International mutual funds are investment vehicles that allow Indian investors to build a diversified mutual fund portfolio by investing in overseas markets. These funds offer portfolio risk management through global exposure, provide capital preservation via diversification, and serve as an alternative investment portfolio option. Popular options include international equity funds, global index funds, and US mutual funds India, each offering different risk-return profiles for investors seeking high return mutual funds.

Introduction

You've built a decent emergency fund. Your savings account is growing. But somewhere in the back of your mind, there's a nagging question: "Is investing only in India enough?" If your portfolio is entirely concentrated in Indian equities or fixed deposits, you're missing out on growth opportunities that exist across the world. Many investors feel trapped between the comfort of what's familiar and the desire to explore global markets. That's exactly where international mutual funds enter the picture.

In this comprehensive guide, we'll explore how international mutual funds work, unpack India's tax rules on global investments, and help you decide whether building an international equity fund position makes sense for your wealth goals.

What are International Mutual Funds?

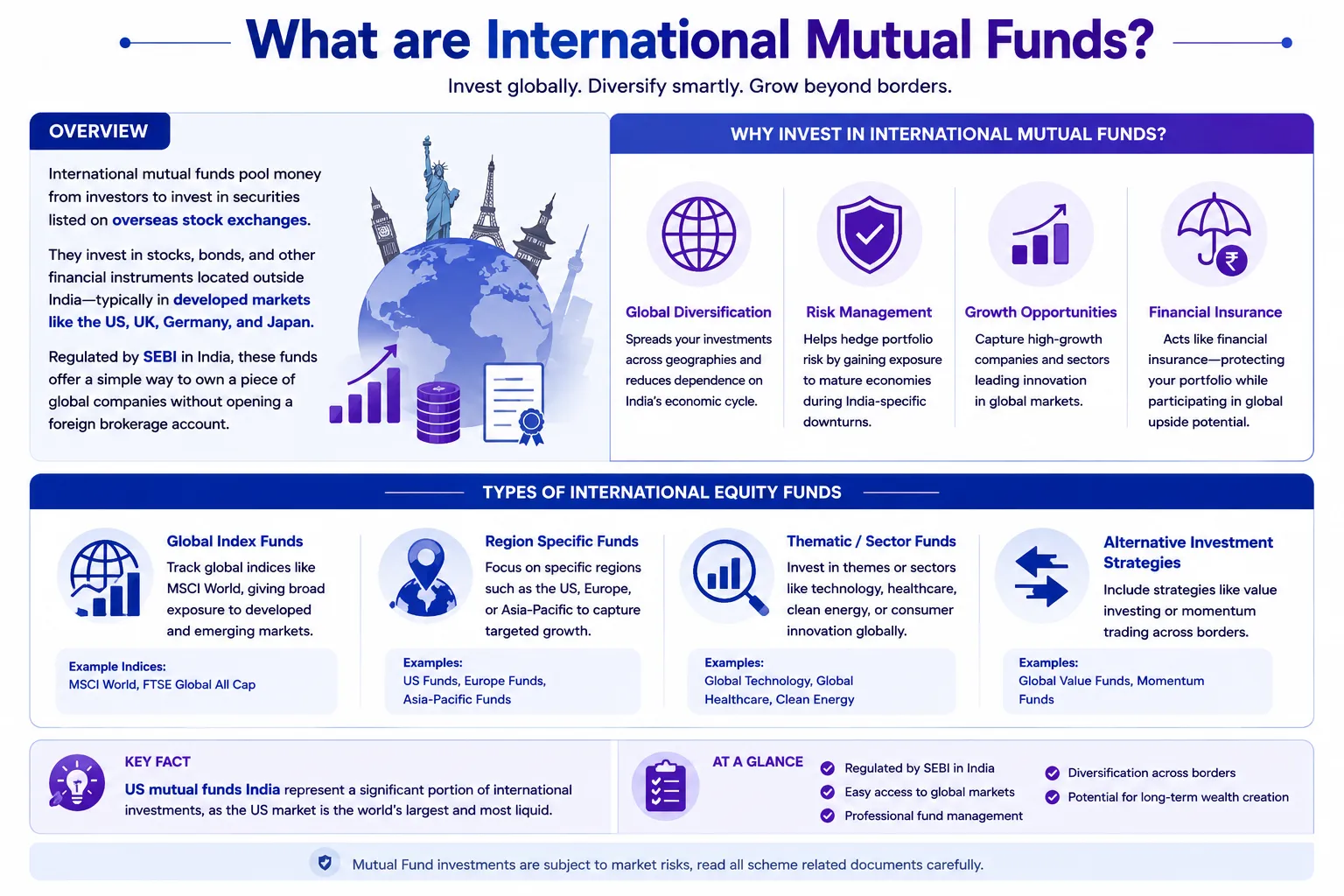

International mutual funds are investment schemes that pool money from investors to purchase securities listed on overseas stock exchanges. These funds invest your capital in stocks, bonds, and other financial instruments located outside India—typically in developed markets like the US, UK, Germany, and Japan. An international mutual fund is regulated by SEBI in India, but gains its returns from foreign market movements. It's your gateway to owning a piece of global companies without physically opening a foreign brokerage account.

The primary appeal lies in creating a diversified mutual fund portfolio that spans geographies. Instead of betting entirely on India's economic growth, you're hedging your portfolio risk management strategy by gaining exposure to mature economies with different economic cycles. Think of it as your financial insurance against India-specific downturns while capturing upswings in global markets.

There are several types of international equity funds available to Indian investors: some track global index funds that mirror worldwide market indices, others focus on specific regions (US, Europe, Asia-Pacific), and some pursue alternative investment portfolio strategies like value investing or momentum trading across borders. Among these, US mutual funds India represent a significant portion since the US market is the world's largest and most liquid.

How International Mutual Funds Work

The mechanics of international index funds are straightforward, though the underlying operations are complex. When you invest in an international mutual fund, your money flows into a pool managed by professional fund managers. These managers use your collective capital to purchase foreign securities typically stocks of multinational corporations, government bonds, or index-tracking instruments.

Here's the process broken down:

Step One: Investment & Currency Conversion

You invest rupees into the scheme. Your money gets converted into foreign currency (usually US dollars) at prevailing exchange rates. The fund manager then uses these foreign currency funds to purchase securities on overseas exchanges.

Step Two: Portfolio Construction

Fund managers construct a portfolio aligned with the scheme's objective. An international index fund might replicate the Nasdaq 100 or MSCI World Index. Meanwhile, an actively managed international equity fund applies manager expertise to select specific stocks, aiming for high return mutual funds performance.

Step Three: Currency Management

Unlike domestic mutual funds, international schemes deal with currency fluctuations constantly. When foreign assets appreciate, but the rupee strengthens against those currencies, your rupee-denominated returns could be dampened. Conversely, rupee depreciation can enhance your rupee returns. These currency dynamics become part of your overall portfolio risk management equation.

Step Four: Dividend & Return Distribution

As foreign holdings pay dividends or appreciate, these gains accrue to the fund. The fund then declares dividends or enables growth through NAV appreciation, which you can redeem at prevailing NAV prices.

International Mutual Funds in India: Key Facts & Data

According to SEBI data as of March 2026, the Indian mutual fund industry's overseas exposure through international schemes has grown significantly. There are currently over 45 active international mutual funds available to retail investors in India, collectively managing over ₹85,000 crore in assets. This represents a 23% year-over-year growth in this category.

Comparison Table: International vs Domestic Mutual Funds

Parameter |

International Mutual Funds |

Domestic Equity Mutual Funds |

Minimum Investment |

₹500–₹5,000 |

₹100–₹500 |

Regulatory Authority |

SEBI (India) + Foreign Regulators |

SEBI (India) |

Currency Risk |

Yes |

No |

Tax Treatment |

FPI tax rules apply |

Long-term capital gains tax (20%) |

Typical Returns (10-year avg) |

12–16% |

13–18% |

Best For |

diversified mutual fund portfolio |

Domestic concentration plays |

Liquidity |

High |

High |

The US market dominates international mutual funds available to Indian investors, accounting for nearly 65% of overseas exposure. This makes sense given the US market's size, stability, and the presence of global technology giants. US mutual funds offer both index-tracking options (like those mimicking the S&P 500) and actively managed variants.

According to AMFI data, investors deploying capital into international index funds have seen 10-year returns in the range of 13–15% annualized returns, driven primarily by US equity market performance. However, currency movements have created periods where capital preservation became more important than aggressive growth. In years when the rupee depreciated sharply (2022–2023), international equity funds delivered outsized returns to Indian rupee investors.

Tax Treatment of International Mutual Funds

This is where many investors stumble. International mutual funds in India are taxed differently from domestic schemes, and the tax structure has changed multiple times since 2018.

Current Tax Structure (as of FY 2025-26):

Long-Term Capital Gains (LTCG): If you hold an international equity fund for more than 24 months, gains are taxed at a flat 20% plus applicable cess. This is significantly lower than short-term gains.

Short-Term Capital Gains (STCG): If you sell within 24 months, gains are added to your income and taxed at your slab rate, potentially as high as 42.94% (including cess) for high earners. This makes high-return mutual funds less attractive if you're trading frequently.

Currency Gains: Notably, if you invest in US mutual funds India and the rupee depreciates, the currency component of your gain is taxed separately under the capital gains rules. This can become complex during volatile currency periods.

Dividend Distribution Tax (DDT): When an international mutual fund distributes dividends, a 20% flat tax (plus cess) applies before the dividend reaches your account. This makes growth-focused international index funds more tax-efficient than dividend-distributing variants for most investors.

Reinvestment vs. Redemption Strategy: For building a diversified mutual fund portfolio, choosing growth plans (reinvestment) over dividend plans helps defer tax until redemption, improving your post-tax returns.

Who Should Consider International Mutual Funds?

The Long-Term Wealth Builder: You're 35 years old with a 25-year investment horizon. Your domestic portfolio is steady, but you want to hedge against India-specific risks. An alternative investment portfolio approach using international equity funds allows portfolio risk management across geographies. Investing ₹5,000 monthly in a global index fund through SIP ensures you benefit from global growth while staying disciplined.

The Diversification Seeker: You've made solid returns in Indian mid-caps, but you recognize the concentration risk. Building a diversified mutual fund portfolio that includes international mutual funds reduces your exposure to India-specific downturns. Economic recessions in Europe or Asia-Pacific slowdowns won't wipe out your entire wealth.

The Early Retiree: You plan to retire abroad or want foreign currency reserves for future overseas expenses. International mutual funds offer capital preservation in a foreign currency while providing growth. An international index fund mimicking global indices provides steady growth without active management overhead.

The Tax-Efficient Investor: High earners benefit from the 20% LTCG tax on international equity funds versus 42.94% STCG rates. For rupee-neutral portfolios seeking high-return mutual funds, the tax efficiency often makes US mutual funds India attractive even after currency considerations.

How to Build a Diversified Mutual Fund Portfolio with International Funds

Wright Research advocates a systematic approach to adding international mutual funds to your portfolio. Rather than timing the market or making lump-sum guesses, a factor-based approach works better.

Step One: Assess Your Current Exposure

Calculate what percentage of your wealth is currently invested domestically versus internationally. If you're entirely in India, starting with a 15–25% allocation to international mutual funds is prudent. This provides meaningful portfolio risk management without overexposure to currency risk.

Step Two: Choose Your Category

Decide between international index funds (passive, low-cost) or actively managed international equity funds. For first-time investors, international index funds tracking the MSCI World Index or S&P 500 provide simplicity and low costs. This suits investors seeking high-return mutual funds without paying active management fees.

Step Three: Set Up Regular Investment

Rather than investing ₹10 lakhs today, use SIPs (Systematic Investment Plans). Investing ₹10,000 monthly in US mutual funds India over 10 years smooths out currency fluctuations and builds a diversified mutual fund portfolio methodically. This approach embeds capital preservation via averaging.

Step Four: Review Quarterly, Don't Panic

Markets move. Currency fluctuates. Your international mutual fund NAV will sometimes dip. Review performance quarterly, but resist selling during short-term dips. The tax penalty (STCG) alone makes this costly.

International Mutual Funds vs Domestic Alternatives

Detailed Comparison Table

Criteria |

International Mutual Funds |

Domestic Equity Mutual Funds |

Direct Foreign Stocks |

Ease of Investment |

Simple (single transaction) |

Simple |

Complex (foreign account needed) |

Cost |

0.5–1.5% expense ratio |

0.4–1.5% expense ratio |

Brokerages + currency costs |

Currency Risk |

Yes |

No |

Yes |

Tax Treatment |

20% LTCG |

20% LTCG |

20% LTCG |

Diversification |

Instant (global basket) |

Sector-specific |

Individual stock risk |

Best For |

diversified mutual fund portfolio |

Domestic plays |

Experienced investors |

An international equity fund provides instant global diversification without needing to research individual foreign stocks. An alternative investment portfolio using international index funds costs less than direct stock ownership while providing better portfolio risk management through diversification. Meanwhile, domestic funds are ideal if you're bullish on India and want focused exposure. Most investors benefit from holding both—a diversified mutual fund portfolio of 60% domestic and 40% international mutual funds represents a balanced capital preservation and growth approach.

How to Get Started with International Mutual Funds in India

Getting started is simpler than you think. Many brokers, including those who partner with Wright Research's ecosystem, offer seamless access to international mutual funds.

Step One: Choose Your Platform

Open an account with a mutual fund distributor or directly with asset management companies offering international equity funds. Your existing brokerage (Zerodha, Paytm, etc.) likely supports these.

Step Two: Select Your Fund

Browse the best international mutual funds using filtering on platforms like AMFI's website or your broker's app. Compare expense ratios, performance, and fund manager tenure. For simplicity, start with an international index fund.

Step Three: Complete KYC & Invest

Provide necessary documentation (PAN, address proof, bank details). Set up a SIP for ₹5,000–₹10,000 monthly, or make a one-time investment if you have lump-sum capital.

Step Four: Monitor & Rebalance

Track your international mutual fund performance quarterly. If international holdings grow beyond your target allocation (say, 40%), rebalance by investing more domestically. This maintains your portfolio risk management strategy.

Wright Research's quant-based approach suggests that factor-based international equity funds (those screening for quality, momentum, or value signals) often deliver higher return mutual funds outcomes than pure market-cap weighted global index funds, particularly over 7+ year horizons.

Conclusion

International mutual funds represent a logical step for investors seeking capital preservation through diversification and exposure to global growth. By building a diversified mutual fund portfolio that includes international equity funds or global index funds, you implement effective portfolio risk management across geographies. Whether you choose passive international index funds or active international mutual funds depends on your preference for costs versus the potential high return of mutual funds performance.

The tax framework, while complex, favors long-term holding. Starting with US mutual funds, India, or global index funds as an alternative investment portfolio component ensures you capture global growth while staying grounded in Indian tax compliance. Over 10–15 year horizons, international mutual funds have consistently delivered returns comparable to or better than domestic options, particularly when currency tailwinds exist.

The best time to start isn't when the rupee is at its weakest or when US markets are booming; it's today, through disciplined SIPs.

FAQs

1. Are international mutual funds riskier than domestic funds?

Both carry risks, but different types. International mutual funds face currency volatility plus foreign market risk. Domestic funds face India-specific risks. A diversified mutual fund portfolio combining both reduces overall portfolio risk management through uncorrelated assets. Over long periods, international equity funds have proven as stable as domestic variants.

2. How is currency handled in international mutual funds?

International mutual funds automatically handle currency conversion when you invest and when you redeem. Currency gains (if the rupee weakens) or losses (if the rupee strengthens) are embedded in your NAV returns. You don't actively manage currency; the fund does.

3. Can I start investing in international mutual funds with ₹500 monthly?

Absolutely. International mutual funds accept SIP investments as low as ₹500 monthly. Starting small builds discipline and lets you experience currency fluctuations firsthand. Over 10–15 years, ₹500 monthly becomes significant due to compounding.

4. Should I invest in US mutual funds or diversified international funds?

US mutual funds in India are attractive given market dominance, but global index funds offer diversification. Consider your portfolio's current geography. If you already own India-exposed assets, a global index fund provides better diversification. If you're underweight US tech, a dedicated international equity fund focusing on the US makes sense.

5. What's the difference between international dividend and growth funds?

Growth funds reinvest dividends, deferring taxes until you sell. Dividend funds distribute earnings, triggering immediate 20% DDT. For capital preservation and long-term wealth, growth plans are more tax-efficient. Choose dividend plans only if you need regular income.

6. How do I handle taxes on international mutual fund gains?

Track your purchase date and redemption date. Gains within 24 months are taxed at your income slab rate (STCG). Gains beyond 24 months attract a flat 20% LTCG tax plus cess. Keep statements ready for tax filing. Using a tax software like ClearTax or consulting your CA simplifies this.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox