For 3 decades, Indian IT services ran on one equation. Take a task that costs a high hourly rate in New York or London, route it to an engineer in Bengaluru or Pune who costs a fraction of that, and keep the difference. Add more engineers, win more revenue. That model built a software export industry worth more than $280 billion and turned TCS, Infosys, Wipro, HCLTech and Tech Mahindra into some of the most valuable companies on the Indian market.

In early 2026, that equation came under public pressure. The trigger was a US AI company, and the question investors began asking was blunt: if software can increasingly write, test and maintain itself, what happens to an industry built on billing for human hours? Let's separates the market panic from the reality, and looks at what actually changed.

What triggered the selloff in Indian IT stocks?

In late January 2026, Anthropic expanded its Claude Cowork product and released plug-ins that let its AI agent perform real work across legal, sales, marketing and data analysis functions. The signal investors took from it was that AI had moved from assisting workers to doing the work itself. Global software stocks fell first. The fear then reached India.

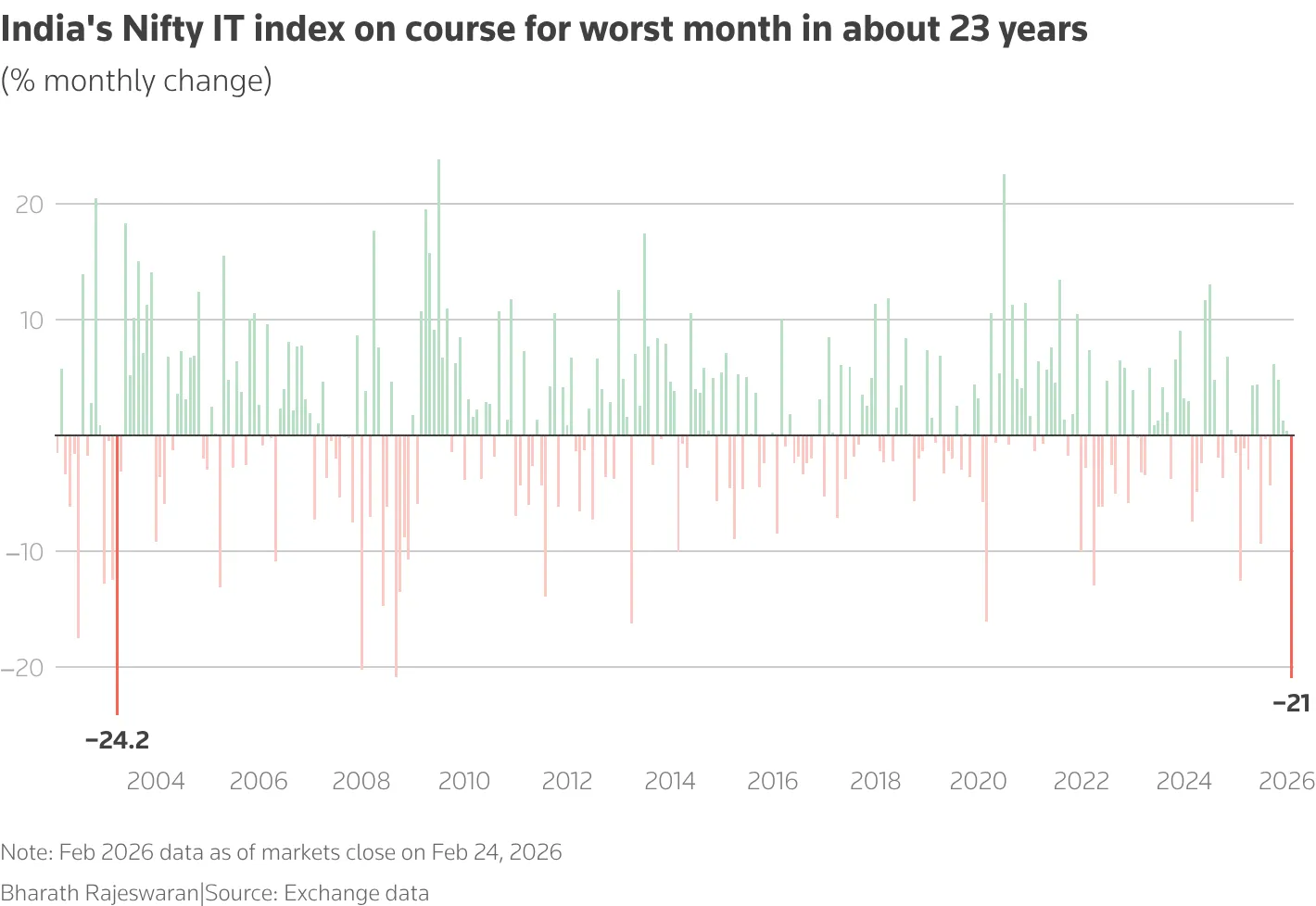

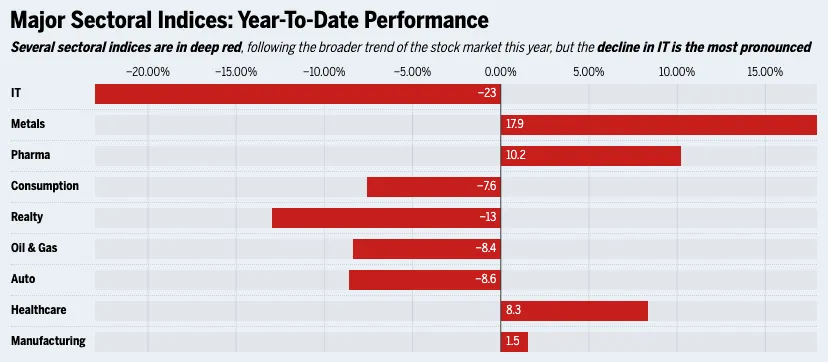

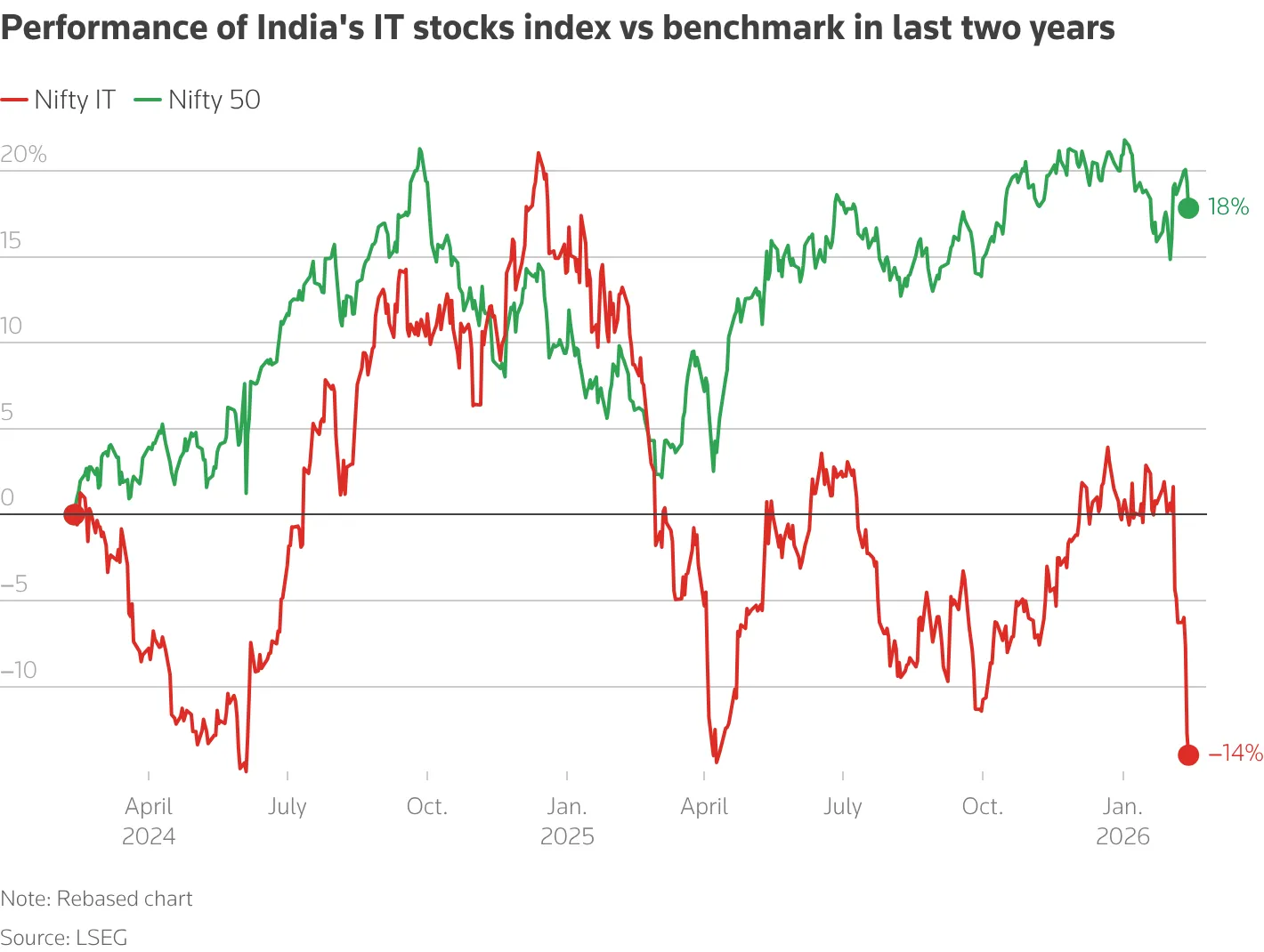

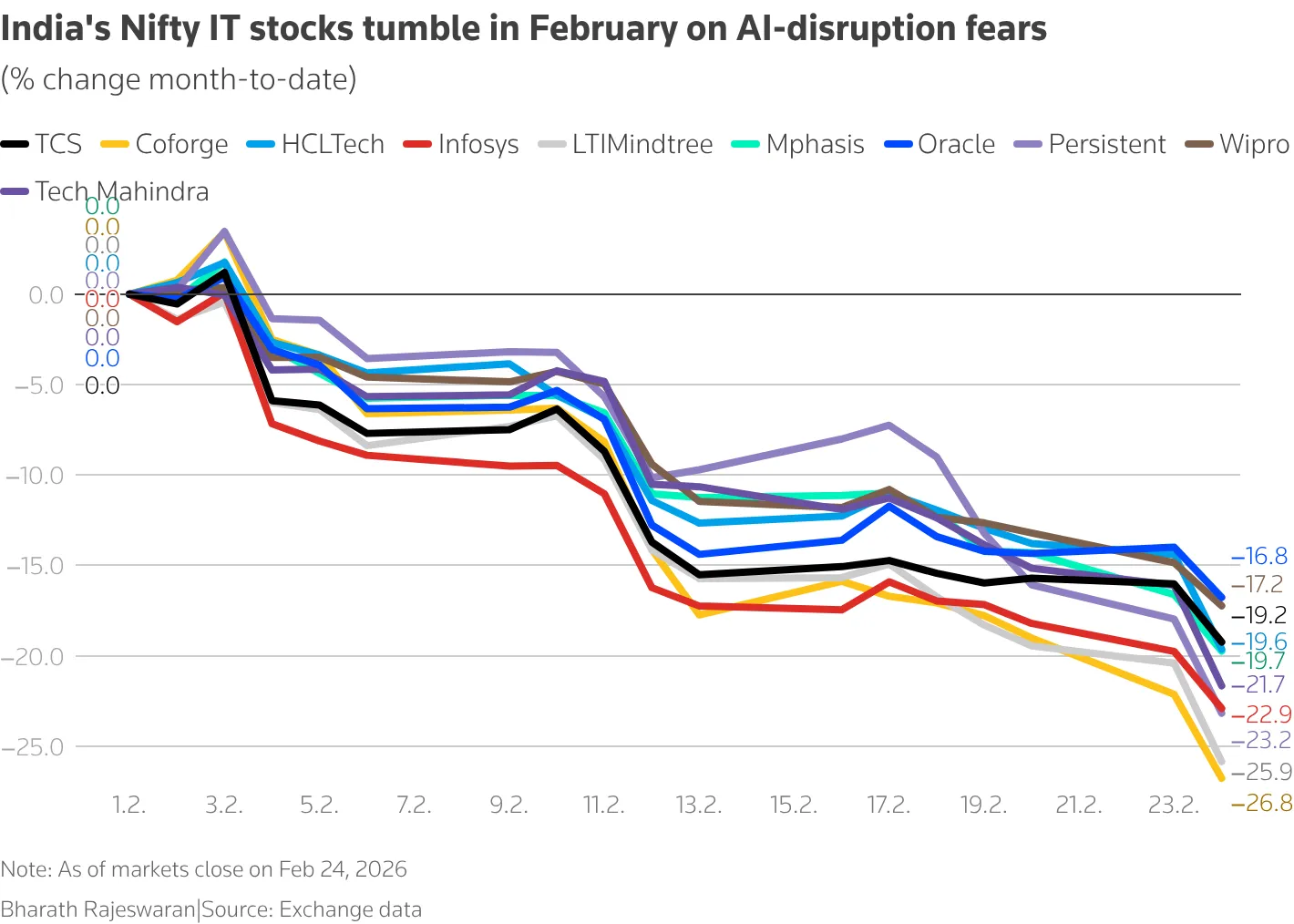

On February 4, the Nifty IT index recorded its worst single-day fall since March 2020, dropping about 6% and erasing close to 2 lakh crore rupees in value. Infosys led the decline at roughly 7.3%, with TCS, Wipro and HCLTech all falling sharply. The slide continued for days. By mid-February the index had dropped about 19% from its February 3 peak across eight trading sessions, and roughly $50 billion in market value was gone. Analysts gave the episode a name: the Anthropic shock.

Is Anthropic really worth more than India's entire listed IT industry?

Figure 1: Market value compared with annual revenue, February 2026.

On the surface, the numbers look impossible. After a $30 billion funding round in February 2026, Anthropic was valued at $380 billion. On the same dates, the combined market capitalisation of the 77 companies in the BSE IT index stood at about $351 billion. A company that earned its first dollar of revenue roughly 3 years earlier was worth more than every listed Indian IT firm put together.

The revenue picture runs the other way. Anthropic's run-rate revenue was around $14 billion. The 77 BSE IT firms together recorded close to $100 billion in revenue in FY25 and about $15 billion in profit. TCS alone reported revenue of about $28 billion, and Infosys about $18 billion. The market was paying far more for a company earning far less. That gap is the whole story in one picture: investors were pricing in expected disruption rather than current earnings.

Measure | Anthropic | 77 listed Indian IT firms |

|---|---|---|

Market value (Feb 2026) | About $380 billion | About $351 billion |

Annual revenue | About $14 billion (run-rate) | About $100 billion (FY25) |

Years since first revenue | About 3 | More than 25 |

Has AI actually hurt the companies' revenue and profits?

This is where panic and reality diverge. Through FY26, client bookings largely held up. Several firms grew. The damage so far has appeared in share prices and in the shape of future contracts, rather than in collapsing sales.

Management points to 2forces working at once. The first is plain macro caution. US clients have stretched out decision cycles and chosen smaller, contained projects over large transformation programmes. The second is AI itself, which is starting to compress the human effort each project requires. A note from Nirmal Bang Institutional Equities captured the tension neatly: managements talk up AI-led deal momentum, while the aggregate numbers stay restrained.

The valuation also looked stretched going into the fall. By mid-February 2026, the Nifty IT price-to-earnings ratio had eased to about 23.6, below its one-year average of 26.8 and its two-year average of 29.6. Part of the decline corrected high expectations. Part of it was a genuine repricing of the business model.

What part of the Indian IT model is actually breaking?

The clearest structural change is the link between revenue and headcount. For 3 decades, more revenue meant more engineers. In FY26, that link visibly loosened. HCLTech said its revenue had grown 4 to 5% over 2years while its headcount stayed flat, describing the shift as non-linearity. Mphasis reported the same de-linkage over several quarters.

The sharpest example came from Coforge, a mid-cap that grew revenue around 30% in FY26 while its employee cost base grew only about 20%. The gap between those 2lines is the change in one sentence: a unit of revenue is detaching from a unit of labour.

That carries a human cost. The major Indian IT firms together employ close to 2million people, and the wider sector employs about 5.8 million. HCLTech said productivity gains had released staff, and that workers in entry-level or lower-skill roles are not all easy to redeploy because automation now handles much of that work.

The pricing model is changing too

Pricing is moving away from the hourly rate card. HCLTech told clients it would use AI to cut their costs even where that meant lower revenue for itself, and said a contract that once carried a $100 million value now closes closer to $80 million. Tech Mahindra has begun describing work in service tokens, a unit borrowed from how AI models are priced, where the client buys an outcome instead of a number of hours. Infosys has pointed to outcome-based and team-based models as the likely successors. The common feature across all of them is the quiet disappearance of the billing rate.

The same change shows up as both discount and premium

FY26 produced a curious split. New AI-led work commanded premium pricing, because clients are still working out what it is worth, and several CFOs called AI accretive to margins. At the same time, savings from automating older work were handed back to clients in competitive deals, which made AI look deflationary. Both were true. They simply described different ends of the same book. HCLTech took the most cautious view, sizing the structural drag on its own portfolio at 2 to 3%, and walked away from deals it judged unprofitable, forgoing more than $1 billion in potential contract value to protect pricing.

How are the companies responding?

The firms are not standing still. The shared strategy is to move from selling labour to owning software, platforms and infrastructure. HCLTech has split its portfolio into 3 buckets, each with a different growth path, and frames the whole challenge as a race for the AI-native bucket to grow fast enough to outrun the shrinking one.

Category | What it covers | Direction |

|---|---|---|

AI-disrupted | Routine services that AI can automate | Shrinks 3 to 5% a year |

AI-amplified | Services made more productive by AI | Grows with the business |

AI-native | New AI platforms and advanced AI work | Targeted 25 to 30% growth |

Beyond reclassifying their books, the companies are making concrete bets. Wipro launched a dedicated AI-native business and platforms unit, describing the approach as services-as-a-software. TCS announced plans to build one gigawatt of data centre capacity through a venture called HyperVault, a striking figure given that India's total data centre capacity in early 2026 was roughly 1.4 gigawatts. HCLTech won a deal worth more than $100 million to build AI data centres for a global technology company, and its quarterly Advanced AI revenue reached $155 million.

A surprising growth area is the work of building and running AI itself. Both Wipro and Tech Mahindra now earn meaningful revenue training, fine-tuning and evaluating AI models for the very companies that make them. About a tenth of Tech Mahindra's business process services book is now this kind of work. The firms that AI was supposed to displace are being paid to help build it.

Why does this matter beyond the stock market?

Indian IT is a pillar of the national economy. It contributes about 7.3% of GDP, earned roughly $224 billion in services exports in FY25, and accounts for close to 58% of the country's total services exports. Cities such as Bengaluru, Hyderabad, Pune and Gurugram were reshaped by IT salaries, which feed housing, cars, retail and credit. A sustained slowdown in hiring or wages would spread well beyond the sector and into consumption and lending.

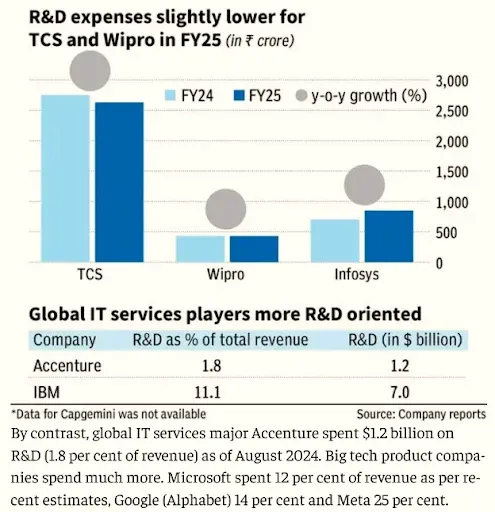

There is also a question of preparation. Between FY20 and FY25, India's top five IT firms returned about 4.8 trillion rupees to shareholders, equal to roughly 87% of their combined profits, with TCS distributing close to 99% of its earnings. Over the same period, the IT-software sector's share of corporate R&D spending in India fell from 4% to under 3%.

Global technology firms reinvest far more: Microsoft and Alphabet put 13 to 16% of revenue into research, and Meta more than 20%. Western firms largely chose to own technology platforms, while Indian firms chose to perfect the delivery model and return cash. In an AI cycle, owning the platform may matter more than executing on someone else's.

So, has AI broken Indian IT?

No, it has not broken the industry. The companies remain profitable, are still winning deals, and several are still growing. What AI has broken is the old equation that revenue grows by adding people. The selloff was partly an overreaction, since a 3 year-old company earning $14 billion does not literally outweigh an industry earning $100 billion. Yet the market read the direction correctly. The labour-arbitrage model that built Indian IT is being replaced, by the firms themselves, with platforms, intellectual property and infrastructure.

The real test is timing. The older, AI-exposed services will shrink while the new AI-native services grow. The question for the coming years is whether the new business scales fast enough to cover the decline of the old one. Indian IT is not dead. It is being rebuilt in public, one earnings call at a time.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox