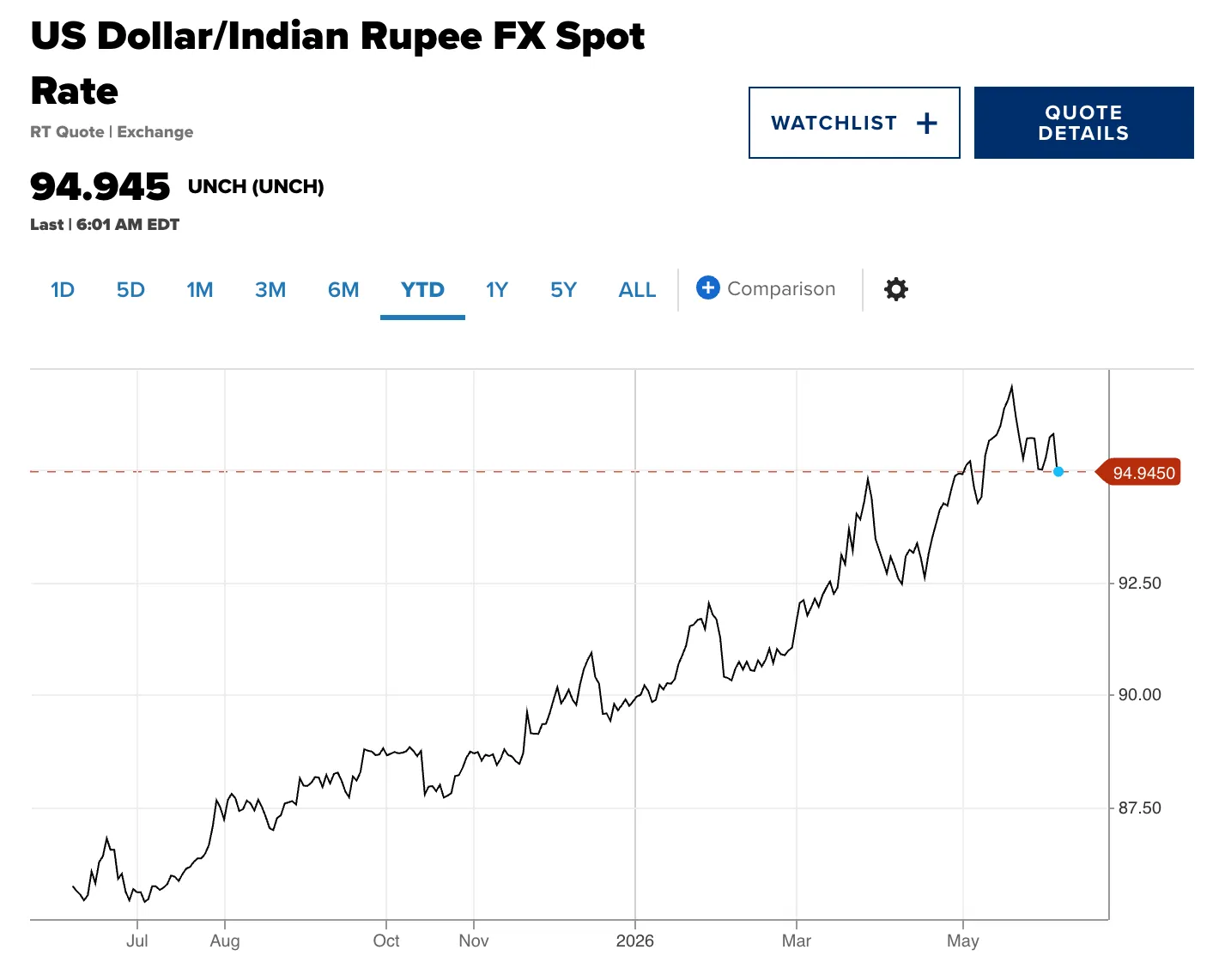

The rupee has spent most of 2026 sliding toward levels it has never touched. On June 5 it traded near 95.7 to the dollar, after dropping to a record low close to 96.96 earlier in the year. The Reserve Bank of India has been spending heavily to slow that fall. For anyone holding rupees, importing goods, or watching prices at home, this raises two plain questions. Can the RBI actually keep the rupee from falling? And what does defending the rupee cost?

Why is the rupee falling now?

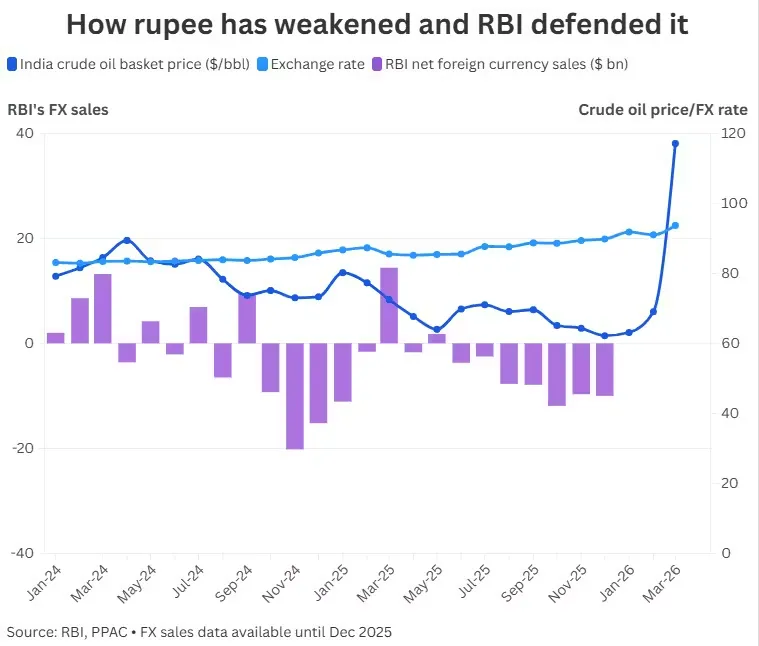

The main trigger is the war involving Iran that broke out late in February 2026. The conflict pushed crude oil prices higher, with Brent hovering around 97 dollars a barrel. India imports close to 90% of its crude, so a higher oil price means a bigger dollar bill every month. That demand for dollars pulls the rupee down.

Capital flows have made it worse. Foreign portfolio investors have been heavy sellers of Indian equities in 2026, with net outflows running into record territory of around 23 billion dollars. When investors sell Indian assets and take money out, they convert rupees into dollars, adding to the pressure. A generally firm dollar against most Asian currencies has done the rest.

Three forces pulling in the same direction. The rupee is being squeezed by a costlier oil import bill, a steady exit of foreign money, and global dollar strength at the same time. The currency has lost roughly 5 to 7% against the dollar so far this calendar year. The slide toward the 100 mark is partly mechanical and partly about sentiment, since 100 is a round number that markets and the public watch closely.

How does the RBI actually defend the rupee?

The RBI runs a managed float. It does not fix the rupee at any particular level. Its stated aim is to smooth out sharp, disorderly moves and keep the market orderly, while letting the currency adjust over time. To do that it uses a set of tools, and it tends to reach for them in a rough order, starting with the least painful.

Tool | How it works | The trade-off |

|---|---|---|

Spot dollar sales | RBI sells dollars from reserves to add supply and slow the fall. | Drains foreign exchange reserves and tightens rupee liquidity. |

Forward and swap deals | RBI sells dollars for future delivery, easing pressure without an immediate hit to reserves. | Builds up a forward book that has to be settled later. |

Liquidity tightening | Squeezing rupee liquidity lifts short-term rates and makes betting against the rupee costly. | Raises borrowing costs across the economy. |

Inflow incentives | NRI dollar deposit schemes and tax breaks for foreign bond buyers pull in dollars. | Works slowly and depends on global appetite. |

Curbs on speculation | Limits on rebooking cancelled contracts and related-party trades reduce one-way bets. | Adds friction for genuine hedgers too. |

Repo rate hike | A higher policy rate widens the yield gap and can attract capital. | Slows growth and is treated as a last resort. |

What the RBI has reached for first

Through 2026 the RBI has leaned on dollar sales, forward deals, inflow incentives, and curbs on speculation. Alongside the June rate decision, the government scrapped capital gains tax for foreign investors in government bonds and removed a 20% tax on the interest they earn, effective April 1, 2026. The RBI also sweetened dollar deposit schemes for non-resident Indians. These measures try to pull in dollars without raising borrowing costs for everyone.

How much has RBI earned in FY25 and FY26?

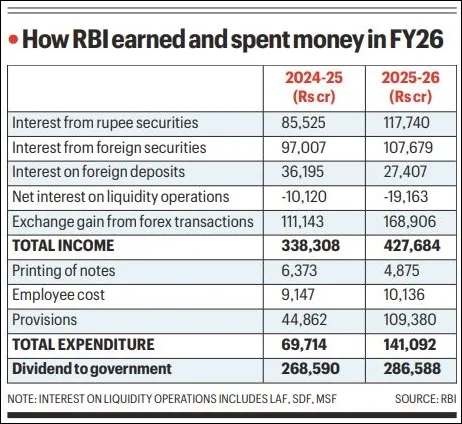

In FY25, RBI transferred ₹2.69 lakh crore as dividend to the government of India. That was a record at the time, a 27.4% jump over the ₹2.1 lakh crore paid for the previous year. The earnings came largely from higher income on foreign and domestic assets, including gains from dollar sales, even as the RBI net sold around $34.5 billion that year to steady the rupee. The board also lifted the contingent risk buffer to 7.5%, setting aside more capital before arriving at the transferable surplus.

FY26 was larger on every count. The RBI's total income rose to a record ₹4.28 lakh crore, up about 26% from the previous year, while it spent roughly ₹1.41 lakh crore on operational and provisioning expenses. Foreign exchange operations were the single biggest contributor, generating about ₹1.69 lakh crore in exchange gains, a 52% rise. Interest income from government securities came to around ₹1.18 lakh crore, and interest on foreign securities to about ₹1.08 lakh crore. Out of all this, the dividend transfer to the central government reached an all-time high of about ₹2.87 lakh crore. The RBI's balance sheet expanded by roughly 20.6% to nearly ₹92 lakh crore as of March 31, 2026.

As the rupee depreciated nearly 10% against the dollar, RBI sold foreign exchange it had bought at lower rates in earlier years, and selling those reserves at higher rates produced large gains. In other words, defending the rupee was the biggest revenue driver of the year. This ties back to the cost question, in pure profit-and-loss terms, the intervention added to income rather than draining it. The real cost showed up elsewhere, in the buffer of reserves spent down and in the rupee liquidity pulled out of the banking system. Analysts also caution that a surplus this large rests partly on one-off valuation gains, so it should not be read as a permanent run rate.

What has the defence cost so far?

The clearest cost shows up in dollar sales. In the year ended March 2026, the RBI net sold about 53 billion dollars in the foreign exchange market, the largest amount on record. That follows 34.5 billion dollars in the previous year, which was itself the highest since the 2008 crisis. The trend is one of rising intervention.

RBI net dollar sales, FY25 and FY26. Source: RBI data as reported in the press.

Reserves are large, and they are finite

Those sales draw down reserves. India's foreign exchange reserves slipped to a more than one-year low of around 681 billion dollars, with foreign currency assets near 543 billion. The reserves still cover roughly 10 to 11 months of imports, which is a comfortable buffer by most standards. The point is that reserves are not unlimited. India needs them to pay for essential imports such as crude oil, machinery, and edible oils, so the RBI cannot sell dollars forever.

Why Does the RBI Keep Returning to the Swap Window?

The buy-sell swap auction shows how a once-occasional tool has turned into a recurring crutch. The mechanics are simple: a bank sells dollars to the RBI today and agrees to buy them back later, which leaves the bank with rupees in the meantime and injects liquidity into the system without touching the policy rate. The RBI introduced the format in March 2019 under Shaktikanta Das to plug a routine liquidity deficit, and the first $5 billion auction drew bids 3.3 times the amount on offer. It reached for the same tool in March 2020 as COVID hit, but in reverse, selling dollars to banks when global dollar funding dried up.

Date | Amount | Tenor | Total Bids | Cover | Cut-off | Accepted |

Jan 31, 2025 | $5B | 6-month | $25.6B | 5.1× | ₹0.97 | $5.1B |

Feb 28, 2025 | $10B | 3-year | $16.2B | 1.6× | ₹6.55 | $10.1B |

Mar 24, 2025 | $10B | 3-year | >$20B | 2×+ | ₹5.86 | $10.0B |

Dec 16, 2025 | $5B | 3-year | $10.4B | 2.1× | ₹7.65 | $5.0B |

Jan 13, 2026 | $10B | 3-year | $29.9B | 3.0× | ₹7.28 | $10.0B |

Feb 4, 2026 | $10B | 3-year | $25.0B | 2.5× | ₹7.51 | $10.0B |

May 26, 2026 | $5B | 3-year | $9.8B | 2.0× | ₹9.10 | $5.0B |

The present cycle stands apart on both scale and urgency. Since January 2025 the RBI has run seven buy-sell auctions worth at least $55 billion, and the January 2025 round alone was oversubscribed five-fold, with $25.6 billion in bids against $5 billion offered. The price banks pay has climbed with each round, from a weighted average premium of ₹6.73 in February 2025 to ₹7.51 in February 2026 to ₹9.20 now, so every auction costs more than the one before. That rising premium is the tell. The RBI keeps returning to the window because the underlying loop has not broken: it sells dollars to defend the rupee, that drains rupee liquidity, the swap injects the liquidity back, and the swap in turn swells the forward book that eats into future reserves. Each round trip leaves the balance sheet a little more encumbered than the last.

Selling dollars tightens money at home

There is a nuance worth keeping in view. The RBI tends to buy dollars when the rupee is calm and sell when it is under pressure, so the buying and selling generates gains. Reported estimates put those gains in the region of 50,000 crore rupees, and the RBI transferred a record surplus of about 2.86 lakh crore rupees to the government for FY26. So the headline drawdown overstates the net financial hit. The harder cost is strategic: every dollar sold is a dollar of buffer used up, and the buffer is what protects India in the next shock.

There is a second, quieter cost. When the RBI sells dollars, it takes rupees out of the banking system. That tightens domestic liquidity and can push up short-term interest rates, which the RBI then has to manage so that credit does not seize up. Defending the currency and keeping money markets steady can pull in opposite directions.

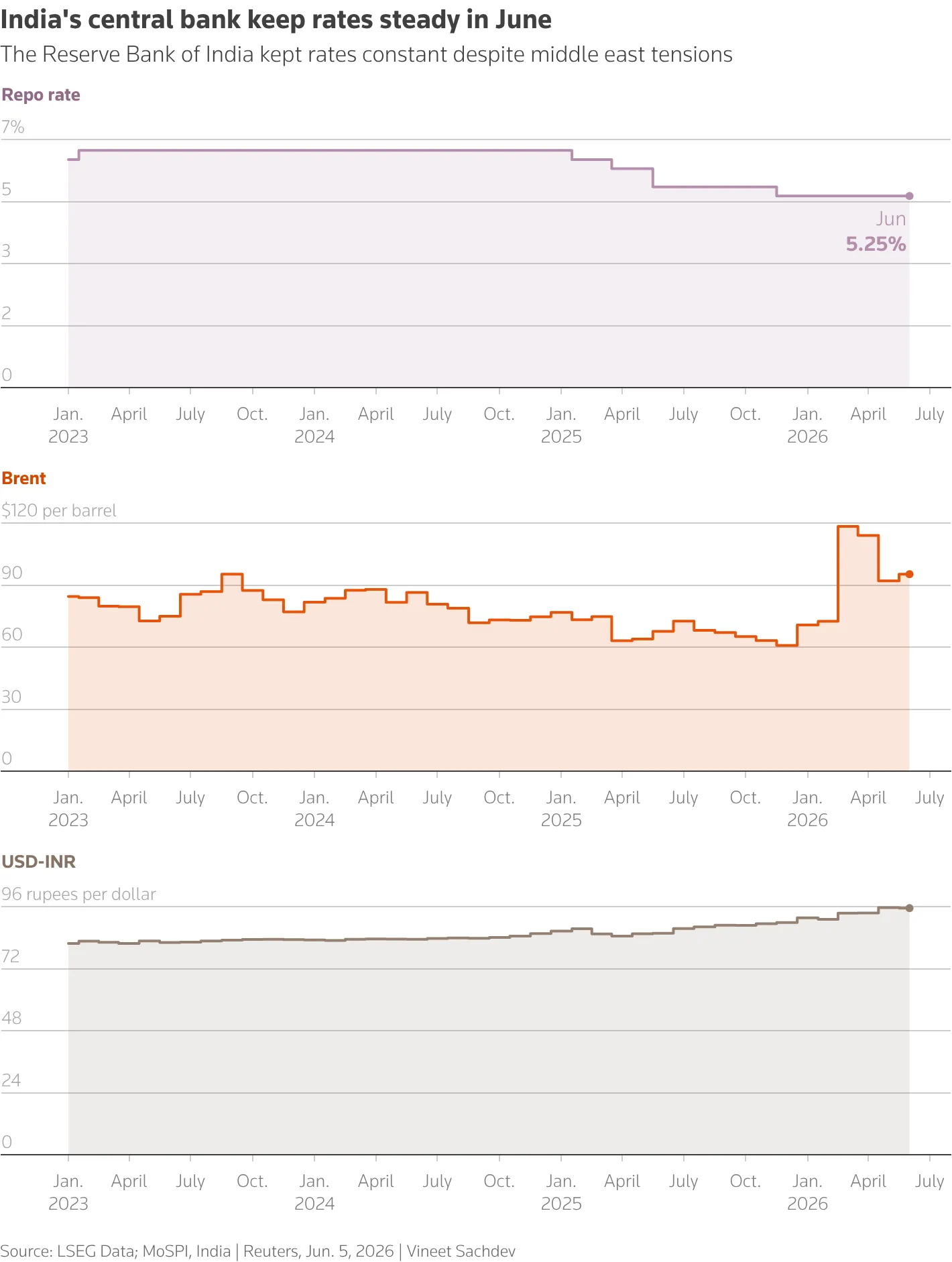

Why is the RBI holding rates instead of hiking?

On June 5, the RBI kept the repo rate at 5.25% for the third meeting in a row, with a neutral stance. A rate hike is the textbook way to defend a currency, because a higher rate widens the yield gap with the United States and can attract foreign money. The RBI chose not to use it. The reasons sit in the data.

Inflation is low and growth is slowing

Retail inflation was 3.48% in April, comfortably inside the 2 to 6% target band. With prices contained, there is little inflation reason to raise rates. Growth, on the other hand, is softening. The RBI cut its growth forecast for the current year to 6.6%, down from 6.9% in April, after the economy grew 7.6% in the year ended March 2026. Raising rates to defend the rupee would risk slowing growth further at a delicate moment.

What policymakers and economists are saying

RBI officials have signalled that inflation, rather than the currency, will guide interest rate decisions. A meaningful currency defence through rates would require steep increases, and smaller moves tend to do little while still hurting demand. Former RBI Governor D. Subbarao has argued that monetary policy should focus on inflation and growth rather than the currency. Economists have praised the RBI for letting the rupee adjust while stepping in only to prevent disorderly moves, and warned against intervening so heavily that the currency stops moving at all.

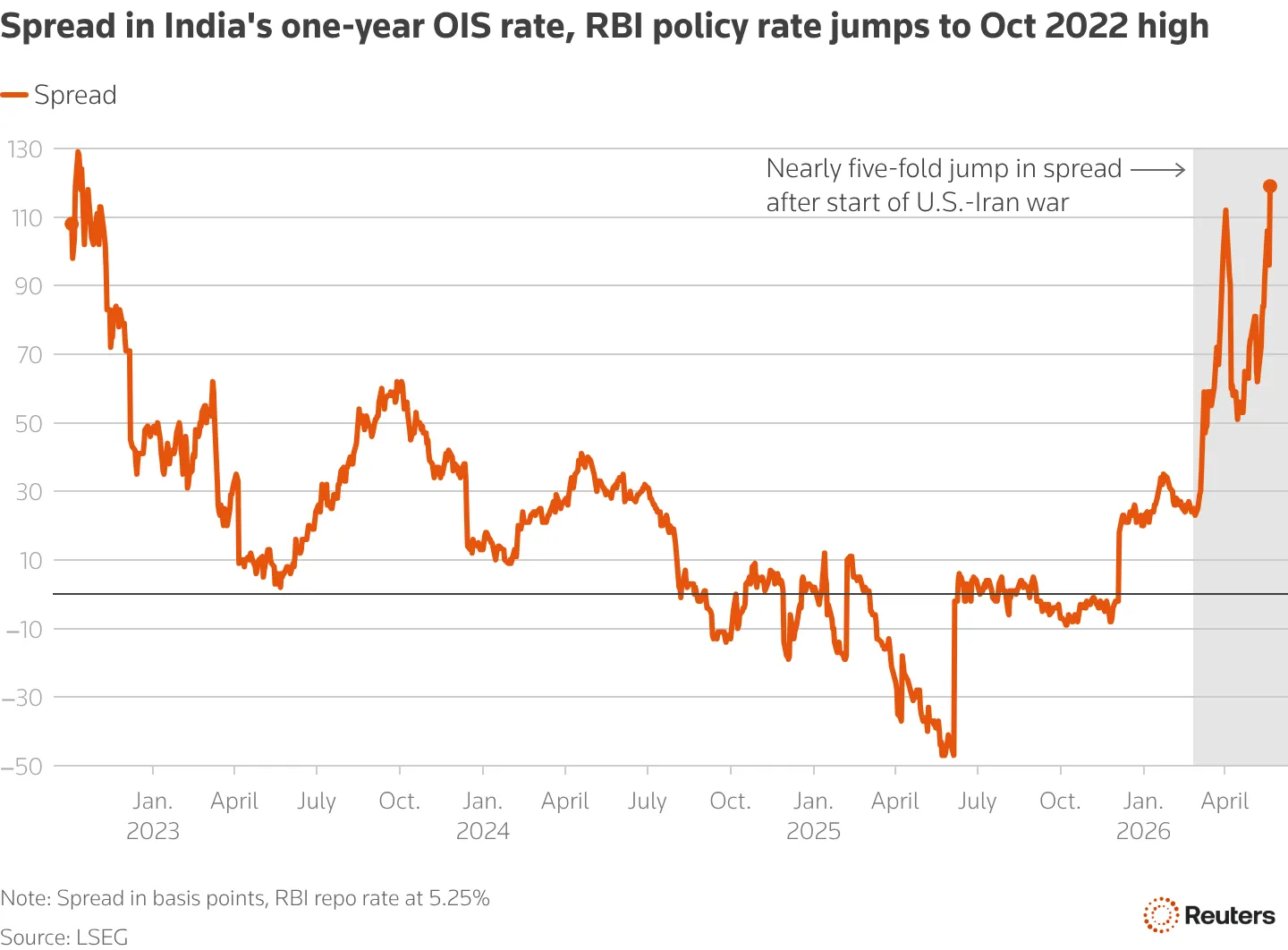

Call Rate Spread Jumps To Highest

The call rate captures today's stress, but the overnight indexed swap (OIS) market shows what traders expect next. A one-year OIS is essentially a bet on where the overnight rate, the same rate the call market reflects, will average over the coming twelve months, so when the one-year OIS sits above the RBI's repo rate, the market is pricing in hikes.

The spread between the one-year OIS and the 5.25% repo rate jumped nearly five-fold after the U.S.-Iran war began, swinging from barely above the policy rate (and negative as recently as mid-2025, when traders were betting on cuts) to well over 100 basis points, the highest since late 2022.

In plain terms, the swap market is wagering that the RBI will eventually have to raise rates to defend the rupee. The central bank disagrees. Reuters reported in late May 2026 that the RBI does not see rate hikes as the best way to shore up the currency and that inflation, rather than the exchange rate, will guide its decisions on borrowing costs, even as swap markets priced in roughly 40 basis points of hikes over three months and more than 100 over a year. The two readings together tell the story of the squeeze: the call rate spiking to 6.9% signals an immediate shortage of rupees from heavy dollar sales, while the widening OIS spread signals that the market expects that pressure to force the RBI's hand on rates, whatever it says today.

India is taking a different path from its neighbours

Several regional peers have gone the other way. Indonesia raised its policy rate by 50 basis points to 5.25% in May, Sri Lanka raised by 100 basis points, and the Philippines has also tightened. India has held, betting that targeted dollar and inflow measures can steady the rupee without sacrificing growth. Interest rate swap markets are still pricing in some tightening, around 40 basis points over three months, and many economists expect a possible rate move as early as August if pressure persists.

So can the RBI keep the rupee from falling?

The honest answer is that the RBI can slow and smooth the fall, but it cannot reverse a decline that is driven by fundamentals. As long as oil stays expensive and foreign money keeps leaving, there is a steady downward pull on the rupee. What the RBI can do is prevent panic, stop disorderly one-day crashes, and buy time for the external picture to improve.

A durable recovery in the rupee depends on factors largely outside the RBI's control. The first is oil. If the Iran conflict eases and crude prices fall back, India's import bill shrinks and dollar demand cools. The second is foreign flows. A return of portfolio investors to Indian equities and bonds would bring dollars back in, and the recent tax breaks for foreign bond buyers are aimed squarely at that. The third is the global dollar. If the United States Federal Reserve moves toward easier policy, the dollar tends to soften and the pressure on emerging-market currencies lifts. The RBI can hold the line while it waits for these to turn. It cannot manufacture them.

That is the realistic frame for the months ahead. Expect more of the same mix: continued dollar sales kept within prudent limits, fresh incentives to pull in dollars, and a rate hike held in reserve as a last resort if the rupee threatens to break down in a disorderly way. The 100 mark may well be tested, and crossing it would be more of a psychological event than an economic cliff. The deeper question is not whether the rupee touches a round number, but how much of its buffer India is willing to spend to manage the descent, and for how long.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox