The past few weeks in the market have been highly complicated. FIIs have sold equities worth $19.82 billion since October 1 last year. In 2008, FIIs sold $15 billion of shares during GFC. But in comparison, the Nifty level has grown three times in size since 2008, and global liquidity has increased. So this selling might not be comparable to 2008.

Why is the FIIs selling?

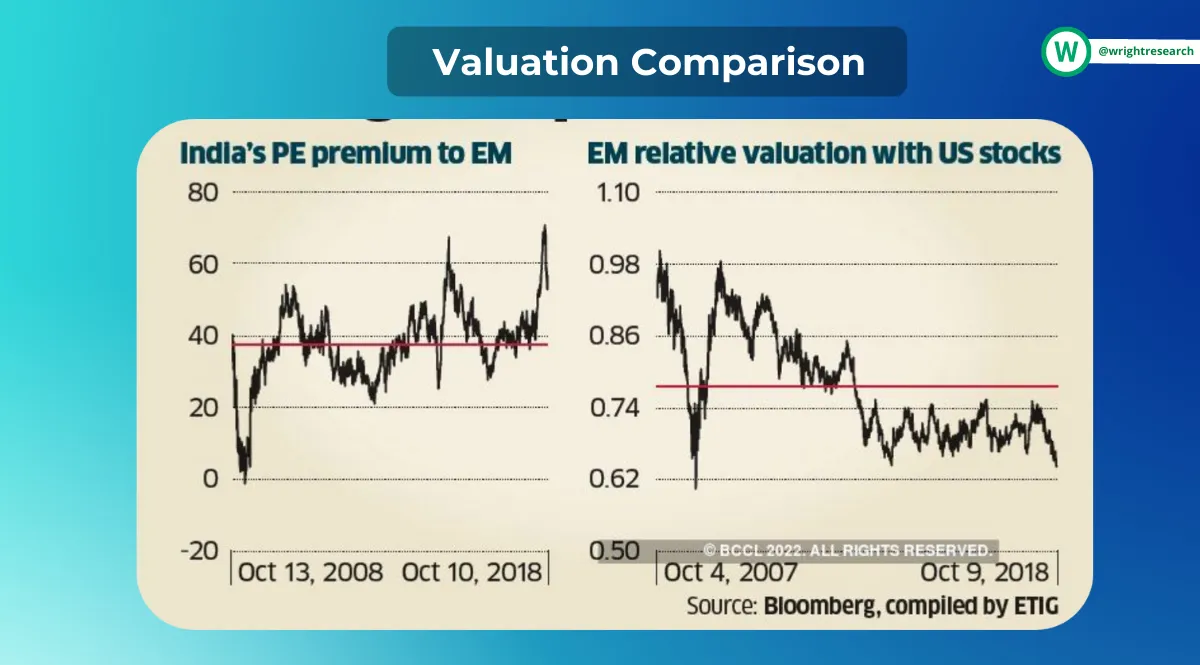

There are various reasons for the FIIs to sell. Interest rate hikes or rising bond yields is undoubtedly one of them but not the only reason. Since October 1 last year, FIIs have sold equities worth $19.2 billion. The first trigger came when India's valuation was regarded high compared to emerging market peers and global funds in October. In addition, the Evergrande crisis had also hit China, and there was conjecture that money would flow from India to China.

The second trigger is, of course, rising interest rates. As bond yield increases in the US, it becomes more attractive for FIIs to invest in US Sovereign Bonds & Domestic Markets. Thus the FIIs start pulling out funds from other markets.

Moreover, in a rising inflationary environment with rising interest rates, overvalued assets suffer, and the idea that India is overvalued has led to people abandoning Indian shares once more. The Rupee would devalue as a result of a high US interest rate.

To put it simply, it becomes more of an opportunity cost for the FIIs to consider & they prefer investing in safe asset classes as they are obligated to provide returns to their investors. Hence, it does make sense for them to sell in such a scenario.

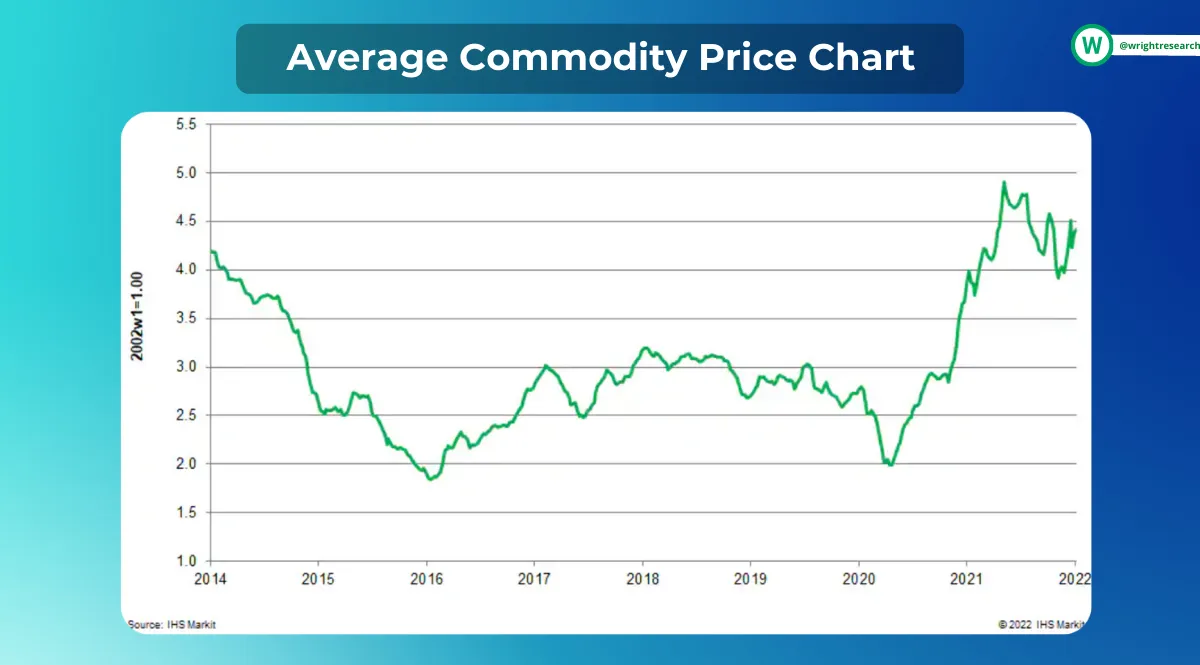

The war in Ukraine was the third and final trigger. The conflict between Russia and Ukraine resulted in severe commodities inflation. As a result, a country like India would be subjected to supply-side pressure, rising inflation, and current account deficit stress. One of the leading causes for the increase in FII outflow was this pressure.

Why are the DIIs buying?

With solid GDP growth rates, rising exports, huge fiscal space, controlled inflation, and a rising Capex cycle, the Indian economy is at its most formidable. Despite the global situation, earnings predictions for different sectors are robust. DIIs realize the potential and pumpkin in money at lows in the Indian market, representing a big consumption-led economy with other sectors appealing to investors. FIIs are expected to regain trust in emerging markets, particularly India, as earnings growth and economic recovery continue in the second half of 2022.

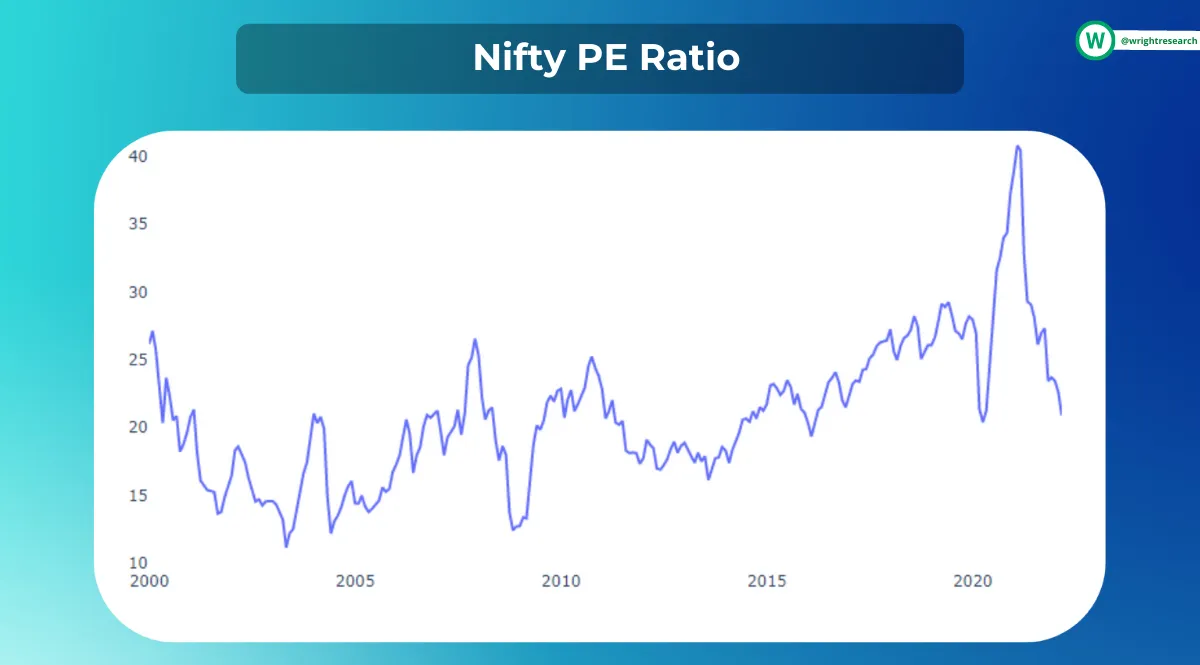

Regarding valuation, the Nifty PE is at a historic low, virtually reaching the bottom levels of March 2020, and a recovery is expected after the geopolitical issue is resolved.

Indian investors also know that the war-related slump is only temporary and that we will recover.

Another factor driving Indian investors to expand their stakes is the growing depth of the domestic market and the growing number of investors who see Indian equities markets as the best place to park their money. In the past few years, retail expansion and penetration to new investors have been unparalleled, and the increased depth is sustaining the markets.

What should you buy?

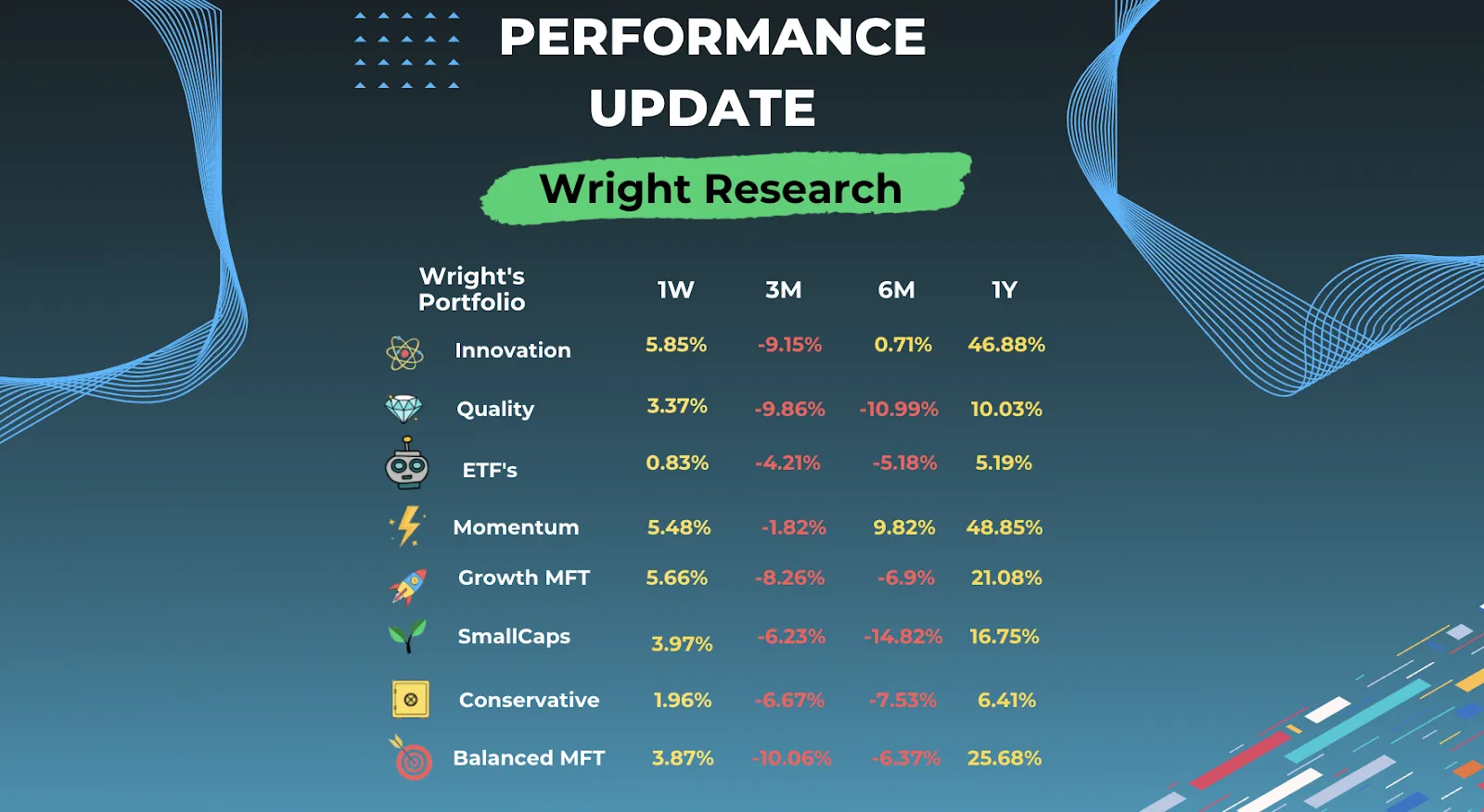

If we were to look at the performance update of all our portfolios, it is evident that the 1W & 1Y returns have been appropriate, irrespective of various market conditions.

We have curated various portfolios based on average risk profiles that provide superior returns even in complicated market conditions. Our innovation portfolio is performing exceptionally well in terms of weekly & yearly returns.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart