Every February, India dissects the Union Budget line by line. The state budgets that together shape most spending on schools, roads, hospitals, and welfare receive a fraction of that scrutiny, even though several Indian states run economies larger than mid-sized countries. In 2026, the consolidated picture looks calm. Read past the headline and that calm rests on a few specific supports that may not hold.

How healthy are India's state finances in 2026?

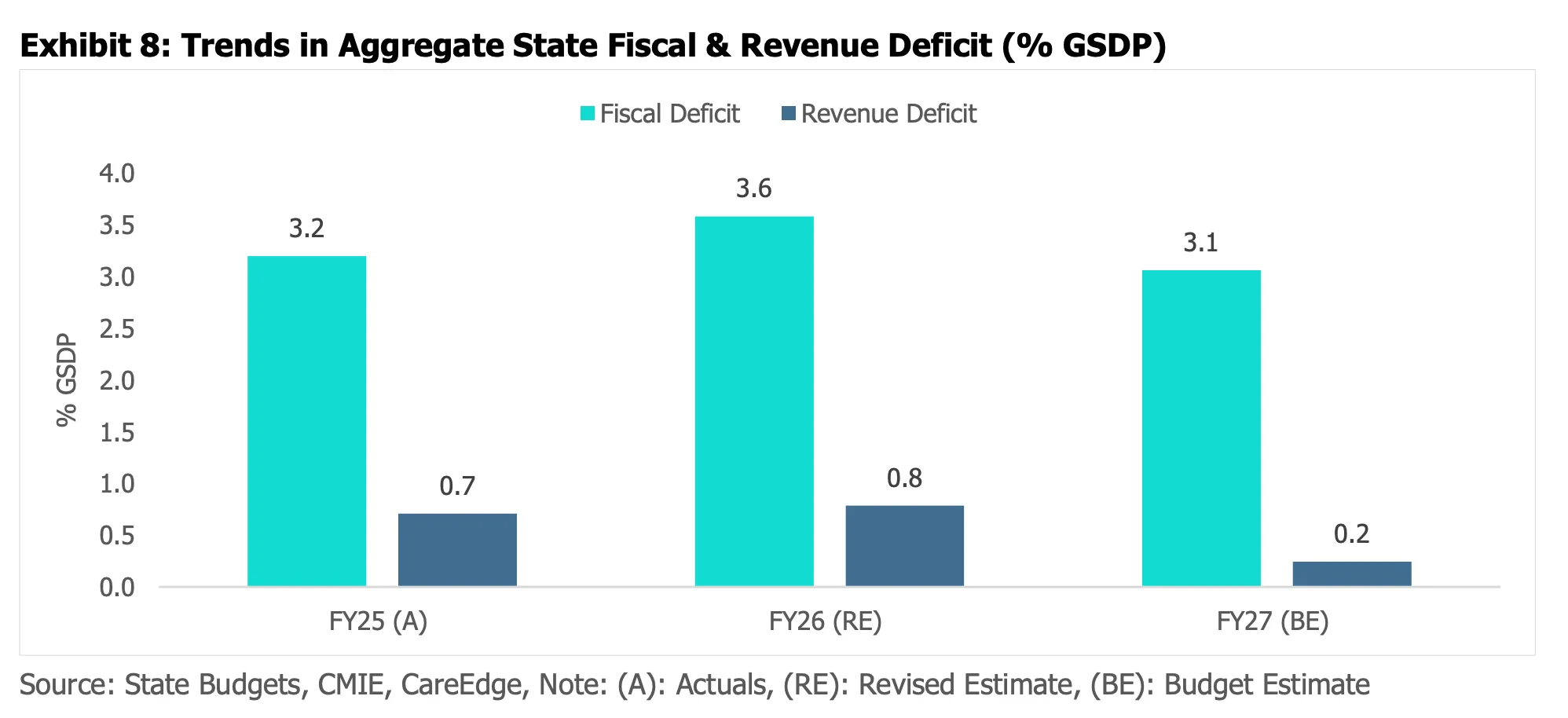

The headline number is the combined fiscal deficit, the gap between what states spend and what they earn. After staying below 3% of GDP for three years, the RBI reports it widened to 3.3% in 2024-25 and is budgeted at the same level for 2025-26, inside the Centre's 3.5% ceiling. CareEdge, using a 25-state sample measured against state GDP, estimates a higher 3.6% for FY26, easing to a budgeted 3.1% in FY27. The two readings differ because they cover different state samples and years. They agree on the shape: deficits have crept back above 3% without breaching the limit.

Chart 1: States' combined gross fiscal deficit,% of GDP. Source: RBI, State Finances 2025-26.

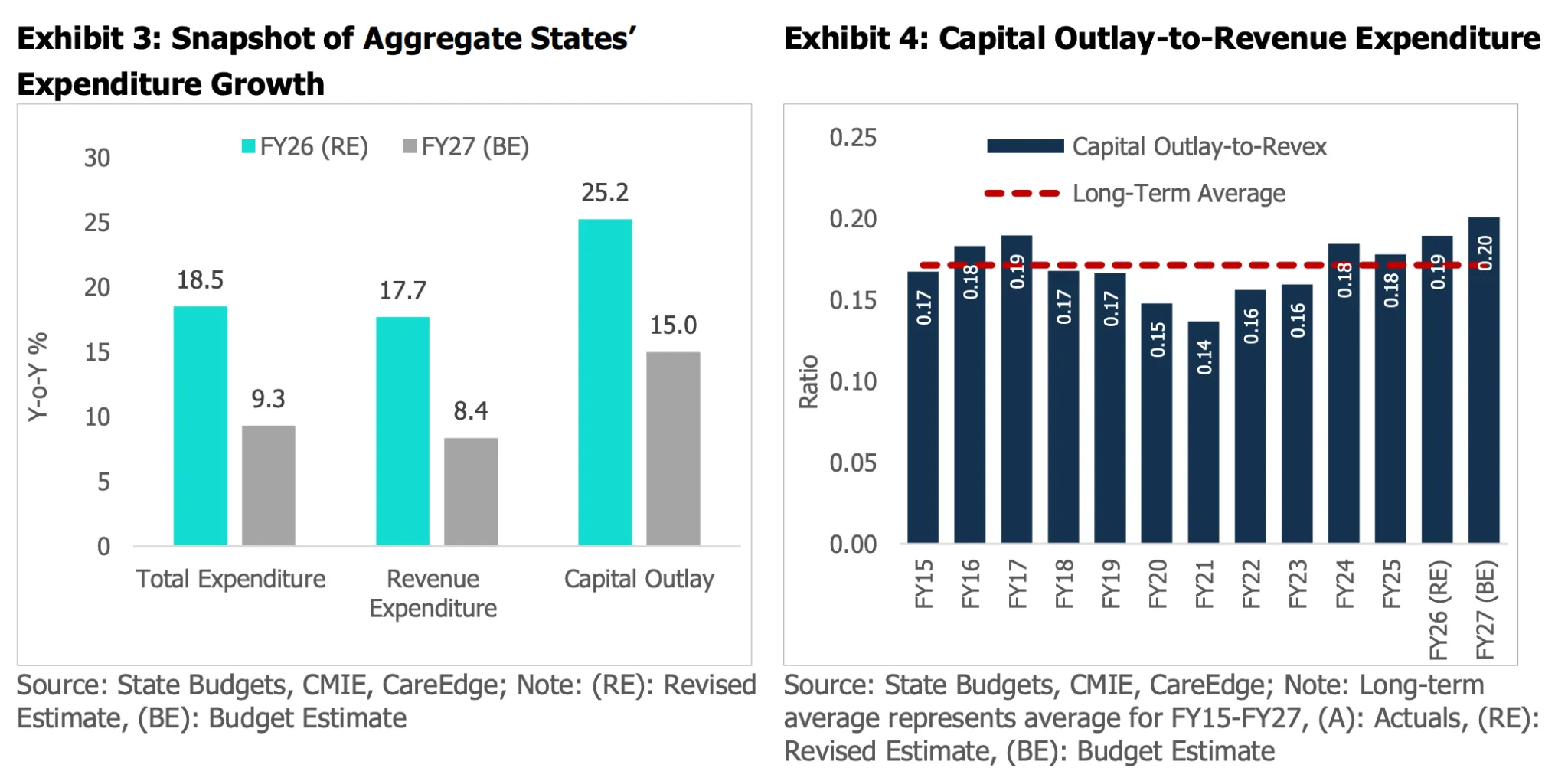

The composition of spending also improved. Capital outlay, the money states put into building assets, reached its highest share of total spending in years, rising to a budgeted 18% of total expenditure in 2025-26 from about 13% in 2020-21. Routine revenue spending eased as a share of the economy over the same period. A larger portion of borrowing is now funding investment rather than consumption.

Why does the deficit cross 3%?

Most of the rise above 3% traces to one federal scheme. The Scheme for Special Assistance to States for Capital Investment gives states 50-year, interest-free loans on the condition that they spend the money on infrastructure. It began in 2020-21 as a Covid-era stimulus and was meant to be temporary. It grew from about ₹12,000 crore in the first year to ₹1.5 lakh crore in 2024-25, and the allocation rises to ₹2 lakh crore for FY27.

The RBI notes that the deficit exceeding 3% in 2024-25 mainly reflects these loans, which sit on top of the normal borrowing ceiling. Because they carry no interest and run for half a century, they cost almost nothing to service. This is why states' interest payments have stayed within a narrow 1.5 to 1.9% of GDP for over a decade even as their debt rose to a budgeted 29.2% of GDP by March 2026. The headline deficit, in other words, overstates the underlying strain.

Is Delhi's support to states shrinking?

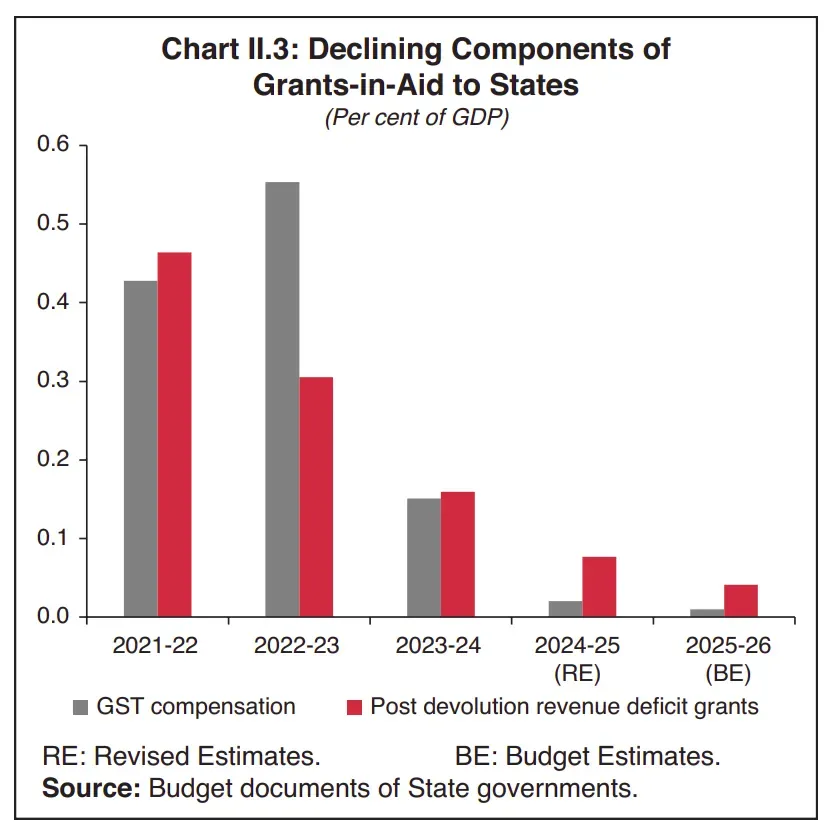

States draw money from three sources: the taxes they raise themselves, their fixed share of central taxes (devolution), and grants. The 16th Finance Commission, whose award runs from 2026-27 to 2030-31, kept the states' collective share of the divisible tax pool at 41%, the same as the previous commission. The squeeze shows up in grants.

The Commission discontinued three categories: revenue deficit grants, sector-specific grants, and state-specific grants. Together these made up about 45% of the earlier grant pool, with revenue deficit grants alone accounting for 28.5%. It redirected the money to local bodies, raising those grants to ₹7.9 lakh crore for 2026-31 from ₹4.4 lakh crore in the previous cycle.

Grant category | 15th FC | (% share) | 16th FC | (% share) |

|---|---|---|---|---|

Local governments | 4.4 | 42.2 | 7.9 | 83.5 |

Disaster management | 1.2 | 11.9 | 1.6 | 16.5 |

Revenue deficit grants | 2.9 | 28.5 | Discontinued | |

Sector-specific grants | 1.3 | 12.6 | Discontinued | |

State-specific grants | 0.5 | 4.8 | Discontinued | |

Total | 10.3 | 100.0 | 9.5 | 100.0 |

Table 1: Finance Commission grants, ₹ lakh crore. Source: 16th Finance Commission documents, CareEdge.

That reallocation shifts flexible money, which states once used to balance their own books, toward municipalities and panchayats, earmarked for specific tasks such as water and sanitation. States that leaned on the discontinued grants feel it most, including Kerala, Himachal Pradesh, Punjab, and several North-Eastern states.

Why the tax base limits the response

With grants narrowing, states fall back on their own taxes, and that base is narrow. State GST, fuel taxes, liquor excise, and stamp duties on property together make up about 90% of states' own tax revenue. One lever stands out. The RBI finds wide gaps in how efficiently states collect stamp duty and registration fees, with efficiency scores ranging from 0.3 to 0.9 across states. States that digitised land records and updated property valuations raised more money without changing a single rate. Non-tax revenue also got a lift after the July 2024 Supreme Court ruling that allowed states to tax mineral rights, prompting Karnataka, Rajasthan, and West Bengal to act.

How are states covering the gap?

When grants shrink and taxes cannot move quickly, states borrow. Market borrowings now fund about three-quarters of the combined deficit, up steadily over the past decade. Gross market borrowing reached ₹10.73 lakh crore in 2024-25 and is budgeted at ₹12.45 lakh crore for 2025-26, with most of it concentrated in the final quarter of each year.

Two features of this borrowing deserve attention. First, the spread between the safest and riskiest states is only a few basis points, which suggests the market assumes the Centre stands behind every state rather than pricing each one's finances. Second, heavy state issuance competes with the Centre and private firms for the same pool of long-term money. Large buyers such as banks and insurers have shown a more muted appetite for state bonds as supply has climbed.

What are states actually spending on?

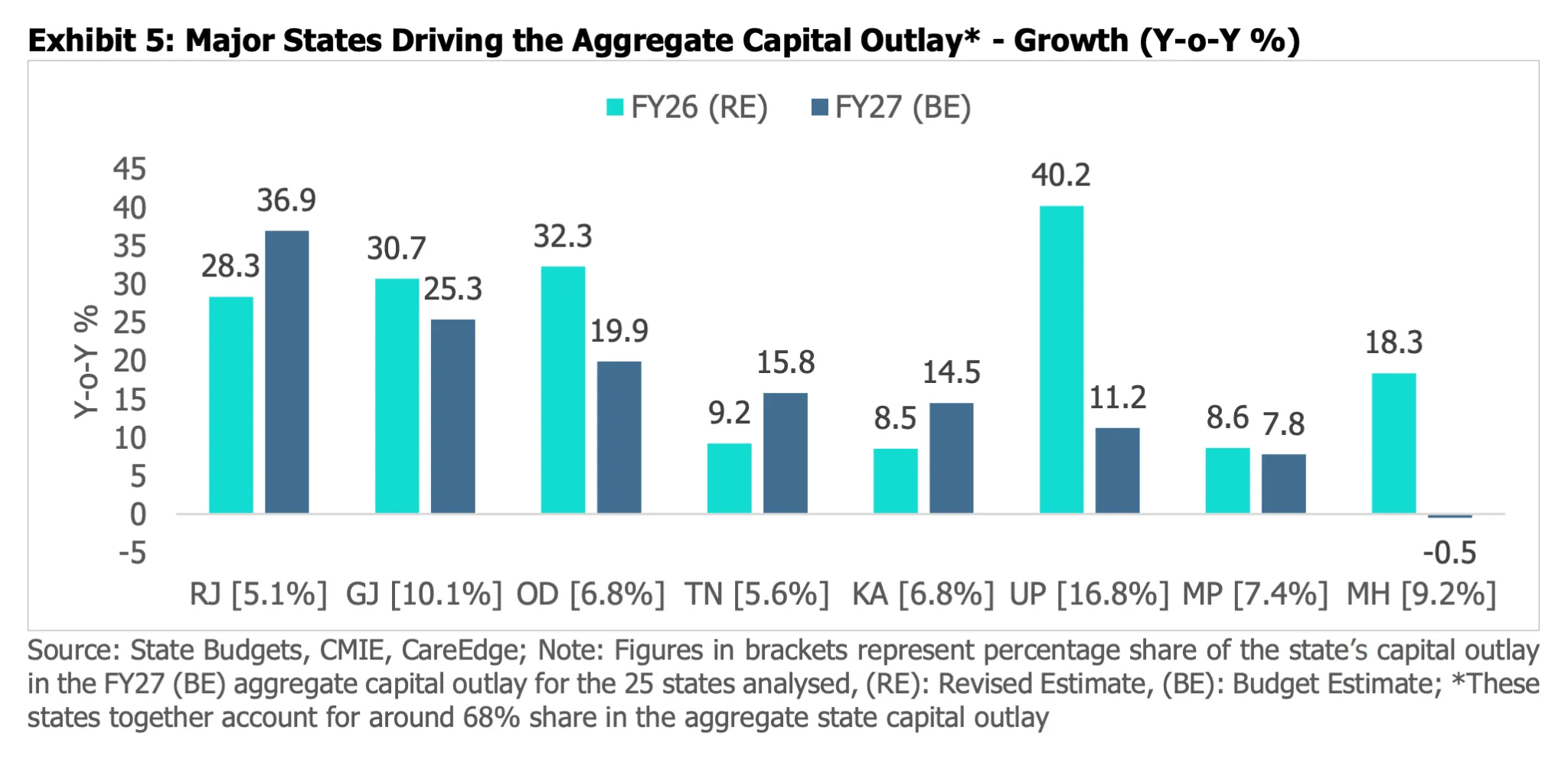

States are funding two expensive priorities at once. The first is the capital push, which the data supports: aggregate capital outlay grew about 25% in FY26 and is budgeted to grow 15% in FY27, led by Uttar Pradesh, Gujarat, Karnataka, Odisha, Tamil Nadu, and Rajasthan, which together account for roughly half of all state capital outlay.

The second is welfare. Free electricity, loan waivers, and direct cash transfers have expanded across states, often around election cycles. CareEdge attributes the jump in developmental revenue spending in FY26, to 8.8% of GDP from 8.1% the year before, mainly to these schemes. The RBI's text analysis of budget speeches captures the same shift: the language has moved from “subsidy” toward “income support” and “cash assistance,” a sign that direct transfers are becoming a structural feature of state budgets. Cash transfers are easy to start and difficult to withdraw, and they tend to harden into permanent budget lines with vocal constituencies attached.

Why are some states more stretched than others?

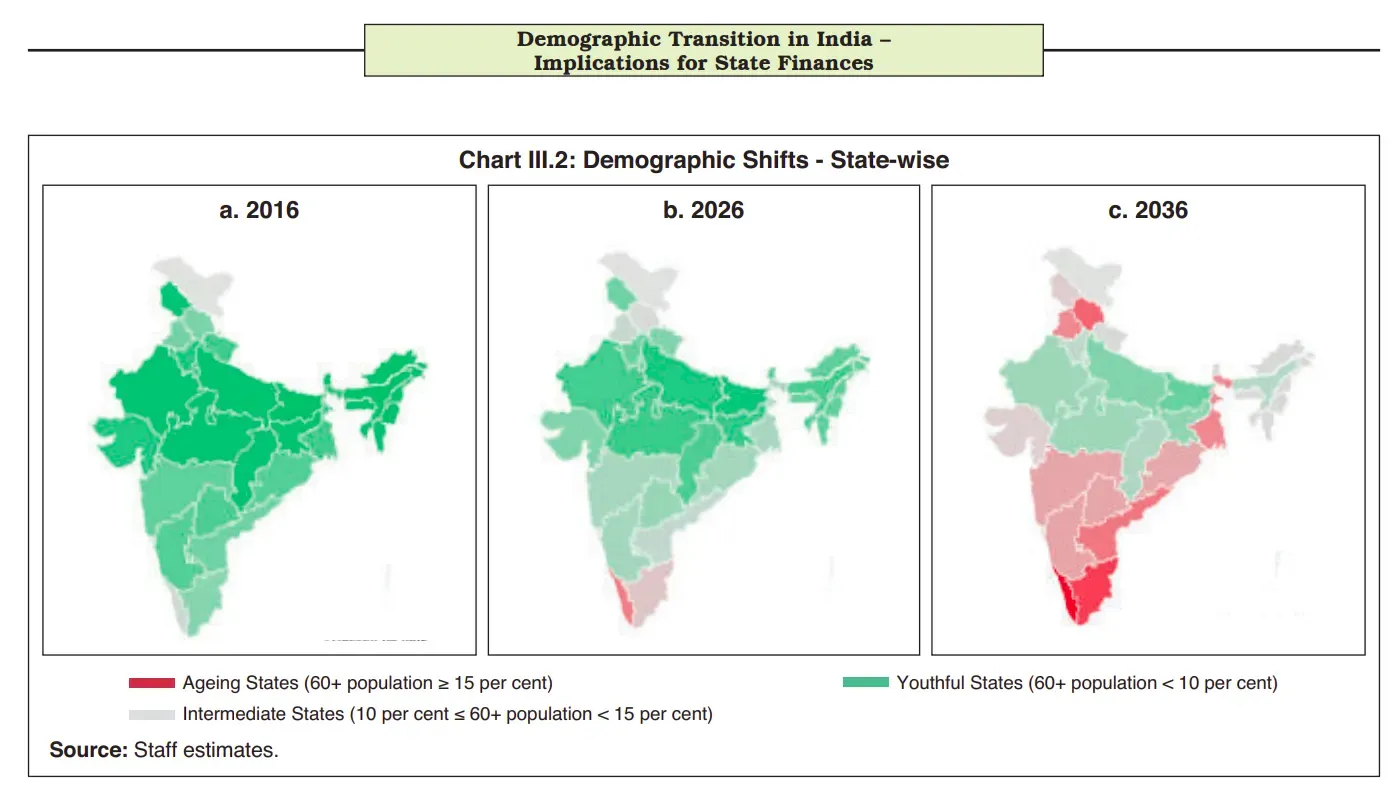

A national average hides large differences. The RBI groups states by demographics into youthful states such as Bihar, Uttar Pradesh, and Madhya Pradesh, intermediate states such as Maharashtra, Gujarat, and Karnataka, and aging states where more than 15% of people are over 60. Today that last group is Kerala and Tamil Nadu, with Punjab and Himachal Pradesh close behind.

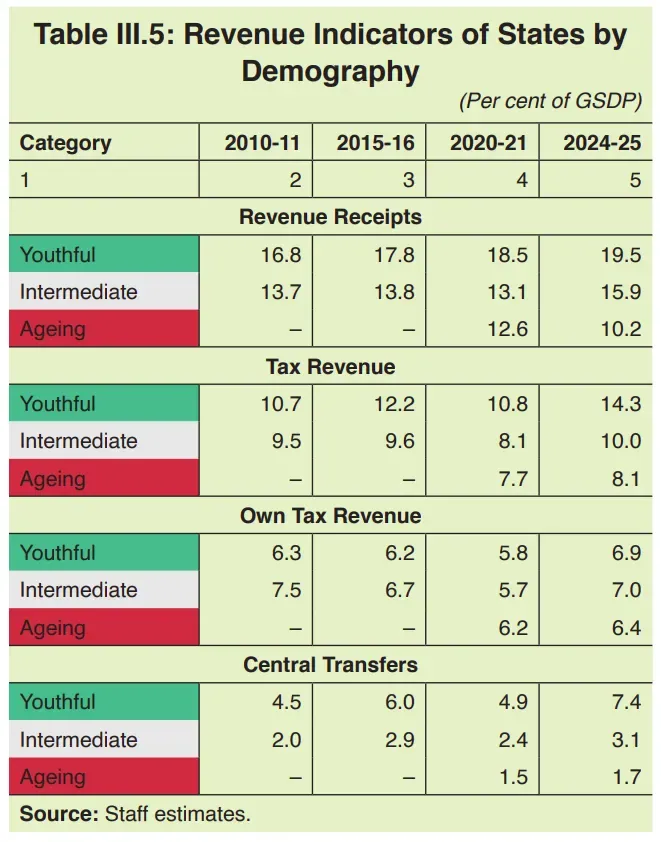

The fiscal consequences follow the demographics. For every ₹100 their economies generate, youthful state governments collect close to ₹19 to ₹20, while aging states collect around ₹10.

Chart 2: State revenue per ₹100 of state GDP, by demographic group (illustrative). Source: RBI demographic study of state finances.

The gap comes from central transfers, not from tax effort. Both groups raise a similar amount through their own taxes, around ₹6.50 to ₹7 per ₹100. Youthful states receive a much larger top-up from Delhi because the devolution formula is redistributive and India's youngest states are also among its poorest. The position is structural: an aging state like Kerala faces a stagnant tax base from a shrinking workforce and a thin cushion from the Centre at the same time. The 16th Finance Commission's new 10% weight for a state's contribution to GDP tilts the formula slightly toward economic output, which helps larger and richer states at the margin.

Migration complicates the picture. Young workers from poorer states move to richer, aging states for work, so a state with a young population on paper may not capture the gains at home. At the same time, the share of youthful states' budgets going to education has been falling even as cash transfers rise, which erodes the very advantage their demographics are supposed to provide.

Which bills are about to land?

Several costs are converging over the next few years.

The 8th Pay Commission: the latest revision of central government salaries and pensions, which states inevitably follow. Its impact is expected to reach state budgets around 2027-28.

Climate: disaster response is becoming a recurring budget line. India ranks among the countries most exposed to extreme weather, and the 16th Finance Commission has enlarged disaster management grants to ₹1.6 lakh crore for 2026-31.

Contingent liabilities: state guarantees, much of them backing loss-making power utilities, rose to 3.9% of GDP by March 2024. If a guarantee is called, the cost lands in the deficit at once, which is why the Commission is pressing states to disclose these liabilities and end off-budget borrowing.

GST in transition: the September 2025 move to a two-slab structure of 5 and 18% lowered rates on a wide range of goods. The Finance Ministry estimated a near-term revenue shortfall of about ₹48,000 crore, and several states flagged the loss at the GST Council. The RBI expects the temporary hit to be partly offset by stronger consumption.

An external shock: CareEdge links the conflict in West Asia to slower growth and softer tax collections, and estimates it could push the FY27 deficit 0.2 to 0.4 percentage points wider than the budgeted 3.1% of GSDP.

What does this add up to?

State finances in 2026 are stable on the surface and held up by two conditions. The Centre keeps lending cheaply through interest-free capital loans, and the economy grows fast enough to outpace the rising debt. Both conditions hold for now. The risks build where they meet: grants are shrinking, the tax base is narrow, welfare commitments are sticky, and a cluster of large bills arrives over the next few years.

The 16th Finance Commission has responded by tightening the rules, capping state fiscal deficits at 3% of GSDP, ending off-budget borrowing, and pressing states to rationalise subsidies and disclose contingent liabilities. States that manage their finances well will absorb these pressures. States that do not could face a sharp adjustment when the supports loosen.

State governments together account for a large share of public investment, so their capex decisions matter for national growth as much as the Centre's own budget. As long as states keep building, they reinforce India's investment-led growth strategy and the Centre's capital-spending numbers.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox