India is fast becoming a pivotal hub in global chemical manufacturing. This transformation is driven by robust domestic consumption, strategic global shifts, and the nation's competitive advantages, making India an attractive destination for chemical sector investments.Let's look at the Indian chemical industry in depth today.

Globally Chemicals Has Lagged

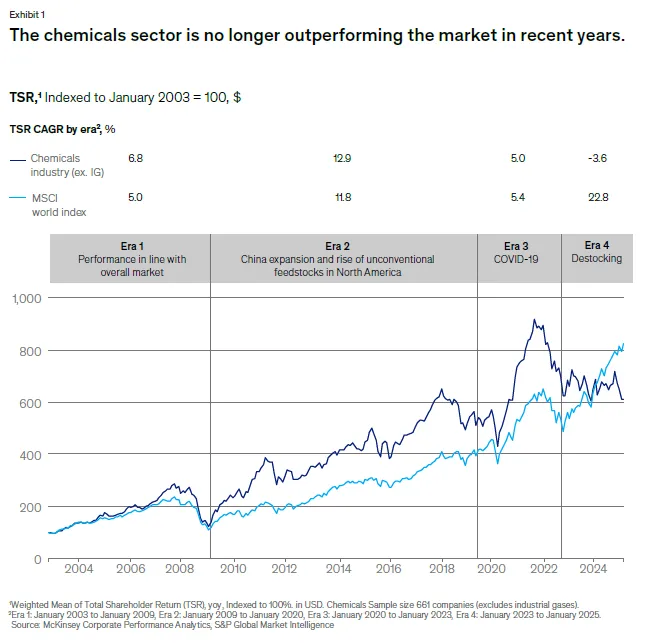

Globally, the chemical industry has witnessed significant volatility, especially in recent years. While the sector traditionally outperformed broader markets, recent years have presented multiple challenges, including the aftermath of the COVID-19 pandemic, fluctuating demand, geopolitical tensions, supply chain disruptions, and increased regionalization.

Returns dropped to -3.6% between January 2023 and January 2025, starkly contrasting the MSCI World Index, which saw a 22.8% increase in the same period. The variability in performance across different chemical segments underscores a shift toward specialty chemicals, which have proven relatively resilient compared to base and diversified chemicals.

Indian Chemical Industry Stocks Performance

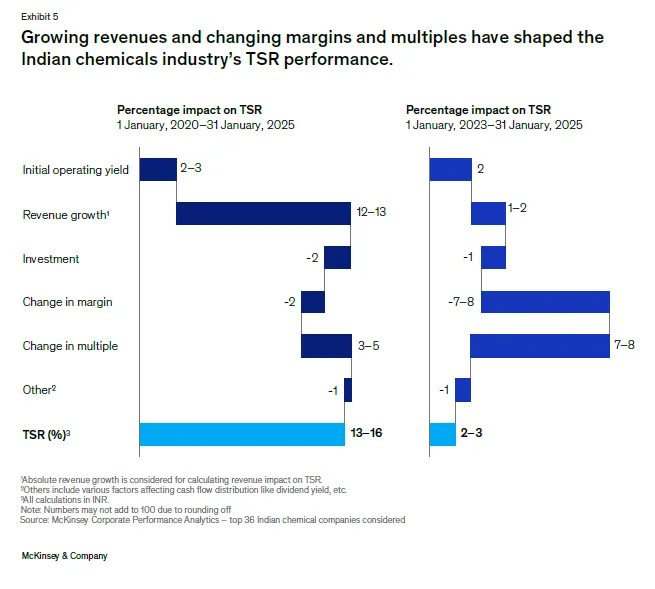

Despite global headwinds, the Indian chemical industry has shown substantial resilience, becoming Asia's standout performer with a return of 10-12% from January 2020 to January 2025. This growth was primarily fueled by recovery growth following the disruptions caused by the COVID-19 pandemic. However, despite this upward trajectory, margins have steadily declined, resulting in flat returns between 2023 and 2025, peaking at about 17.5% in 2021 and subsequently declining to around 13% by 2024.

A deeper analysis of over 200 chemical companies indicates a slight revenue contraction of around 7% between fiscal years 2023 and 2024. EBITDA margins have shown volatility, initially increasing from about 16% in fiscal 2018 to peak at 17.5% in fiscal 2021, only to dip again to roughly 13% in fiscal 2024.

Within the chemicals sector, the specialty and petrochemicals segments demonstrated similar revenue growth rates, each hovering between 10.5% and 11% CAGR. However, margin trajectories within these segments have diverged significantly. Specialty chemicals witnessed a relatively moderate margin decline, falling from around 15.9% in fiscal 2018 to approximately 13.7% in fiscal 2024. Conversely, petrochemicals experienced a more pronounced and volatile shift in margins, reaching a high of 24% in fiscal 2021, boosted by post-pandemic recovery and favorable crude oil prices, before sharply declining to 8.6% by fiscal 2024 due to oversupply, weaker global demand, and rising crude prices.

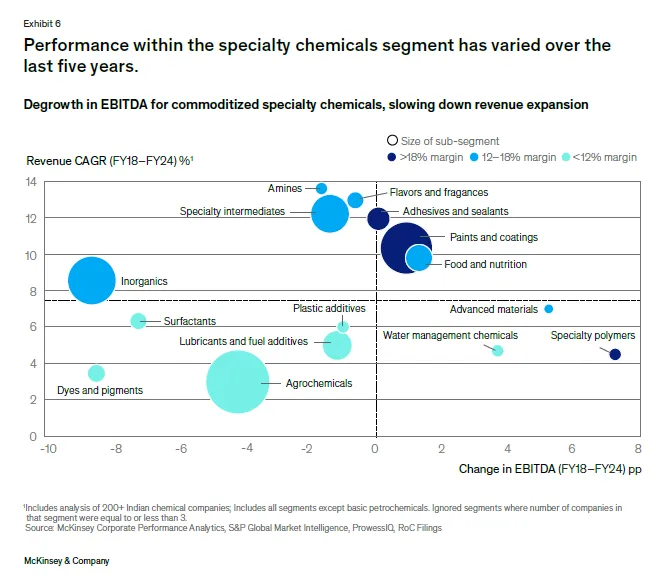

In the last 5 years specialty chemicals have notably outperformed petrochemicals in India. Segments like food and nutrition, flavors and fragrances, and adhesives and sealants displayed robust growth trajectories, while agrochemicals and plastic additives faced challenges including weak revenue and margin compression.

India’s Growth Trajectory For Chemicals

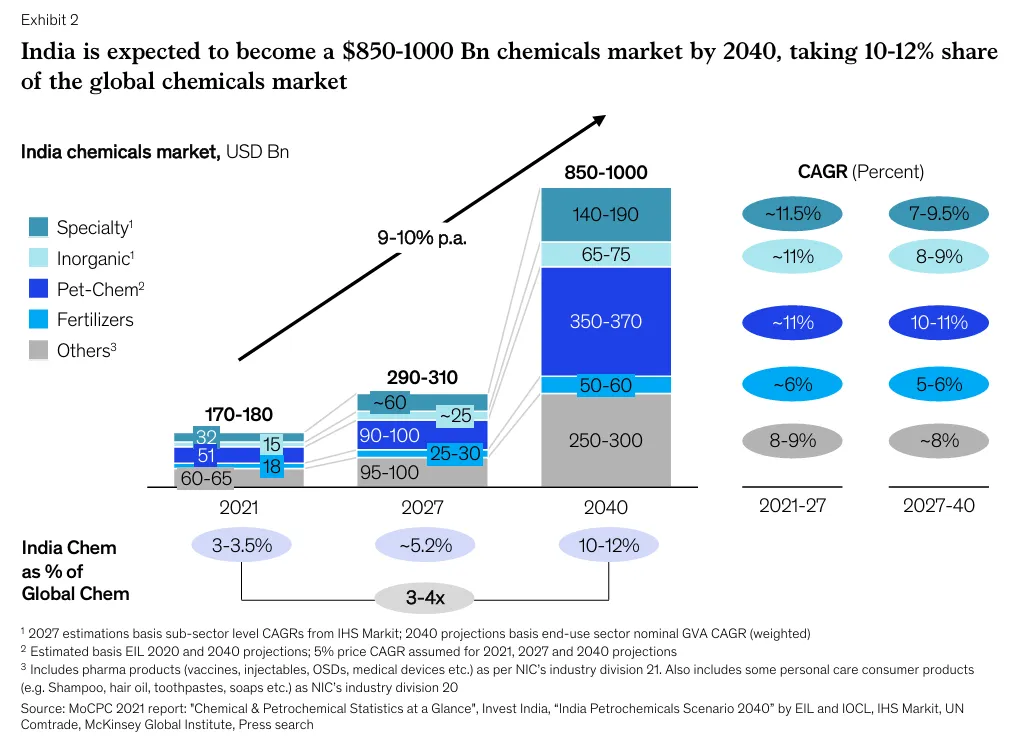

Overall the Indian chemical sector is positioned for extraordinary growth, projecting an expansion from approximately USD 178 billion in 2021 to about USD 850-1000 billion by 2040. India’s chemicals market could potentially account for 10-12 % of the global chemical market, propelled by a 9-10 % annual growth in domestic consumption.

Specialty chemicals play a significant role in this growth trajectory, poised to expand to USD 64 billion by 2025 CAGR of 12.4 %, fueled significantly by segments like dyes and pigments, agrochemicals, flavors and fragrances. It stand out as India’s sole sub-sector maintaining a trade surplus, positioning the country as a viable global supplier, especially in key subsegments such as flavors, fragrances, and food nutrition chemicals. The food and nutrition segment, driven by heightened consumer demand for premium and organic ingredients, has seen robust revenue and margin growth.

Additionally, segments like paints and coatings, flavors and fragrances, amines, and adhesives have expanded swiftly, buoyed by diversification and geographic reach. Nonetheless, these segments faced margin pressures due to raw material price volatility and competitive market dynamics. The paints and coatings segment notably benefited from growth in consumer durables, automobiles, and related sectors, while the amines segment grappled with fluctuating raw material costs.

On the other hand, sectors like agrochemicals, dyes and pigments, inorganic chemicals, and surfactants struggled due to weakened revenue streams and profitability constraints. Agrochemicals faced challenges from China's competitive re-entry into export markets, exacerbated by domestic demand dips linked to climatic events like El Niño. Dyes and pigments were impacted by diminished demand from textiles and plastics sectors and sharp input cost variations.

Inorganics, particularly chlor-alkali, encountered declining profitability after earlier highs driven by reduced European competition and Chinese market constraints. New capacity additions and intensified Chinese competition reduced utilization rates and compressed margins.

Segments experiencing commoditization, such as surfactants, recorded slower growth and tighter margins. Conversely, advanced materials, water management chemicals, and specialty polymers exhibited moderate revenue growth but improved EBITDA through technological advancements and product quality enhancements, highlighting the importance of consumer sentiment in driving specialty segments forward.

Drivers of Future Growth For Chemicals Industry

India's competitive edge in the chemical sector also arises from several crucial factors, including low operating costs, abundant labor, and effective strategic planning by businesses. Its labor costs remain among the lowest globally, complemented by competitive utility rates and robust EBITDA margins. Furthermore, Indian chemical companies excel in profitability, often achieving higher EBITDA per unit of investment compared to global peers. The operational cost disparity between India and China has narrowed significantly, enhancing India's attractiveness.

The Indian government has also facilitated this growth with impactful reforms and improved ease of doing business, which moved India’s global rank. Initiatives like PLI and Petroleum, Chemicals, and Petrochemicals Investment Regions (PCPIR) further bolster the sector's prospects. However, environmental clearances remain challenging, requiring significant time and capital investments. This regulatory bottleneck represents a key area needing improvement.

1. Building Platforms to Meet Domestic Demand

India’s domestic consumption and growing infrastructure investments offer opportunities to establish globally competitive chemical manufacturing platforms. Notably, electronic chemicals and battery chemicals are set to grow rapidly as investments in semiconductor fabs and electric vehicle (EV) adoption increase.

2. Expanding Global Presence

India's chemical exports rose significantly, from around $23 billion in 2015 to $39 billion in 2023. However, the country remains a net importer, suggesting untapped potential. Establishing physical presences in key international markets could enhance exports and deepen customer relationships.

3. Strategic Mergers & Acquisitions

While Indian chemical firms have traditionally leveraged mergers and acquisitions for domestic expansion and diversification, future strategies must focus on acquiring advanced technologies, enhancing R&D capabilities, and building global value chains through strategic international acquisitions.

4. Accelerating Sustainability Initiatives

Sustainability is emerging as a critical driver of growth, compelling chemical firms to explore renewable energy sources, bio-based chemicals, and circular economy solutions. Decarbonization efforts could significantly lower operational costs and emissions, boosting both sustainability and profitability.

5. Enhancing Capital Expenditure Management

With planned capital investments totaling approximately $11 billion over the next few years, improving project execution and strategic capital allocation is crucial. Addressing project delays and cost overruns—averaging around 19%—could significantly enhance investment returns.

6. Leveraging Digital Transformation

Adopting advanced digital technologies like artificial intelligence (AI), machine learning (ML), and digital twins can yield significant operational improvements, potentially increasing EBITDA by 6-8 percentage points. Digital interventions in manufacturing, procurement, supply chain management, R&D, and commercial functions can substantially enhance overall efficiency and profitability.

Conclusion

India's chemical sector is at a transformative juncture. Its favorable economic factors, proactive government initiatives, strategic geographic location, and significant domestic and international demand position India as a future global chemicals manufacturing hub. Businesses looking to invest or expand in India will find a dynamic market ripe with opportunities for substantial growth and global integration.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox