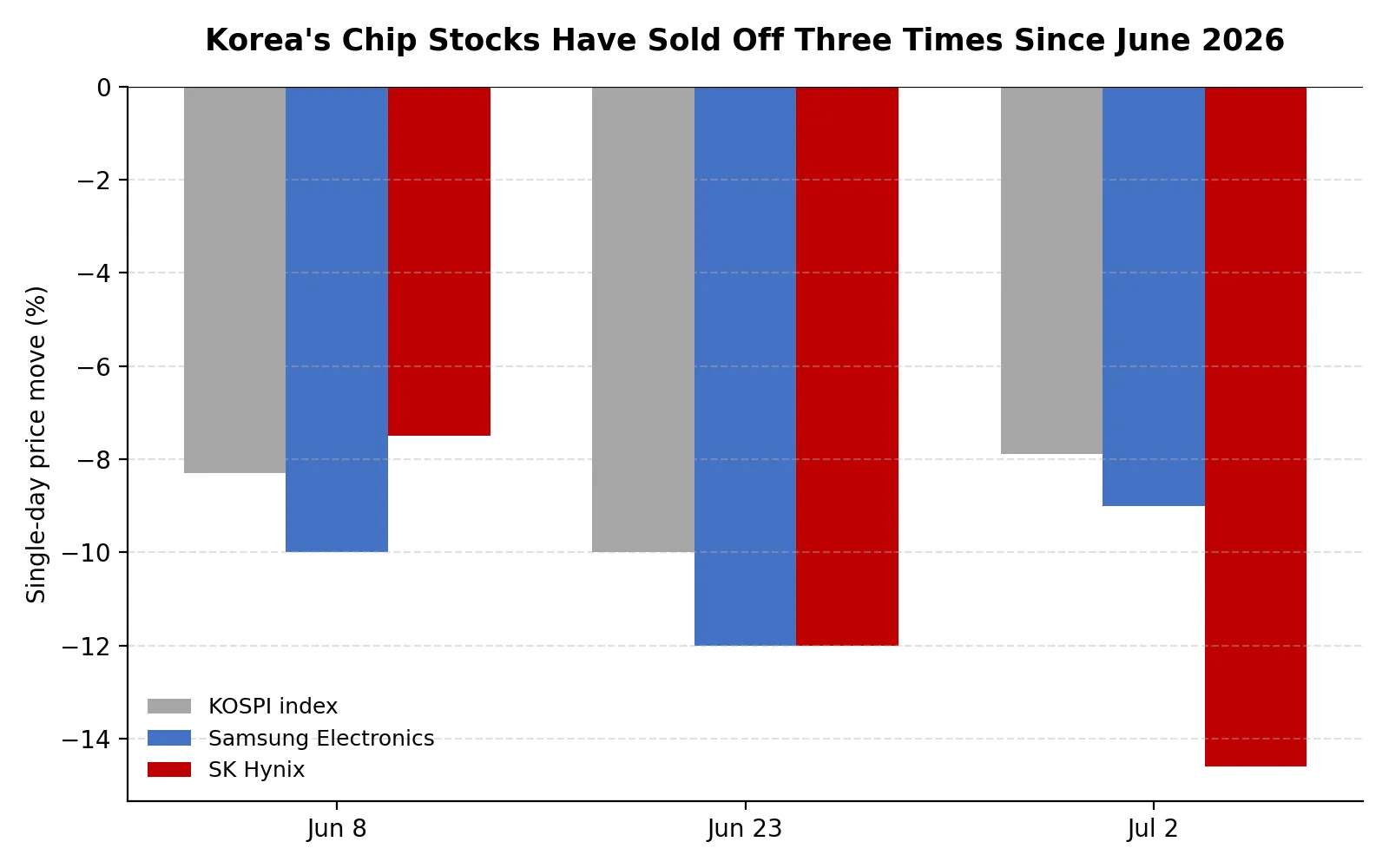

Semiconductor & Chip stocks have sold off three separate times since early June 2026, each one centered on Korea. On June 8, the KOSPI fell as much as 9% intraday and triggered a circuit breaker, with Samsung Electronics down over 10% and SK Hynix down 7 to 8%. On June 22 and 23, the index fell again, closing down 10% with Samsung and SK Hynix both off more than 12%, forcing a 20-minute trading suspension. On July 1 and 2, it happened a third time: the KOSPI dropped 7.89%, SK Hynix fell 14.6%, Samsung fell 9%, and the two companies lost a combined USD 290 billion in value in a single session, according to Bloomberg.

Single-day price moves on the three sell-off dates.

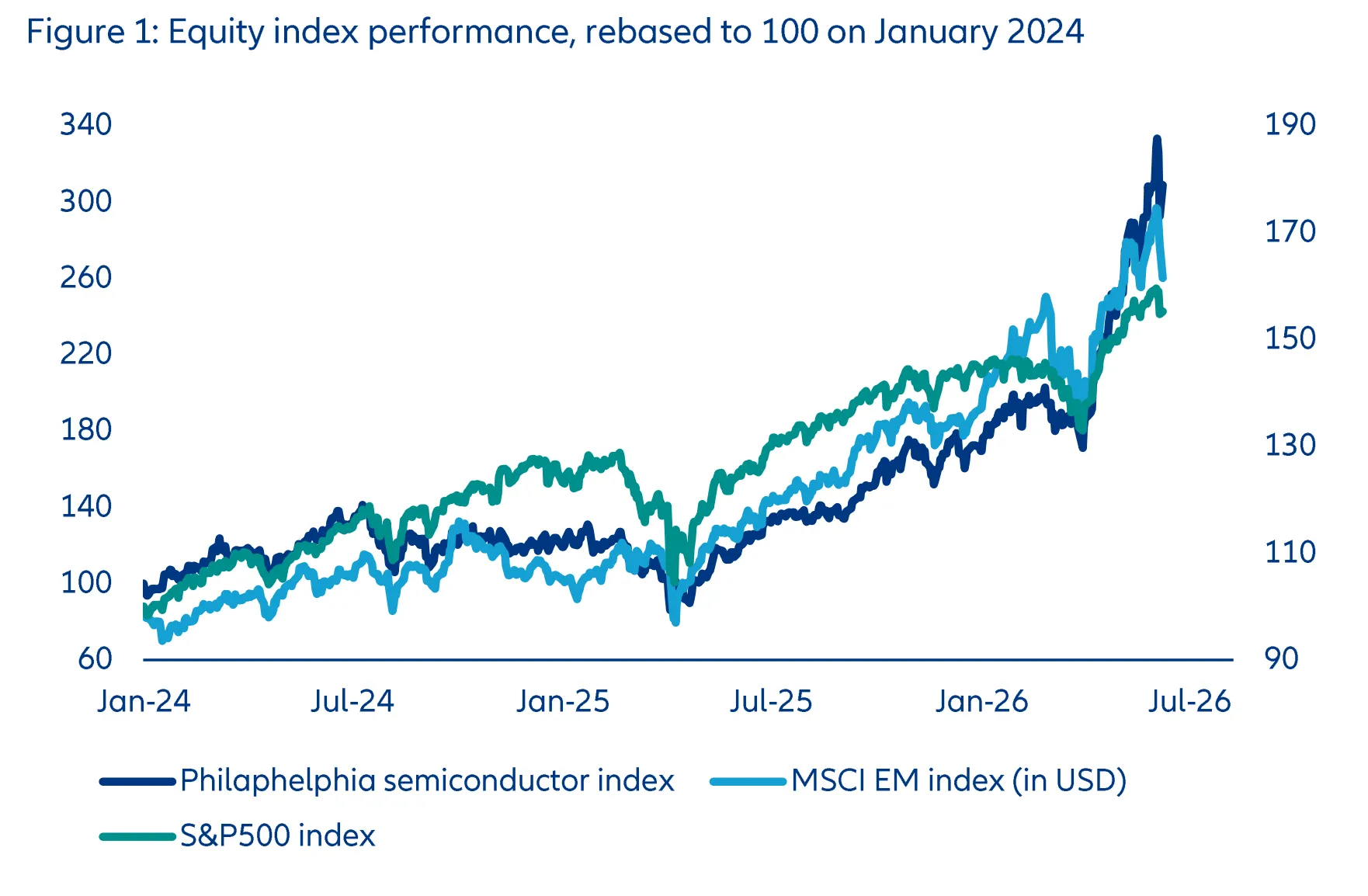

Each Korean drop coincided with weakness elsewhere. Taiwan's TSMC fell between 3.5% and 6.6% on separate days in late June, dragging the Taiex down more than 1,000 points on one occasion, since TSMC alone accounts for over 40% of that exchange's market value. In the US, the Philadelphia Semiconductor Index fell 7.87% in a single session, and Micron, Intel, and Marvell all dropped more than 7% in premarket trading around the same period. Europe's Stoxx 600 Technology index fell 3%, with STMicroelectronics and ASMI both down more than 7%.

None of this erased the year's gains. The KOSPI remained, by most accounts, the world's best-performing major index through the first half of 2026, and the SOX had still more than doubled for the year even after the pullbacks. Data taken before the sharpest of the three drops, already showed the same pattern: a 12% correction that still left the sector up 82% for the year. Every measurement point shows sharp, repeated drops layered on top of an extraordinary rally, not a sustained decline.

Why Did Korea Take the Biggest Hit?

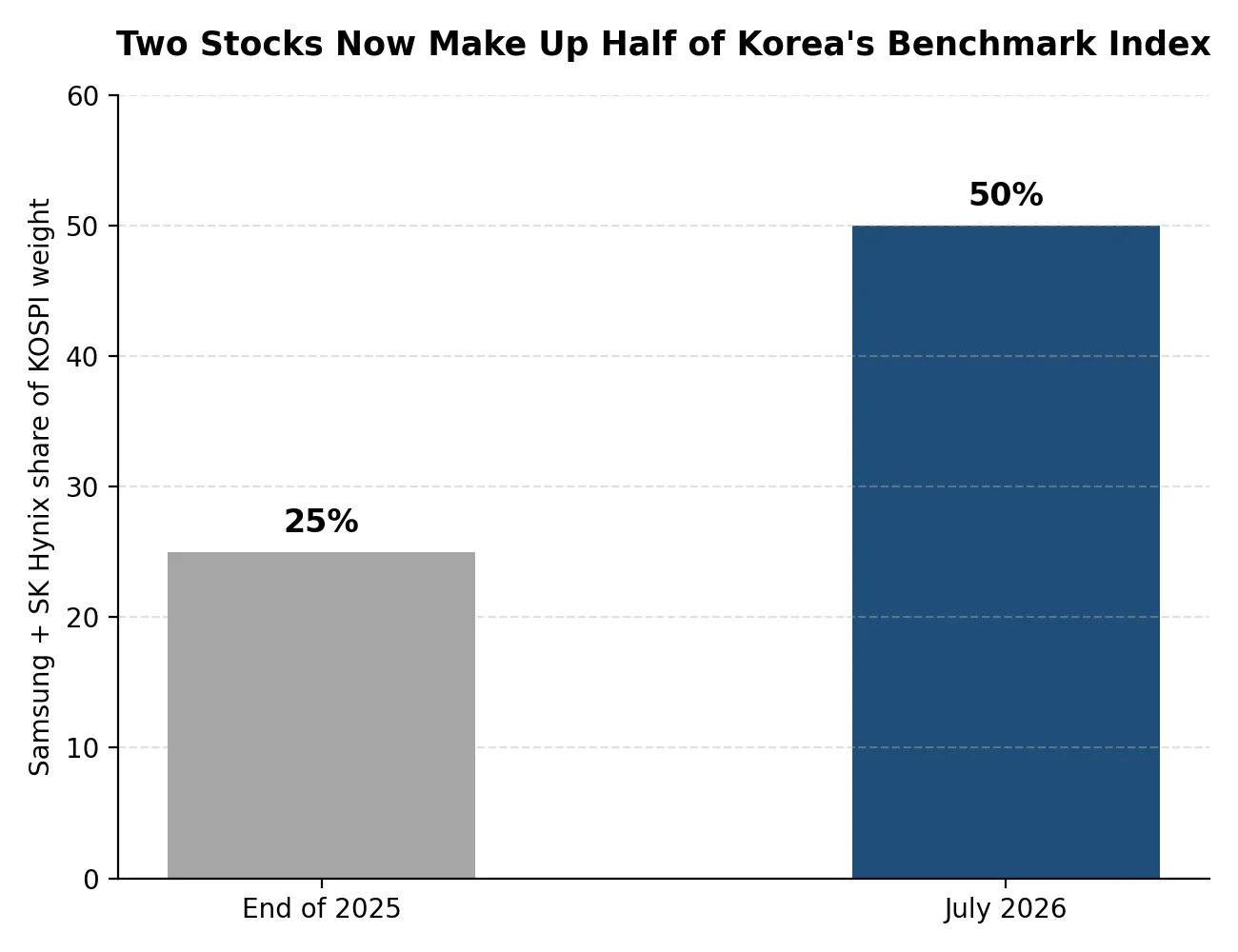

Because two stocks now carry roughly half the weight of Korea's entire benchmark index. Samsung Electronics and SK Hynix made up around a quarter of the KOSPI's total weight at the end of 2025. By July 2026, that combined weight had risen to close to half, according to eToro analyst Zavier Wong. The two companies accounted for as much as 70% of the index's total gain earlier in the year. That structure means a bad day for either stock moves the entire Korean market before the other roughly 900 listed companies get a say, and it means foreign investors who piled into Korea to buy the AI memory story can also exit that story in a single, concentrated move. That is largely what happened: continuous foreign selling turned what might have been an orderly pullback into a sharp, repeated one.

South Korea's semiconductor sector delivered close to half of the country's total corporate profits on around a fifth of its sales over the past 12 months, up from about 40% in 2020 to 2022. Median forward earnings growth for Korean chip firms stood at 52% by mid-May 2026, up from 35% at the start of the year, while Korea's chips still traded near 10 to 11 times forward earnings, the cheapest of the major Asian markets. Investors were buying a cheap story that kept growing faster, exactly the kind of trade that unwinds hardest when sentiment turns.

Korea's own economic data added pressure. The country's June inflation rate accelerated to 3.2%, the highest since December 2023, reinforcing expectations that the Bank of Korea would hold a tighter policy stance even as its economy runs hot on chip exports. Those same exports are the strongest evidence the underlying business has not weakened: South Korea's semiconductor exports hit a record USD 44.8 billion in June, up 199.5% year over year, with HBM exports alone up 171%. The stock market and the export data were telling two different stories at once.

What Actually Triggered These Drops?

Three separate forces converged, and none of them was really about chip demand collapsing.

A More Hawkish Federal Reserve

New Fed Chair Kevin Warsh, who took over in May 2026, signaled a markedly more hawkish stance than his predecessor. At his first FOMC meeting in June, nine of eighteen policymakers supported a rate hike in 2026, compared with none in March. Traders began pricing in 50 basis points of additional rate increases by December, double what they expected two weeks earlier. Higher rates raise the discount applied to future earnings and make debt-funded AI infrastructure spending harder to justify, which hits the most richly valued chip stocks hardest.

Cracks Appearing Around the Edges of the AI Story

Broadcom's fiscal second-quarter results, released June 3, beat on revenue and earnings but guided third-quarter AI chip sales to USD 16 billion against a USD 17.2 billion consensus, and the company did not raise its full-year AI forecast. The stock fell 14% the next day and pulled the rest of the sector down with it. Separately, reports that SK Hynix was slowing the pace of its HBM production expansion raised concerns about supply discipline just as investors were parsing whether AI memory demand could keep absorbing new capacity at the same price. TSMC faced its own company-specific pressure: an active US International Trade Commission patent investigation carrying the risk of an import ban, a wafer price increase of 5 to 10% across advanced nodes that caught customers off guard, and reports that Apple, Google, AMD, and Tesla were exploring dual-sourcing arrangements with Intel and Samsung to reduce dependence on a single foundry.

A Separate Crisis in Consumer Electronics

Underneath the AI story sits a second, less discussed one. IDC now forecasts global smartphone shipments will fall close to 14% in 2026, the steepest annual decline on record, as memory suppliers redirect DRAM and NAND output toward higher-margin AI servers instead of phones and PCs. That shortage is good for the chipmakers' pricing power in the short term but bad for the volume side of the business, and it is part of why memory stocks in particular have swung so violently in both directions.

Is This the End of the AI Chip Boom, or Just a Correction?

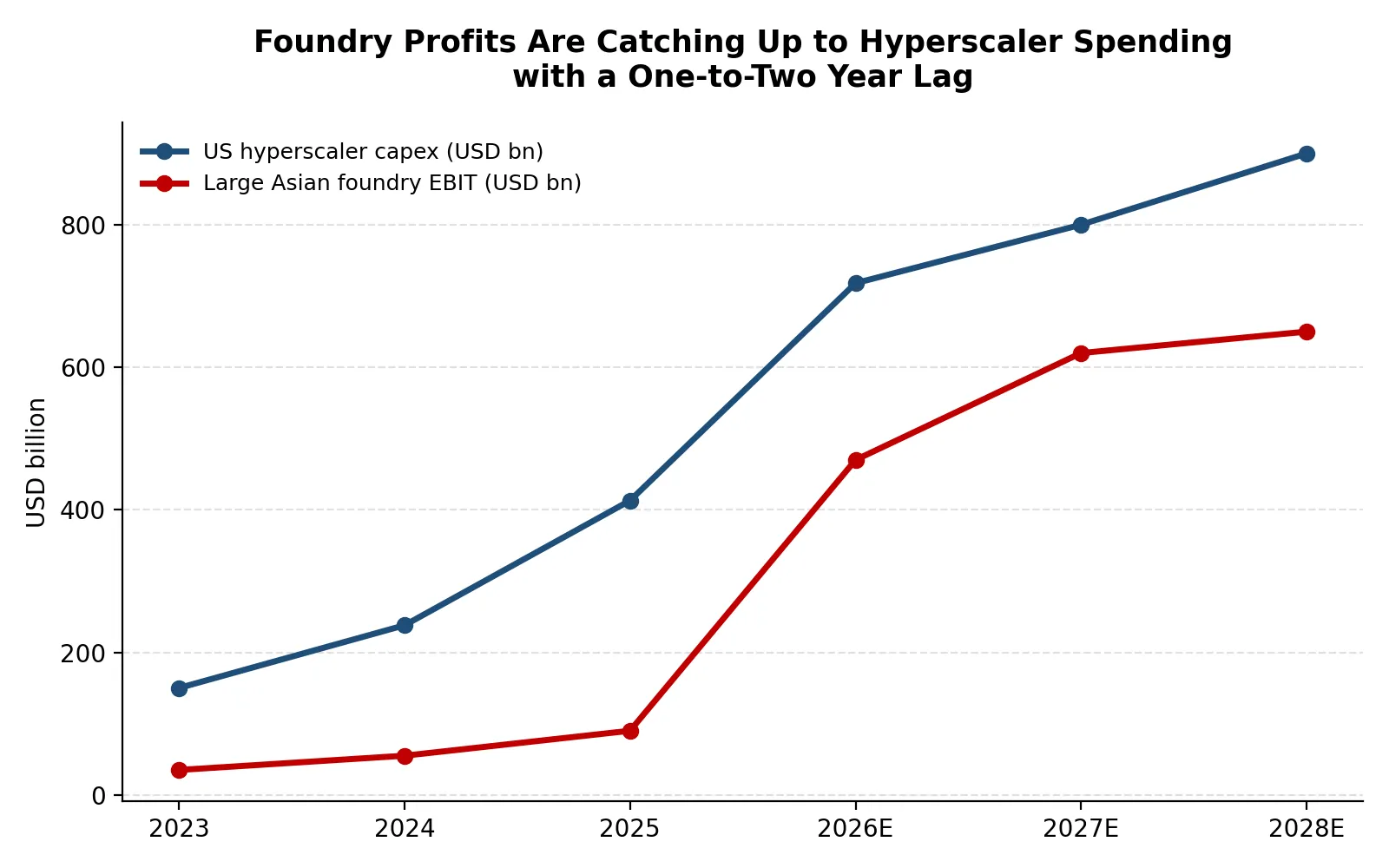

The supply side of the market says it is a correction, not an ending. Nomura's June 2026 research, titled directly "Is the cycle over?", argues that a pullback after a 211% run in chip stocks since May 2025 is healthy, and that conventional cycle-peak signals, price hikes, long-term supply contracts, possible overbooking, are visible but not yet decisive. The reasoning rests on a simple timing fact: building new fabrication or packaging capacity takes roughly two years, and the current wave of investment only began in late 2025.

That means new supply will not fully arrive until 2027 or 2028, regardless of how markets trade this month. Nomura's own tracking of new global data center projects shows the pipeline still expanding, from 240 tracked projects in March to 280 in June, with the number of gigawatt-scale projects rising from over 40 to close to 50 and 2027 capacity estimates revised up to 32 gigawatts from 28 gigawatts.

Nomura flags one real financial constraint worth taking seriously. Hyperscalers could start facing insufficient free cash flow in 2027, driven largely by surging memory costs, even as their own capex needs to keep rising in what the firm calls a "go big or go home" competition. That tension, spending more while generating less free cash, is the kind of setup that produces sharp reactions to any cautious guidance, consistent with how Broadcom's commentary moved the entire sector in June.

Figures for 2023-2025 are actuals; 2026-2028 are estimates.

Where the Bottleneck Actually Sits

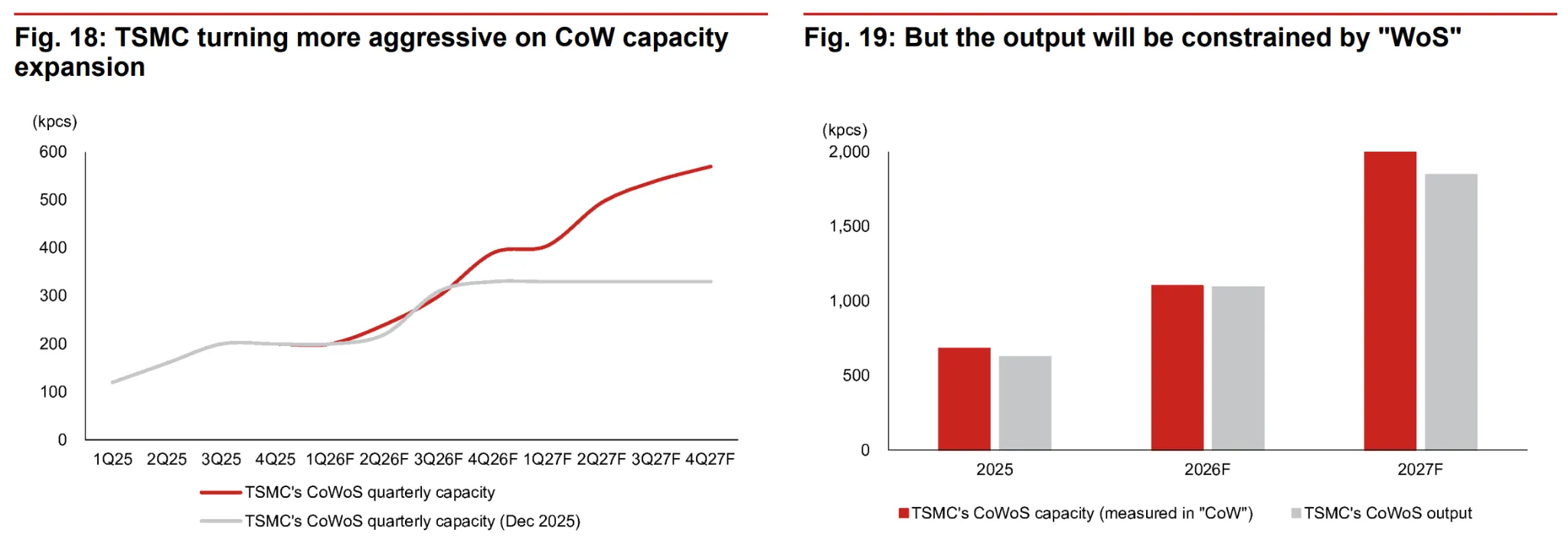

The bottleneck has also moved to a less visible part of the supply chain. TSMC's advanced packaging process, known as CoWoS, links processors to the high-bandwidth memory that AI systems need, and Nomura now expects the company to target 2,000 thousand pieces of CoWoS capacity in 2027, up from 1,100 thousand in 2026, rising to 2,500 to 3,500 thousand pieces by 2029 to support management's stated goal of high-50% annual AI revenue growth through the decade.

Nomura's own view is that smaller components, substrates, specialty chemicals, and a packaging step called wafer-on-substrate, will likely be a tighter constraint than TSMC's core process through 2027, meaning pricing power now extends well beyond the largest, most visible chip companies. Nomura also flags a longer list of technologies still needed beyond 2027, including a competing packaging approach from Intel and a newer TSMC process, before the current hardware roadmap can extend further. Until those mature, outsourced assembly and testing firms, the OSAT companies that package chips for others, should keep benefiting from both TSMC's overflow demand and their own price increases.

So, Why Does a Sell-Off Hit Emerging Markets Harder Than the US?

Because the concentration that hurt Korea in July exists across the entire emerging markets index, not just inside one country. Taiwan and South Korea together account for 85% of global foundry revenue, and semiconductors make up 75% of Taiwan's stock market capitalization and 39% of South Korea's, compared with roughly 13% in the United States. That is a sharp jump from where things stood only a few years earlier: Taiwan's chip sector generated about 55% of the country's total corporate profits in 2020 to 2022, and that figure had climbed close to 75% over the most recent 12 months, even though Taiwan's chip sector accounts for only around 5% of global semiconductor revenue.

The MSCI Emerging Markets index carries a 37% weighting toward information technology and a combined 45% geographic exposure to Taiwan and South Korea alone. An investor in a broad emerging markets fund is exposed to the chip cycle twice, once through the sector weighting and again through the country weighting. The US market has a deeper, more diversified base of non-chip companies to absorb a sector-specific shock. Korea and Taiwan largely do not.

That gap has started to close, but only partially. Emerging market chip stocks still traded at roughly a 55% forward earnings discount to developed market peers as of June 2026, down from around 75% in late 2024. The discount looks increasingly out of step with reality, since the companies carrying it now sit at the most critical stages of the global chip supply chain, leading-edge foundry work and high-bandwidth memory.

What Could Still Go Wrong From Here?

Four risks sit alongside the ones already visible in July's sell-offs.

Middle East disruption. A further escalation could disrupt helium supply, sourced partly from Qatar and essential to wafer production, and push freight and production costs higher. Taiwan's chip-sector producer price index has already swung from minus 7% year over year in late 2025 to nearly plus 9% by mid-2026. The industry holds three to six months of secured helium inventory as a buffer, but that buffer has a limited shelf life if tensions persist.

A construction gap behind the capex headlines. Only 31% of US data center capacity planned for 2026 delivery was actually under construction as of January, dropping to 13% for the full pipeline through 2032. Announced capex does not automatically become built capacity on schedule, and a project that is announced but not built does not translate into an actual chip order.

A capacity wave arriving in 2027 to 2028. TSMC's Arizona expansion, Samsung's Pyeongtaek lines, and SK Hynix's next memory facility are all scheduled to reach scale in that window, the same period hyperscaler spending growth could plateau if financing conditions stay tight. The industry has a documented history of adding capacity at the top of a cycle only for it to land as demand cools, as it did in 2015, 2019, and 2023.

China's parallel buildout. China has committed an estimated USD 30 to 50 billion to its latest state chip fund, part of a roughly USD 70 billion incentive envelope larger than the US CHIPS Act and EU Chips Act combined, and targets 70% domestic self-sufficiency in AI chips. Its share of global chip shipments by value has nonetheless fallen from 30% to 24% since 2015 under export controls, and China as a competitor still under construction rather than one in direct contention at the leading edge.

Where Does India Fit Into This Picture?

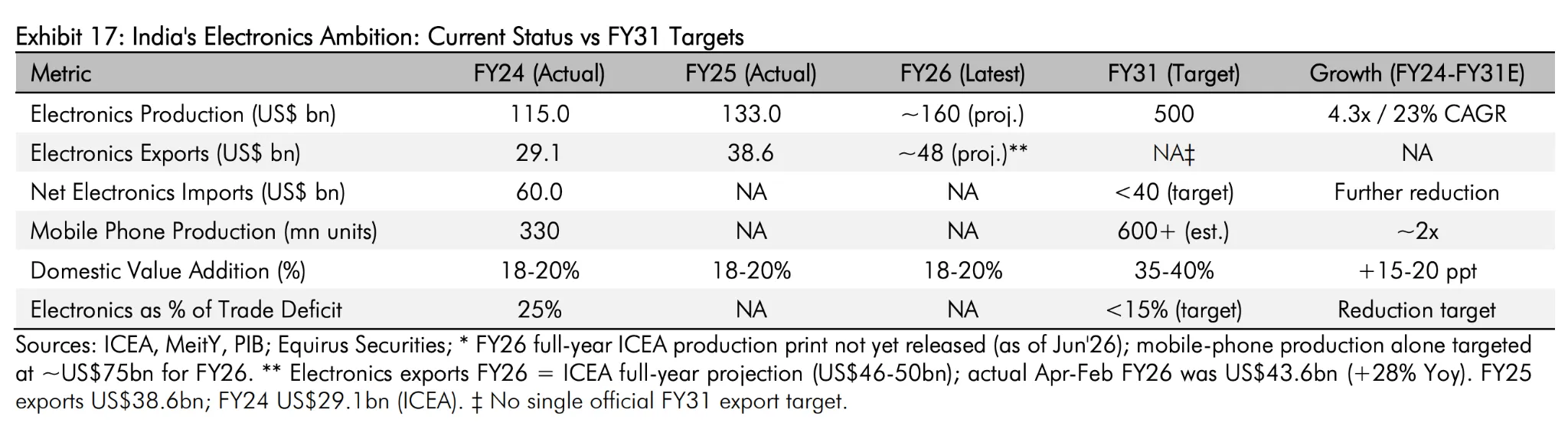

India is not exposed to this specific sell-off in any direct way, because its listed chip companies are not yet material components of a broad index the way Samsung and SK Hynix are in Korea. That is close to the point. There are 12 approved projects under India's Semiconductor Mission (ISM), representing over USD 21 billion of committed investment, and three facilities are already producing commercially: Micron's memory packaging plant in Sanand, Kaynes Technology's OSAT facility also in Sanand, and CG Power's CG Semi pilot line, also in Sanand. India's first wafer fab, an USD 11 billion joint venture between Tata Electronics and Taiwan's PSMC in Dholera, Gujarat, is roughly half built and targets its first chip in December 2026, running on 28 to 110 nanometer analog and logic processes rather than the leading-edge nodes that dominate Taiwan and Korea.

The policy behind this is deliberately structured to avoid the kind of single-sector overexposure now visible in the KOSPI. ISM covers five categories of projects, silicon fabs, display fabs, compound semiconductors, sensors, and OSAT facilities, and pays a 50% central capital subsidy alongside the company's own spending rather than only after a plant becomes operational. State governments layer an additional 20 to 40% on top, pushing the combined subsidy in the most active states, Gujarat, Assam, Uttar Pradesh, and Tamil Nadu, to 60 to 75% of total project cost. A newer ISM 2.0 program, cleared for roughly Rs 1.25 trillion, about USD 14 billion, adds equipment, materials, and intellectual property as new priorities alongside a doubled components scheme and duty removal on 25 critical minerals.

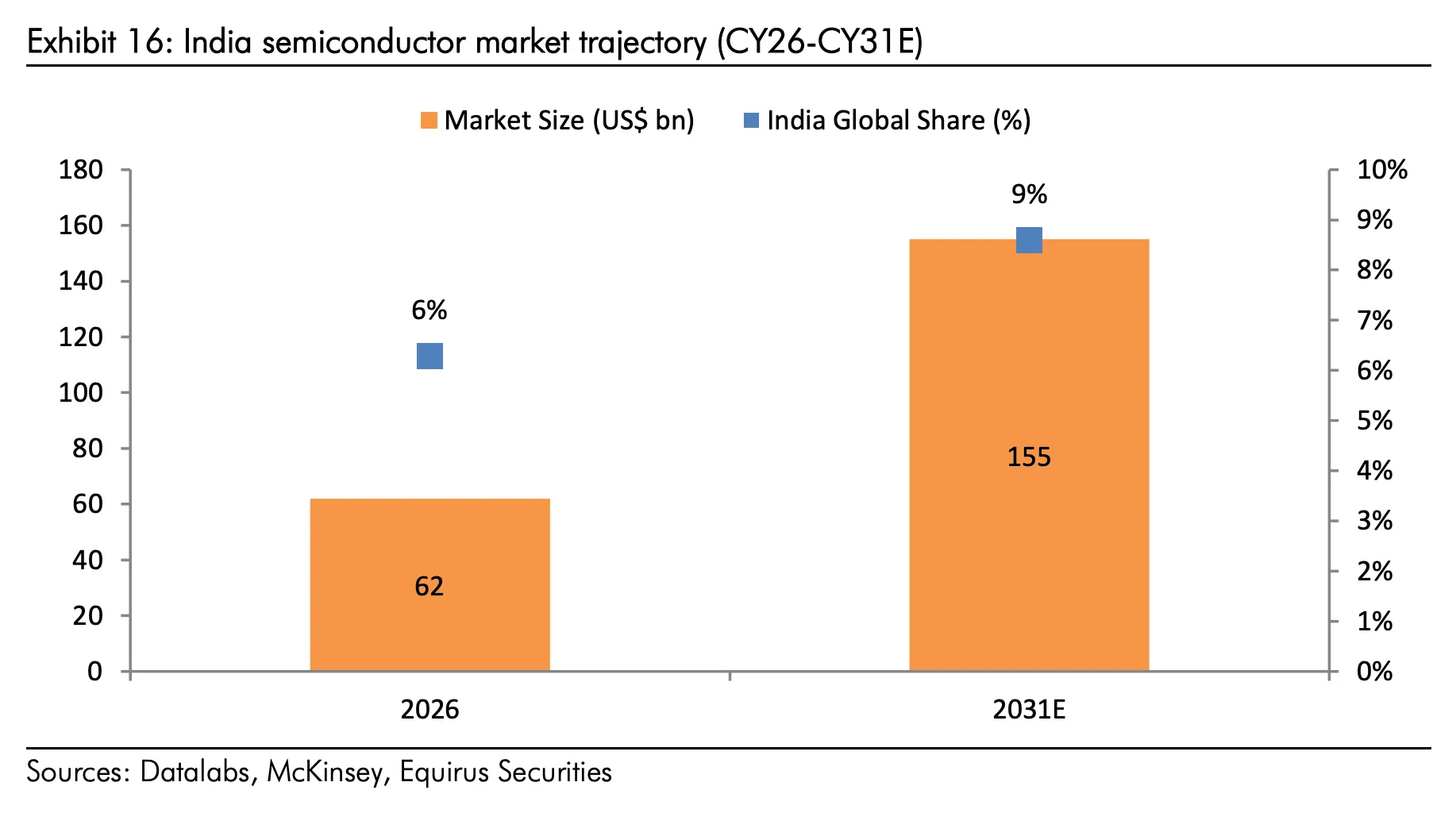

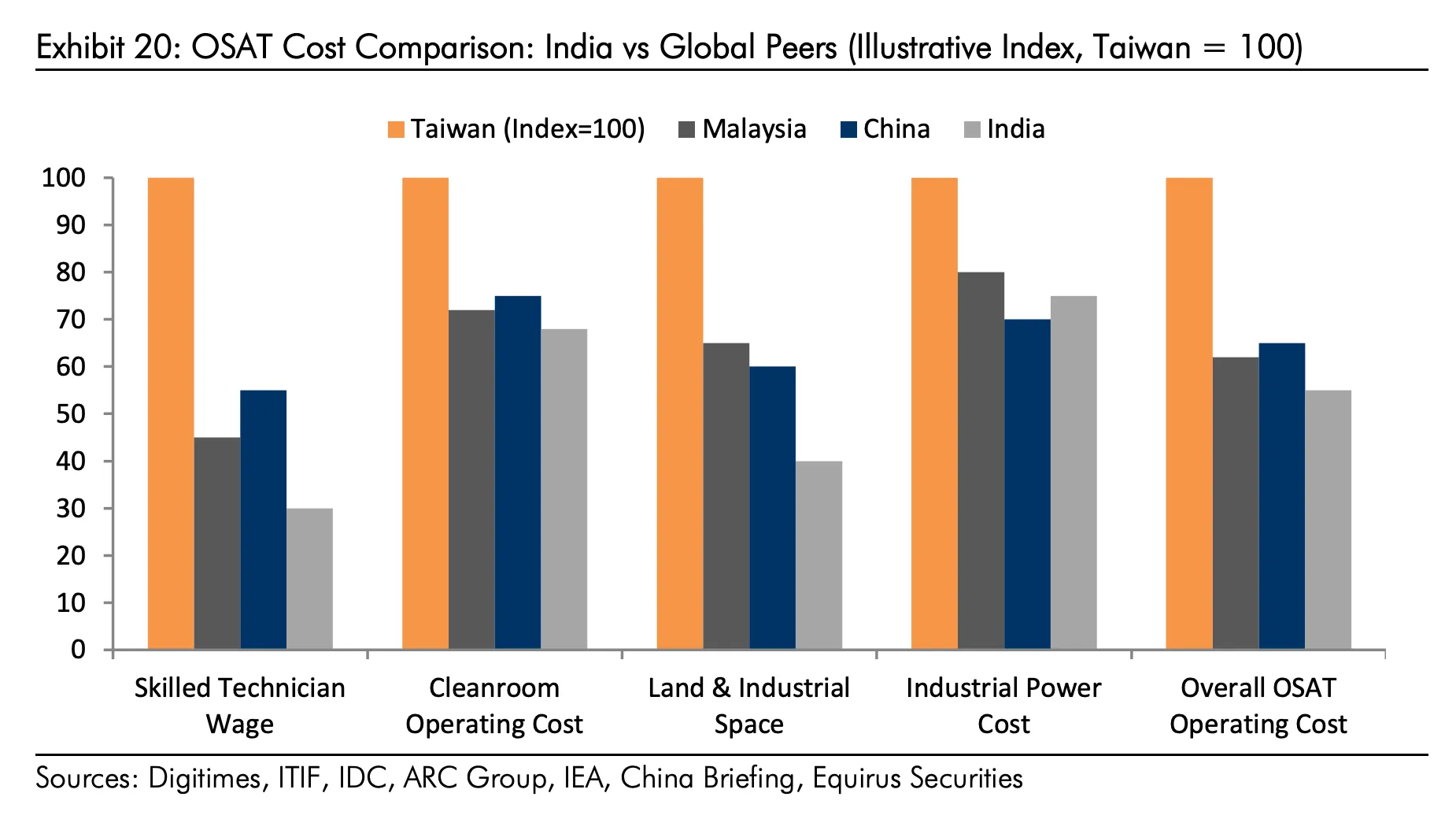

The strategic logic is straightforward. India already trains close to a fifth of the world's chip design engineers, more than any country besides the United States, yet captures only about 3% of global chip design revenue, a gap the government's design-linked incentive programs are aimed at closing. Domestic chip demand is projected to more than double from USD 62 billion in 2026 to USD 155 billion by 2031, driven mainly by smartphones, data centers, and electric vehicles. Rather than compete with Taiwan on the most advanced logic chips, India's policy has targeted mature nodes and packaging work, the segment of the industry that handles roughly 56% of global wafer capacity and serves the automotive and industrial chips India already needs in bulk. Indian OSAT operating costs run around 10% below Malaysia's and roughly 45% below Taiwan's on an indexed basis largely on lower labor and land costs.

How India's Entry Differs From Korea's Concentration Risk

The contrast with what just happened in Korea is instructive. CG Power and Kaynes Technology, the two Indian companies with direct listed exposure to chip manufacturing, together make up a small fraction of India's benchmark indices, nothing close to the roughly half of the KOSPI now held by Samsung and SK Hynix. India's chip ambitions are spread across multiple companies and states rather than concentrated in two national champions, and its manufacturing base sits in mature nodes and packaging rather than the leading-edge logic and premium memory that make Korean and Taiwanese earnings swing so sharply with global AI sentiment. India still imports more than 90% of its manufacturing equipment and 85 to 90% of the specialty chemicals a fab requires, so this remains an early, lower-stakes entry. It is, however, exactly the kind of geographic diversification that becomes more attractive each time a sell-off exposes how much of the industry's value sits in two countries and effectively two stocks.

What Should Investors Take Away From This?

The sell-offs in Korea, Taiwan, and the US were driven by a hawkish Fed, one company's cautious guidance, patent and supply-chain headlines around TSMC, and a separate consumer electronics squeeze, not by evidence that AI infrastructure spending is slowing. Hyperscaler capital spending and new data center announcements kept rising through the same period the stocks were falling, and South Korea's chip exports set a monthly record in the same month its stock market fell twice. The repeated drops confirm a structural point: when half of a country's stock index sits in two companies tied to one global cycle, that market will swing harder and faster than a more diversified one every time sentiment shifts, even as the underlying export and revenue numbers keep setting records. Emerging markets carry that risk twice over, once through sector weighting and once through geography, and the coming wave of new capacity due in 2027 and 2028 means the current combination of tight supply and high pricing power will not last indefinitely. India's early, deliberately diversified entry into the same industry does not change that in the near term, but it is a preview of where some of the industry's future concentration risk could eventually be spread.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox