by Siddhart Agarwal

Published On Aug. 15, 2021

Given the intense market rally with benchmark indices, BSE Sensex & Nifty 50, touching unprecedented levels of 55,000 & 16,500 respectively, investors are concerned about overheating and overvaluation in the markets.

Is the market overvalued? Are we nearing price correction? Is this the right time to double down on investments? What about the FED tapering and rate hikes?

As investors in the equity market and as investment advisors, we at Wright Research have noted persistent concerns among investors about the prevailing market conditions.In this post, we dissect these concerns into four eclectic questions. These burning concerns raised by investors are of utmost appropriate, and thus, we must address them in an unbiased and transparent manner.

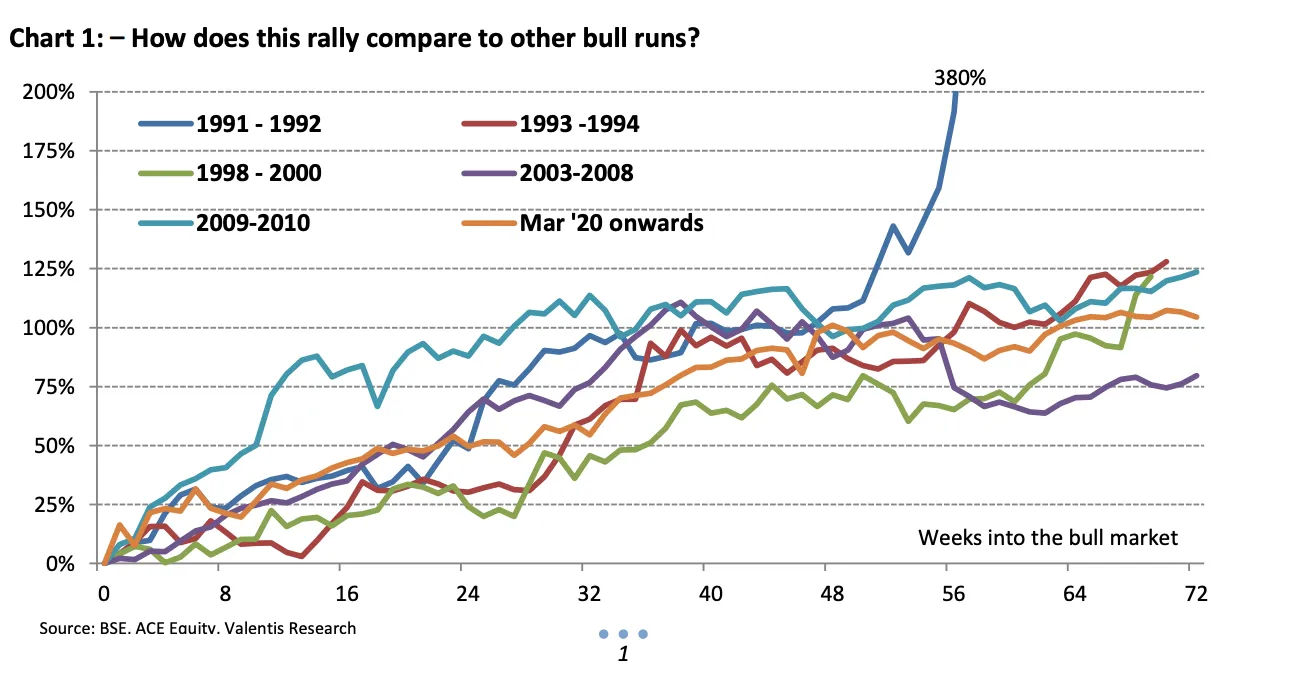

Are we at an unprecedented overvalued level in the market?

The notion of the bull and bear market is interrelated with human psychology. It is not always about the prices but rather the feeling of not experiencing something of this magnitude. The doubling of prices in 14 months like we saw last year is not new when we look back. There have been six instances in the previous 35 years where the market has doubled in 14-18 months. Morgan Stanley defines a bull market as when the index doubles from its trough. India has had six bull markets, including the present, over the past three decades.

What is essential is not the doubling of the market but the length of the rally. The time for which the rally lasts would define the residue that is left behind. The current rally is a recovery rally after the disastrous consequences of the pandemic, and policymakers across the world are looking to make a recovery and growth last, which gives us optimism about the future of the markets.

What about a market correction?

A correction is a decline of 10% or more in the price of a security from its most recent peak, and corrections are inevitable and relatively common. Over the last 16 years, we have seen double-digit corrections in almost all the years. And not all corrections mean that a bear market has started. For example, in 75% of the cases of short-term corrections in the US market, the markets have recovered to come back into the bull phase.

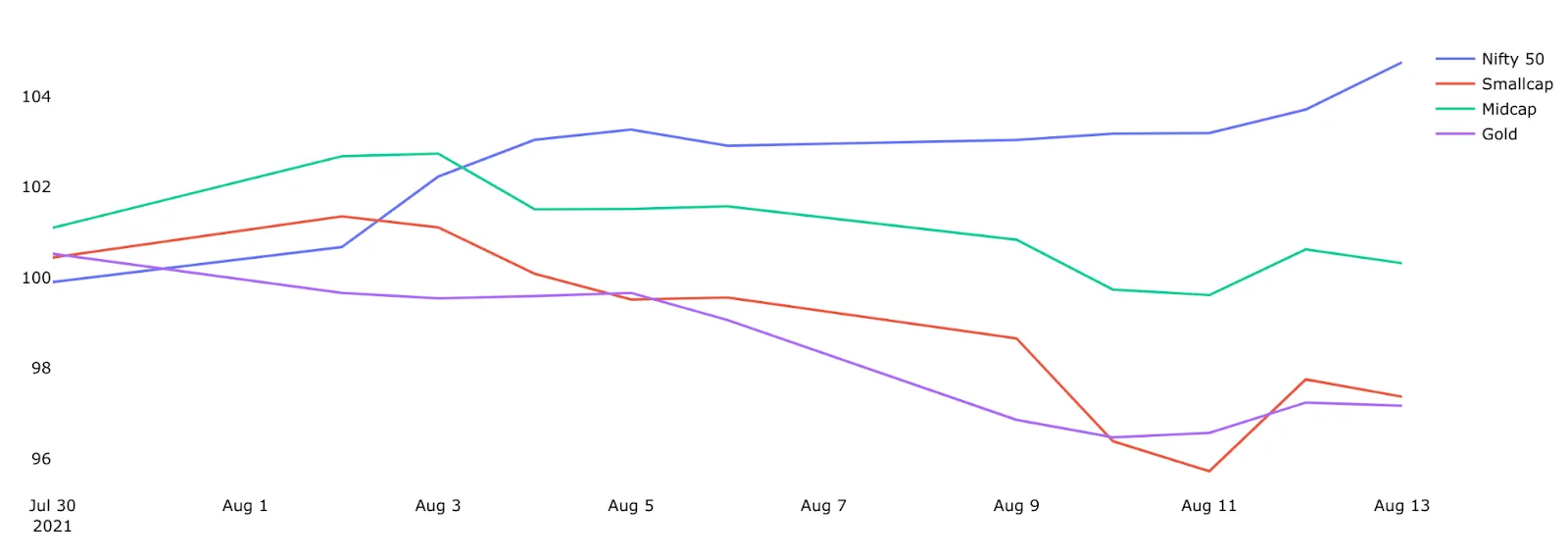

While a correction can affect all equities, it often hits some equities harder than others. For example, a short-term correction hits the small caps and highly volatile sectors hardest. At the same time, the business cycle-proof stocks like FMCG and consumer staples are unaffected by such corrections.

If we look at last week, small-caps & midcaps fell much higher than large caps.

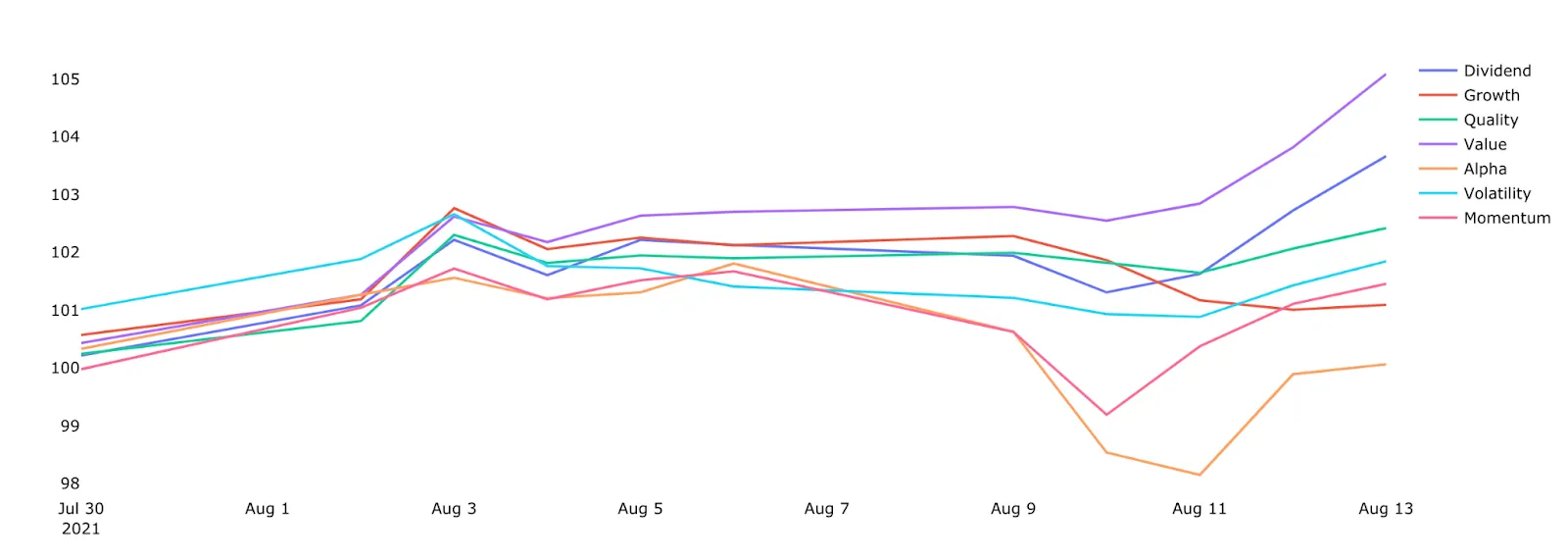

If we look at factors, Momentum & Alpha took a much larger hit compared to other factors.

However, the bigger question is whether there will be a significant correction where the market dips 40-50%. To answer that, we look at the earning cycle. We are at the nascent stage of the earnings upcycle, and such deep corrections happen only at peaks of the earnings cycle. Thus, we are confident that the market will not indulge in a deep correction.

Is this the right time to double down on investments?

If there is a short-term correction in a bull market, isn’t it an opportunity to take advantage of discounted asset prices? Well, there is no doubt about that. We got many calls from our investors last week asking if the short-term correction was an opportunity to buy.

Our view is that it is evident that we are in a bull run but a short-term consolidation phase if you look at the facts in the above two sections. Hence, it might be apt to double-down on investments when we are near the correction’s bottom. However, it is difficult to call the bottom until you see strong hints of recovery. So the correction could well be over, or it might extend for a few weeks.

We feel optimistic about the market’s long-term growth, and we are giving positive reinforcement to our investors while not trying to be exact in calling the market bottom.

What about FED tapering and rising inflation?

The US Federal Reserve has been actively supporting the markets as we recover from the impact of the coronavirus pandemic. A total of $240 Billion in fixed income assets per month, treasuries & mortgage-backed securities have been purchased.

The FED will taper off the asset-buying sooner or later. People are closely watching the Jackson Hole conference of central bankers in August for clues about tapering. In the last meeting, the FED had said that they were open to it. Scott Kimball, co-head of U.S. Fixed Income at BMO Global Asset Management, says, "The Fed opened the door to tapering, but they didn't pin themselves into it,"

The last time the FED stopped tapering in 2013, there was instability for a few months in equity markets , but there was a rally in the one-year time horizon. The effect of tapering, interest rate increase, does not necessarily have to be harmful if the economy is strong and the policymakers cushion the blow, both of which seem like the case this time.

Portfolio Update

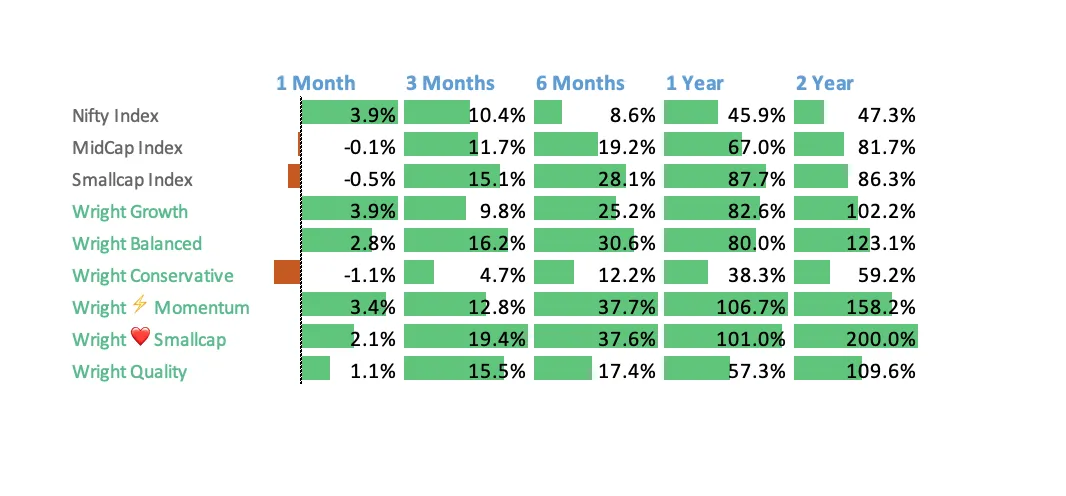

We did see a short-term correction in prices last week, which was quite evident in the meltdown of small-caps & midcaps. As expected, our smallcap portfolio took a hit, and momentum & multi-factor portfolios that have midcap exposure also had a not-so-pleasant time. However, we think that our portfolio of stocks is fit for long term growth and will come back up shining once the correction is over.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart