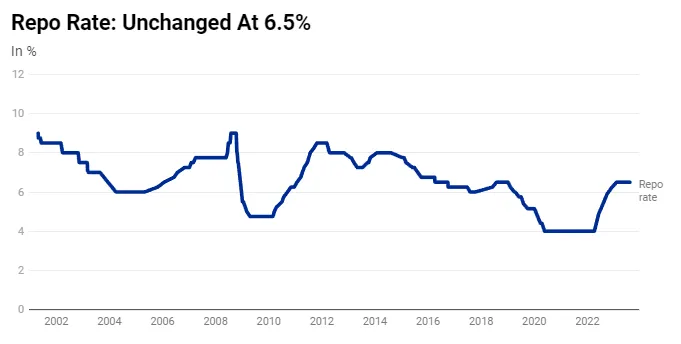

The Monetary Policy Committee (MPC), responsible for setting interest rates in India, has opted to hold the repo rate at 6.5%, with the standing deposit facility rate at 6.25%, and the marginal standing facility rate at 6.75%. This decision comes amid a recent spike in inflation, driven primarily by high prices of food items. Since May 2022, the RBI has raised rates by 250 basis points (bps) in an effort to combat inflation. The latest announcement highlights the central bank's "wait-and-watch" approach, with Governor Shaktikanta Das repeating his caution on the inflation front.

Despite the jump in inflation to 4.81% in June, up from 4.31% in May, inflation has remained largely under the 6% upper band for the last four months. However, the Consumer Food Price Index (CPI) rose 2.5% month-on-month in June, showing the impact of food prices on inflation. Core inflation (non-food, non-oil) remains sticky but has come below the 6% mark, staying in the range of 5.5% to 6.1% in recent months.

Economists had anticipated that the MPC would hold rates steady due to continued upside risks to inflation, including the potential effects of El Niño and erratic monsoon distribution. The erratic monsoon, in particular, has led to a surge in food prices, with tomato prices in wholesale markets rising by over 1,400% in the past three months.

A Reuters poll has suggested that the MPC will likely hold the interest rate at 6.50% through end-March 2024, with potential cuts in Q2 2024. Another poll predicted that India's retail inflation may have accelerated to 6.40% in July, breaching the RBI's tolerance band for the first time in five months. This announcement holds significance against the backdrop of inflationary pressures, fluctuating food prices, global uncertainties, and India's economic growth trajectory.

Measures to Absorb Surplus Liquidity

In response to surplus liquidity from factors like the return of ₹2000 banknotes and capital inflows, an incremental cash reserve ratio (I-CRR) of 10% was introduced, effective from August 12, 2023. This temporary measure will be reviewed on September 8, 2023, or earlier to ensure financial stability without impacting festive season spending.

What is I-CRR (Incremental Cash Reserve Ratio)?

Cash Reserve Ratio (CRR) is a portion of deposits that banks have to maintain with the central bank. ICRR, however, is a temporary measure focusing on the incremental deposits between two specific dates. ICRR was last employed in 2016, after the demonetization of ₹500 and ₹1,000 notes. It was a 100% ICRR then, aimed to absorb the sudden inflow of liquidity. This time, the ICRR is set at 10%, specifically targeting the deposits that have flowed in between May 19 and July 28. This coincides with the period following the withdrawal of the ₹2,000 note, which resulted in ₹3.14 lakh crore returning to the banking system.

Why 10% ICRR Now?

The RBI's decision seems to have taken market participants by surprise, yet the move is seen as strategic and thoughtful. Here's why:

Controlling Excess Liquidity: The deposit of ₹2,000 notes has resulted in surplus liquidity. An excess of liquidity can lead to inflationary pressures and can pose risks to financial stability. The 10% ICRR can act as a non-disruptive way of dealing with this issue.

Temporary Nature of the Measure: Governor Shaktikanta Das emphasized that this is a temporary measure, set to be reviewed on or before Sept. 8. This ensures that it's a controlled experiment, without long-term monetary policy implications.

Ensuring Adequate Liquidity: Despite the temporary ICRR, the Governor assured that there will be adequate liquidity in the system to meet the credit needs of the economy. This assures that the regular functioning of the banking system won’t be hindered.

Avoiding a Direct CRR Hike: A direct hike in the regular CRR would have signaled a more significant policy shift. The temporary nature of the ICRR allows the RBI to manage liquidity without stirring up monetary policy debates.

What is the impact on the banking sector? The immediate impact of this announcement is likely to be a marginal rise in short-term lending rates. However, the longer-term impact might be minimal given the temporary nature of this measure. The banks are likely to continue their regular operations, and the temporary tightening of liquidity might not impact their lending practices significantly.

Inflation Outlook

Headline Inflation Remains a Concern: With the headline inflation staying above the target, RBI remains focused on aligning inflation with the 4% target. Factors such as a spike in vegetable prices, particularly tomatoes, and uneven rainfall distribution are adding to the near-term inflationary pressures. However, these are likely to correct with fresh market arrivals.

Core Inflation Stabilizing: The non-food, non-oil part of inflation, though sticky, has remained in the range of 5.5% to 6.1% in the last few months. This gives the central bank some room to hold rates steady.

Impact of Global Factors: Volatility in global financial markets, potential actions by the US Federal Reserve, and geopolitical tensions also influence the inflation outlook. The challenge of managing recurring food price shocks has been emphasized by RBI Governor Shaktikanta Das.

Positive Economic Momentum: The economy shows resilience, with real GDP growth projected at 6.5% for 2023-24 and 6.6% for Q1FY25. The revival in kharif sowing, robust government expenditure, and normalization of supply chains are promising signs.

Challenges Remain: Weak global demand, geopolitical tensions, and geoeconomic fragmentation pose risks to the growth outlook. RBI will be closely monitoring these factors to maintain economic stability.

Food Inflation Concerns

Weaker monsoon rains and flooding have led to a surge in food prices, driving retail inflation to a three-month high of 4.81% in June. This raises questions about whether food inflation could breach the RBI's target range and put additional pressure on households and the broader economy.

There are other challenges as well. Climbing crude prices, with the oil basket averaging $85.76 a barrel in August, adds another layer of complexity. As the world's third-largest consumer of oil, India could face further inflationary pressures, making imports costlier. Swap pricing indicates that traders are contemplating a potential rate hike in future policy meetings.

High-frequency indicators show a buoyant Indian economy. With elections coming up next year, maintaining growth momentum will be critical for the RBI, even as it has to balance the inflationary pressures. Particularly driven by the surge in food prices, it's essential to zoom in on a specific aspect that has caught everyone’s attention.

Tomatonomics: A Tale of Indian Farmers' Triumphs and Troubles

The recent surge in the prices of onion and tomato has caught the attention of households, traders, and market observers in India. So far, the wholesale price of onions has risen to ₹16-20 per kg, and the retail price has reached ₹30-35 per kg. A week ago, the wholesale and retail prices were ₹12-15 and ₹25-30 respectively. The wholesale price of tomatoes remains at ₹90-120 per kg, with retail prices between ₹160-200 per kg. In the case of tomatoes, every year, during July to November, an upward pressure is observed on the prices of tomatoes in India, with the pressure remaining highest in July. Here are some of the major price shocks in Tomatoes over the last 8 years -

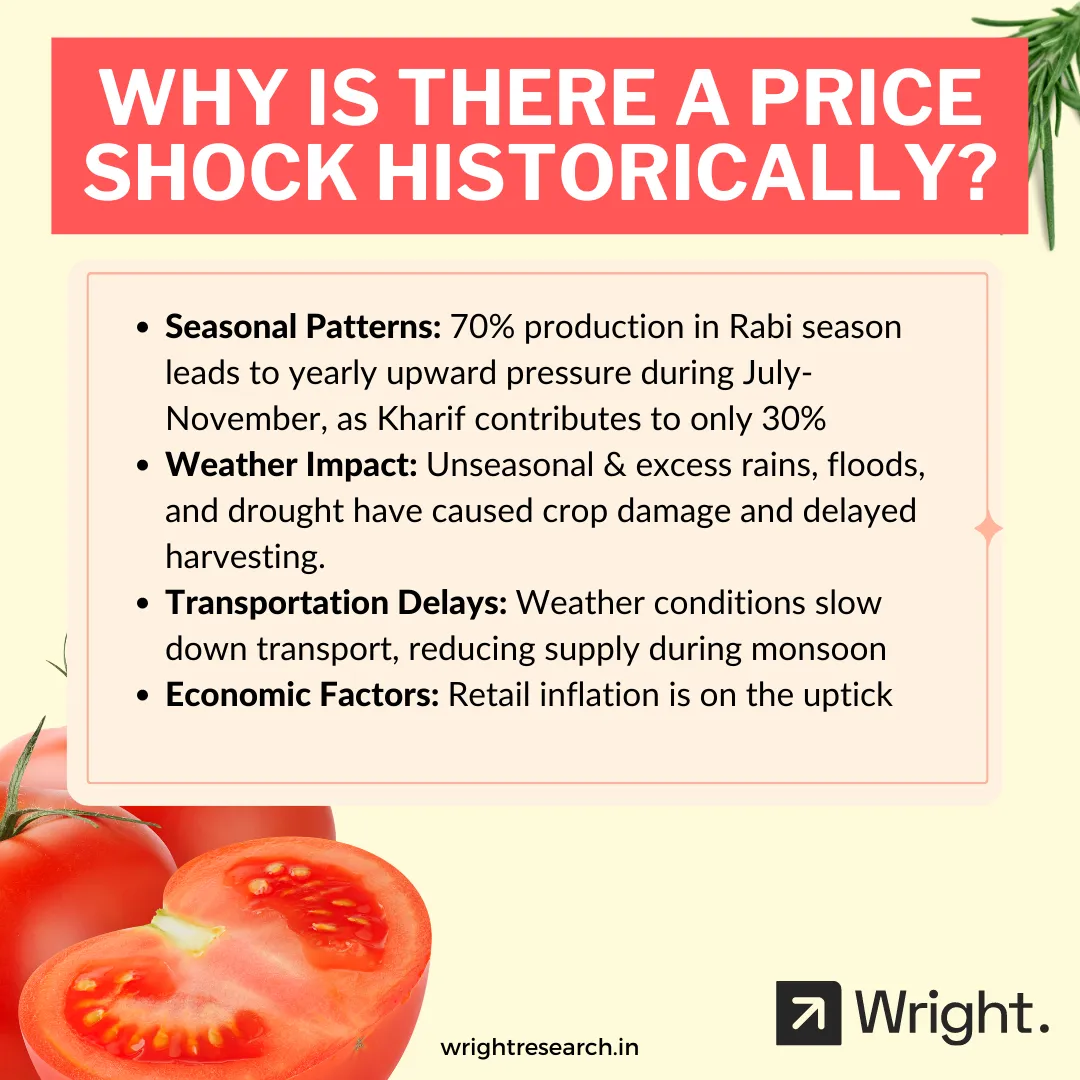

The question is, why is there a price shock nearly every year? There are a few structural reasons why this happens every year -

Seasonal Patterns: 70% production in Rabi season leads to yearly upward pressure during July-November, as Kharif contributes to only 30%.

Weather Impact: Unseasonal & excess rains, floods, and drought have caused crop damage, rotting and delayed harvesting.

Transportation Delays: Weather conditions slow down transport, reducing supply during monsoon

Economic Factors: Retail inflation is on the uptick.

All of this leads to an inevitable short term demand and supply gap which leads to a surge in prices. But, what happened this year?

All of this leads to an inevitable short term demand and supply gap which leads to a surge in prices. But, what happened this year?

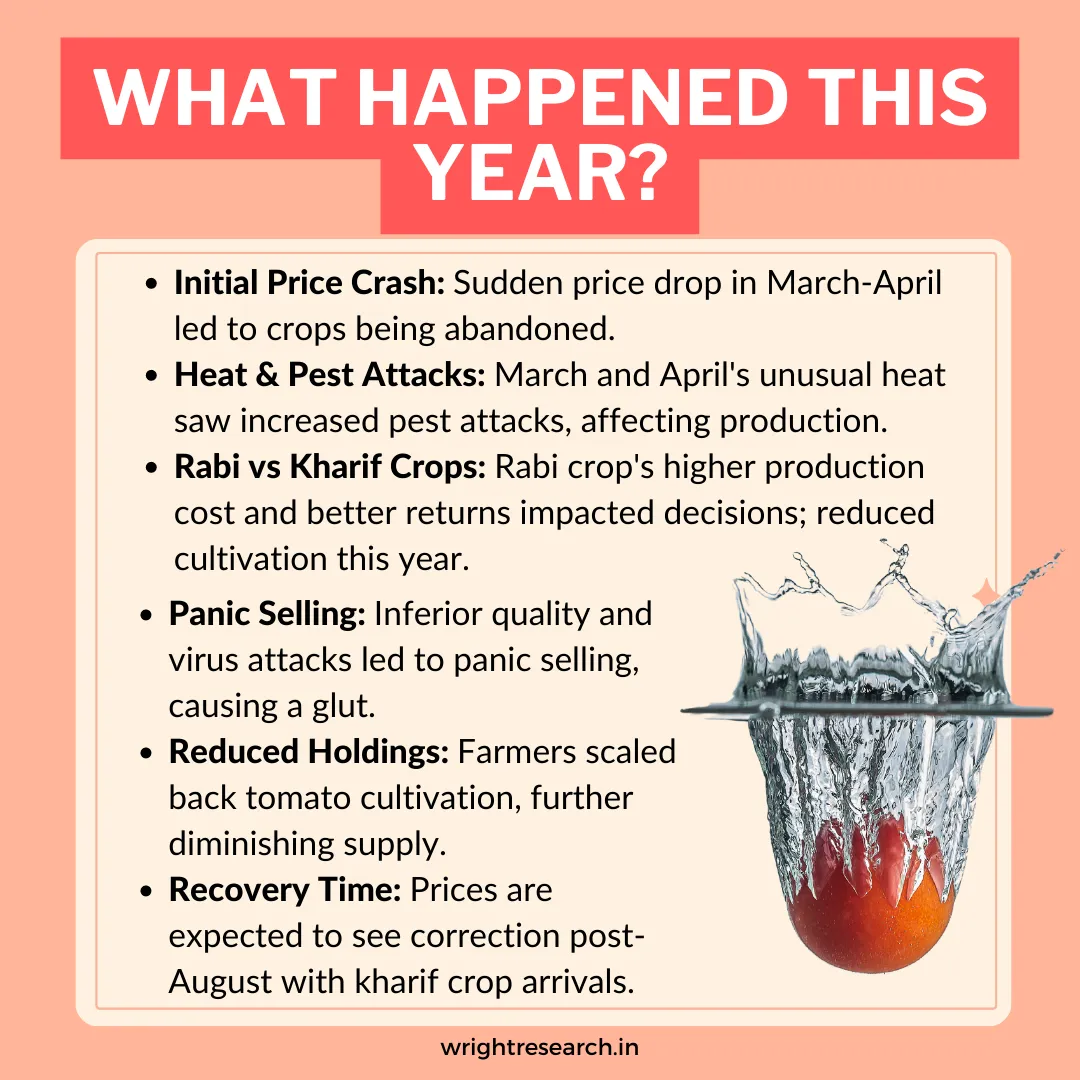

In March-April, the market faced a glut due to overproduction and farmers resorting to panic selling. This was exacerbated by the presence of inferior quality crops and a collapse in prices. Consequently, many farmers abandoned their crops following a price crash. Some farmers also reduced their tomato holding, with certain regions reporting significantly lower rabi tomato cultivation compared to previous years. As the year progressed, excessive heat and attacks by leaf curl and cucumber viruses devastated the crops in South India and Maharashtra, leading to inferior quality and a decrease in production. The rabi crop also fetches better returns, but the price collapse forced farmers to sell at much lower rates. This led to a significant reduction in plantation and an eventual rise in prices.

According to farmers and experts, the chances of prices softening are slim in the near future. The next crop will be the kharif tomato, and it is only post-August that arrivals will improve, and retail prices may see correction.

How Farmers are earning better margins than corporate india?

There are many farmers that had to face natural calamities such as floods and pest attacks. These uncontrollable factors have rendered many homeless and destroyed their crops. The profits being earned by tomato farmers is akin to a lottery, where only the lucky few reap the benefits. The grim reality remains that agriculture is a high-risk, low-return venture for the majority of farmers.

In the world of tomatoes, farmers are enjoying prices ten times the usual rate for their tomato produce. The cost of cultivation varies, but even at the upper range, farmers are making a killing with retail prices exceeding Rs 200 per kg.

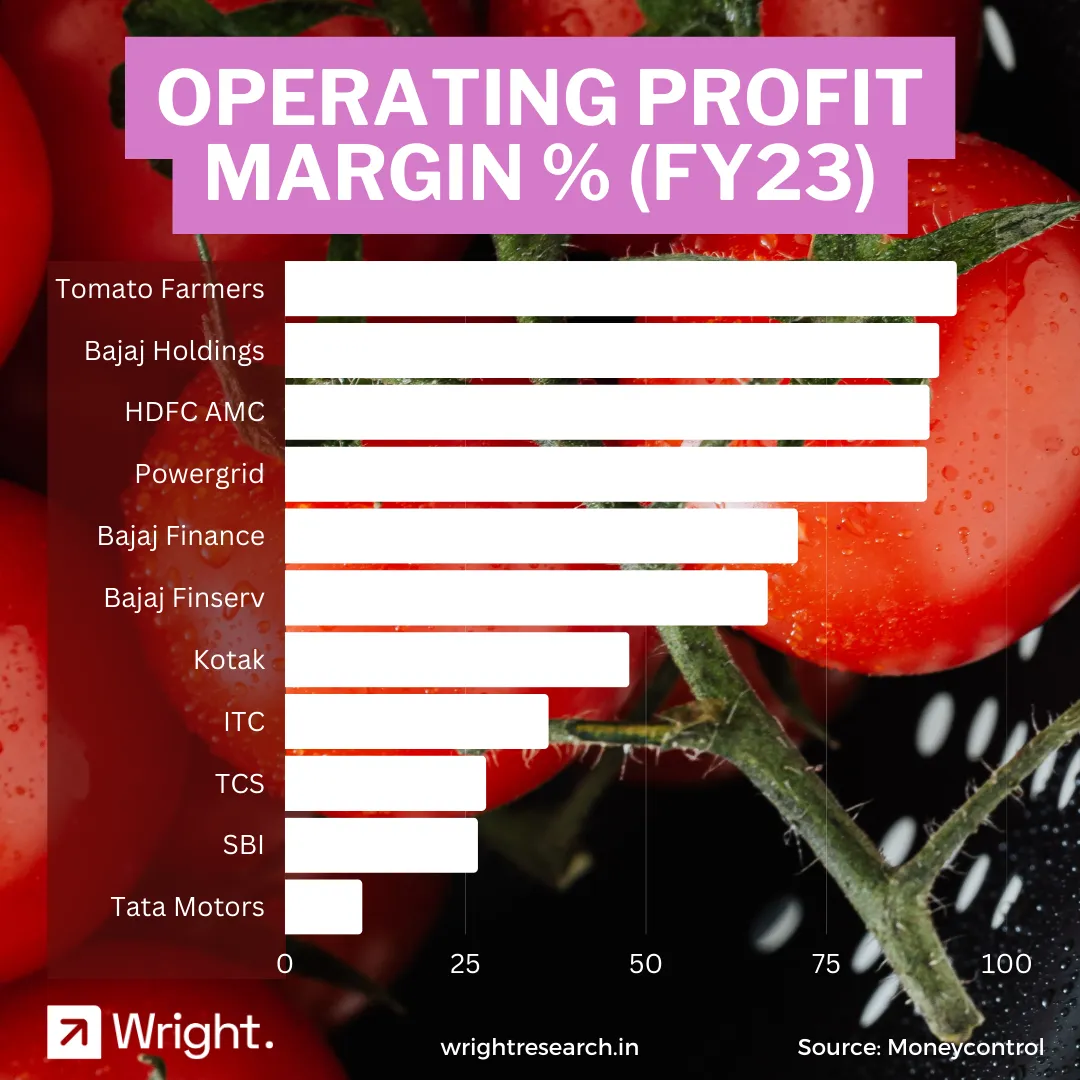

In financial terms, the economics of tomato cultivation has become incredibly attractive. Farmers who once faced crushing losses are now operating at profit margins that would make corporate giants envious. Even marquee names like HDFC, ITC, TCS, Tata Motors are being left behind in terms of operating profit margins.

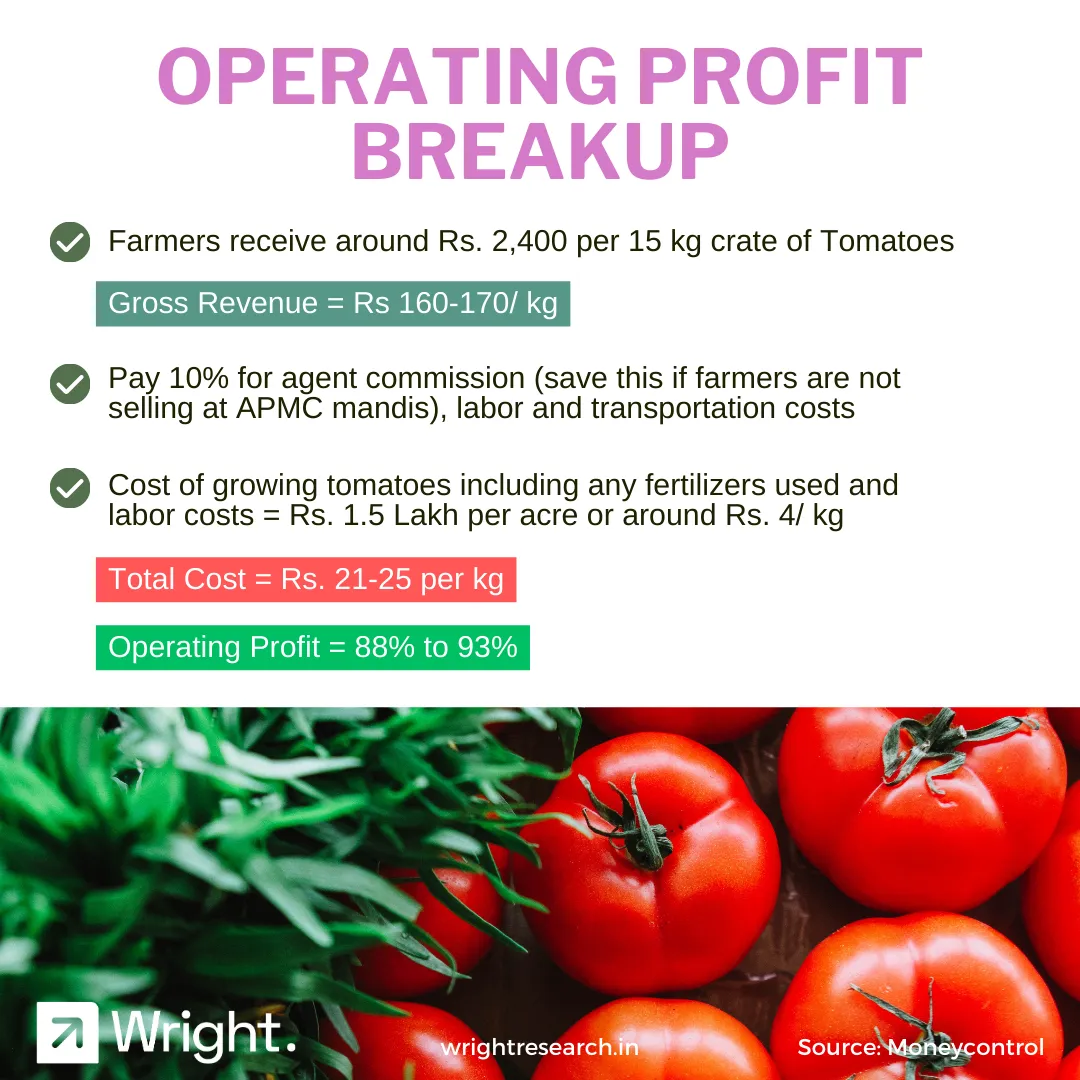

Here’s how Tomato Farmers are earnings nearly 93% operating profit margins -

Farmers receive around Rs. 2,400 per 15 kg crate of Tomatoes. Gross revenue works out to Rs.160-170/ kg

Farmers end up paying around 10% for agent commission, labor and transportation costs. Farmers that are not selling at APMC mandis save the agent commission

Cost of growing tomatoes including fertiliser, manure, labor costs and more amount to about Rs.1.5 Lakh per acre or around Rs. 4/kg

The total cost works out to about Rs. 21-25/ kg resulting in an operating profit margin of 88% to 93%.

What’s next?

The cost of a vegetarian thali in India rose by 28% in July, with a significant contribution from the price of tomatoes alone. The ripple effect is also being felt in other vegetables and spices. Consumers are unlikely to find relief from these high rates, especially as tomatoes are predicted to touch ₹300 per kilogram in the coming days. The situation with onions is equally dire, with prices expected to escalate further.

Is there any relief for consumers? There is typically a stabilization in prices with the arrival of Kharif crops in October. But the fluctuations in the agriculture sector do reveal a larger issue of instability and unpredictability.

What about the broader economy? The growth outlook for the economy appears positive and resilient with sustained momentum. Factors such as the recovery in kharif sowing and rural incomes, a thriving services sector, and consumer optimism are expected to bolster household consumption. Q1 earnings and financials have largely done well, not just in India but in the US also. The financial stability marked by healthy balance sheets in banks and corporations, along with supply chain normalization, business confidence, and strong government capital expenditure, is setting the stage for a broad-based renewal of the capital expenditure (capex) cycle.

However, the outlook is not without risks, as potential headwinds include weak global demand, volatility in international financial markets, geopolitical tensions, and geoeconomic fragmentation. Overall, the growth prospects seem promising but are tempered by potential external challenges.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox