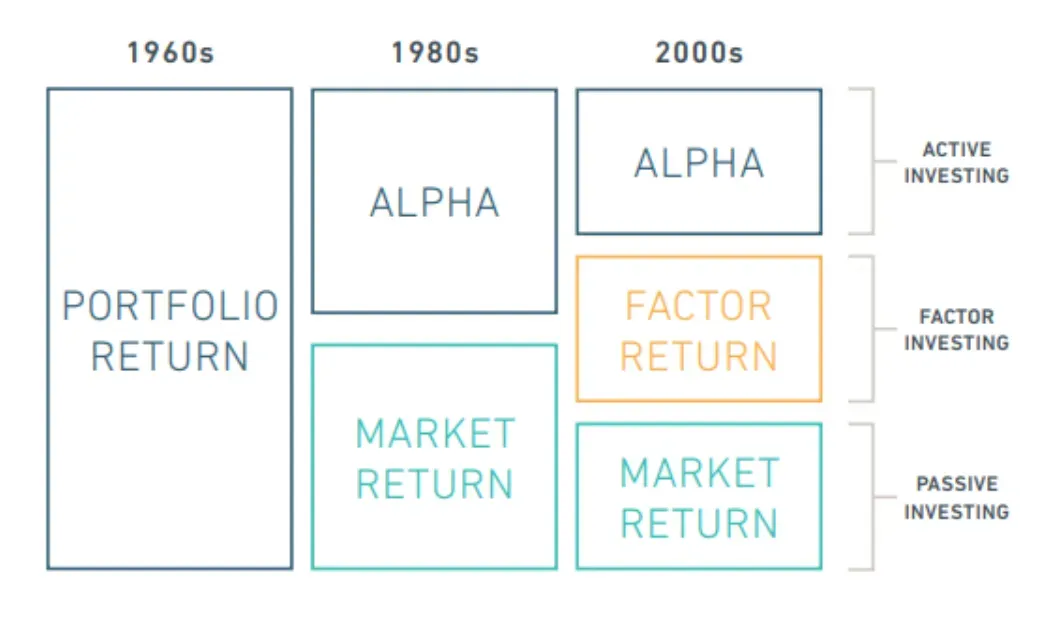

The roots of factor investing can be traced back to the 1960s with the introduction of the Capital Asset Pricing Model (CAPM), which proposed that the expected return of a stock is tied to its beta or correlation with the overall stock market. The factor investing concept underwent further development in the 1970s, evolving from the Efficient Market Hypothesis (EMH). This hypothesis suggested that market prices are always fair since all investors have access to the same information, react instantly, and behave rationally. However, in practice, there are significant discrepancies in information access and timing, coupled with occasional irrational behavior among investors. This indicates that markets don't always operate efficiently, particularly during periods of heightened fear or greed among investors.

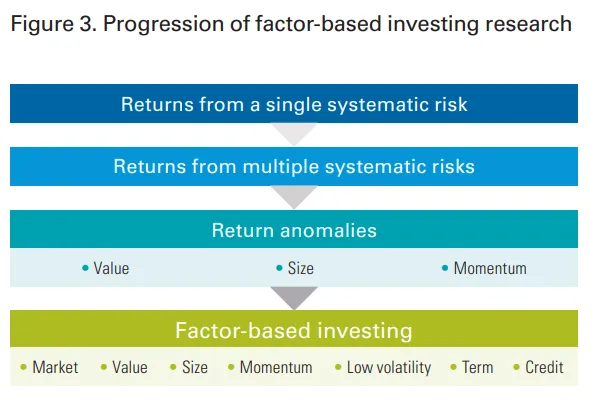

However, it started drawing the attention of institutional investors primarily in the 1990s. Its popularity surged after the release of a pivotal 1992 paper by scholars Eugene Fama and Kenneth French, who suggested a three-factor model to account for stock returns. This model posited that three distinct elements – size, value, and market risk – can justify the variations in stock returns over specific periods. Their studies exhibited that stock portfolios leaning more towards small cap and value companies exceeded market performance in the long run.

This discovery underscored the limitations of the Capital Asset Pricing Model (CAPM), particularly highlighting that market risk or beta is not the sole risk factor elucidating the differences in returns over time. They found out that market beta could only account for approximately 67% of the differences in portfolio returns. However, the inclusion of size and value factors along with market risk in their model led to an explanation of nearly 90% of the differences in returns between diversified portfolios.

The groundwork for factor theory, laid in the 1970s & followed by Fama-French in 1990s, saw a significant breakthrough in 2009 with the release of the "Evaluation of Active Management of the Norwegian Government Pension Fund - Global Report". This report aimed to explain the slump in wealth fund performances during the 2008 financial crisis. Consequently, an increasing number of investors are adopting factor investing strategies for a more systematic approach to their portfolio allocation and security selection.

Who were the pioneers of Factor Investing?

The concept of factor investing has evolved over time, thanks to the contributions of multiple academics. Yet, the credit for factor investing typically goes to Eugene Fama and Kenneth French. Their innovative three-factor model for stock returns, proposed in the early 1990s, set the stage for further explorations into factor investing.

Post the 1992 discovery, more factors beyond the traditional Fama French three-factor model have been recognized.

In 1997, Mark Carhart introduced the factor of "momentum", which is widely acknowledged today as a factor resulting in higher expected returns over an extended period.

In 2012, Robert Novi Marks proposed "profitability" as another determinant of returns. This addition led to a five-factor model, which collectively could explain over 95% of the differences in returns between diversified portfolios.

In 2014, Fama and French presented their own five-factor model, including market risk, size, relative price, profitability, and investment as the five factors that account for differences in returns, while omitting momentum. They disregarded momentum mainly due to its demand for high turnover strategy and associated costs.

Their advanced five-factor model revealed that almost 100% of the differences in returns between stocks and diversified portfolios could be explained based on their sensitivities to these five independent risk factors. This revelation was a blow to many active managers who had proclaimed to generate "alpha" in portfolios by favoring more small-cap and value stocks. Now, any investor could replicate this strategy independently and generate the same alpha without incurring hefty manager fees.

Read about the different types of investing factors .

Invest in Wright Research's Balanced Multifactor portfolio.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox