The financial year 2022-23 was extremely volatile due to geopolitical tensions, interest rate hikes, and slowing domestic consumption in India. Despite these challenges, India Inc showed strong corporate earnings for the first nine months (April to December). In this blog post, we will look at the best and worst performing sectors in Q4 of 2022-23 and discuss the expectations for India Inc's earnings in the March quarter.

Expectations for India Inc's Earnings in Q4

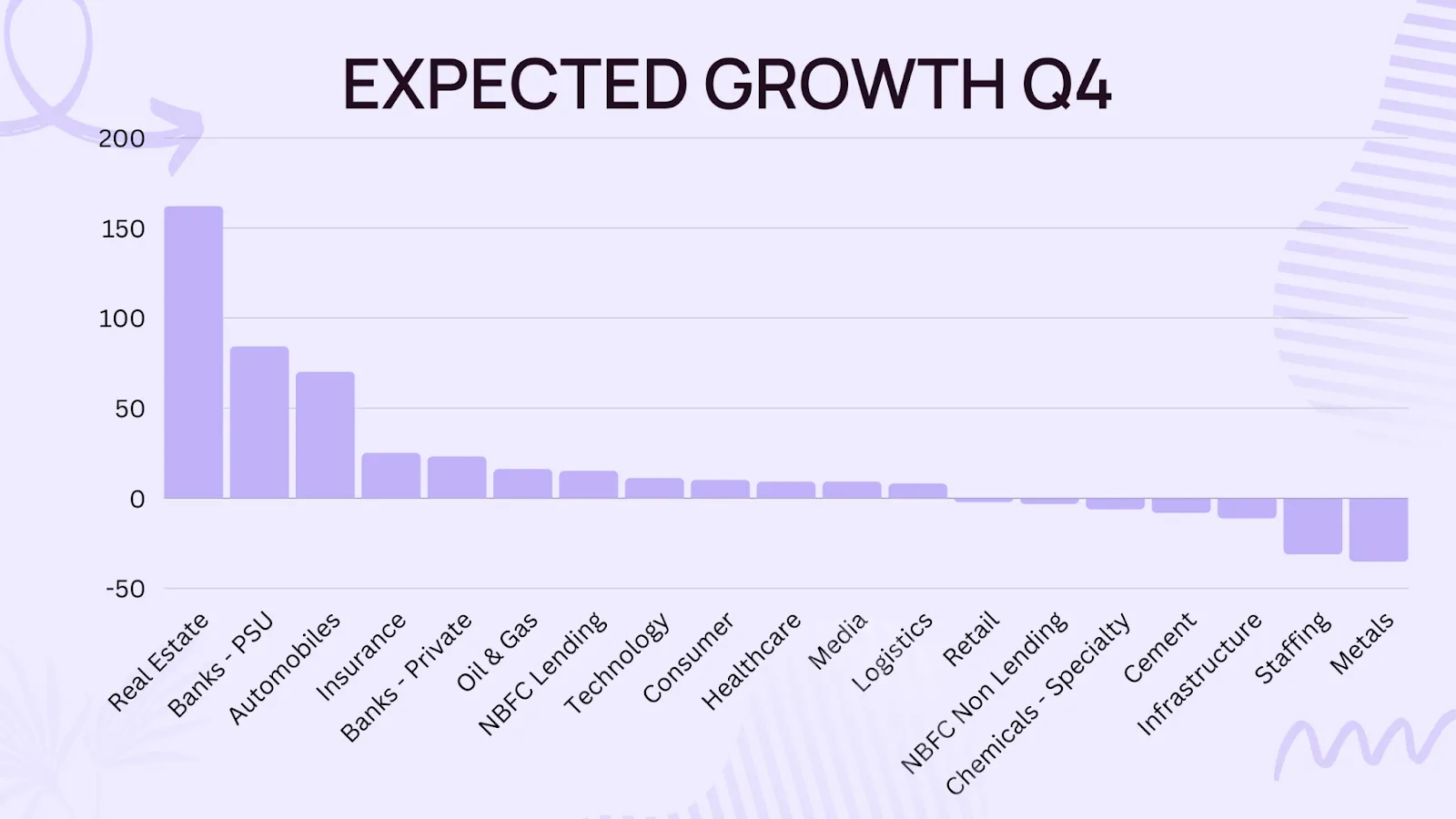

The overall expectations for India Inc's earnings in the March quarter of 2022-23 are largely positive. Significant growth in earnings is expected to come from the BFSI, Automobiles, and Utilities sectors, while FMCG and Healthcare are expected to have moderate earnings. Metals and Technology are expected to lag behind. Although revenues may not show substantial growth due to low aggregate demand, companies are expected to focus on improving margins for better profitability numbers.

BFSI Sector: Leading Earnings Growth in Q4

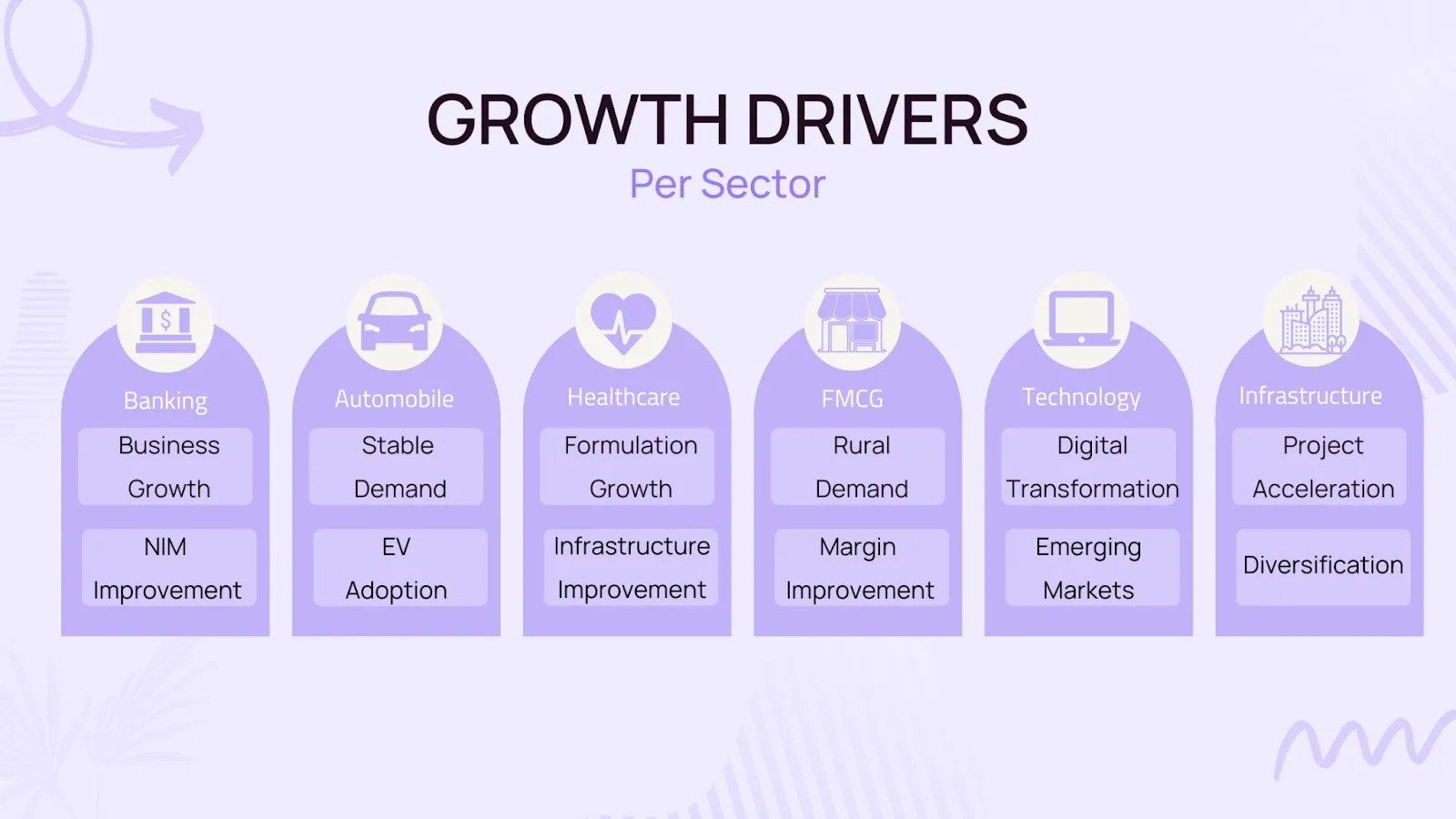

Banking and non-banking lenders are expected to deliver strong growth in both revenue and net profit in Q4, thanks to healthy business growth and improved Net Interest Margin (NIM). Banks have been quick to hike lending rates in line with aggressive rate hikes by the RBI, while insurance companies are expected to see robust premium growth ahead of budgetary changes.

Automobiles Sector: 70% YoY Jump in Earnings

The Automobile sector is expected to report strong earnings numbers, with Tata Motors contributing substantially to the jump in earnings. Stable demand for tractors, domestic two-wheelers, and medium and heavy commercial vehicles have contributed to this growth. However, the sector faces challenges such as export pressures, higher interest rates, and inflationary pressure moderating demand in certain segments.

Healthcare Sector: Moderate Growth

The Healthcare sector is expected to see healthy earnings in Q4, driven by strong traction in domestic formulation and US Generics segments. Sales are expected to rise by 12%, and earnings are expected to rise by 9% in Q4. Hospitals are expected to see higher outpatient volumes compared to previous quarters.

FMCG Sector: Muted Growth

The FMCG sector is likely to see another subdued quarter, with gross margins expected to improve due to declining raw material costs. However, sales are a mixed bag since rural demand continues to lag. Most FMCG companies are expected to post mid single-digit volume growth in Q4, and companies are expected to increase advertising and promotional spending to improve volume growth.

Technology Sector - Moderate Growth

The IT services sector is expected to report moderated growth in Q4 FY23 primarily on account of challenging times from the world’s largest economies. IT automations in North America and Europe may show delayed spend or may face some spend cuts going ahead. Many large enterprises will likely shift their focus on cost optimizations, resulting in higher cost take-out deals, vendor consolidation, and lower discretionary spend. Banking, financial services and insurance, manufacturing, telecom, retail, and high-tech verticals are expected to be impacted by the slowdown, thus weakening the FY24E growth momentum outlook.

Infrastructure Sector: Robust Growth

The Infrastructure sector, particularly road construction companies, is expected to report robust earnings growth in Q4, driven by strong project execution and an increase in project awarding by the National Highway Authority of India (NHAI). The sector is benefiting from accelerated bidding and awarding activities. The order book of companies in the sector has been strengthened, providing revenue visibility for the next two to three years. Additionally, many companies have diversified into non-road projects, further enhancing their revenue profiles. Execution is expected to remain strong as the sector continues to capitalize on the increased pace of awarding and construction.

Oil & Gas Sector: Mixed Results

The Oil & Gas sector's Q4 FY23 earnings are expected to display mixed results, with oil marketing companies experiencing varied outcomes. Despite marketing margins recovering, fluctuations in global oil prices, inventory losses, and changes in refining and petrochemical performances contribute to the sector's mixed performance. Key factors influencing the sector's future prospects include market dynamics, international crude oil prices, and ongoing geopolitical tensions.

Telecom Sector: Absence of Tariff Hikes Impacting Revenues

The Telecom sector is estimated to have moderate revenue for Q4 and flat margins. The absence of tariff hikes and fewer days in Q4 mean that growth in average revenue per user (ARPU) will decline for the quarter. However, 5G technology expansion and coverage will require capital expenditure, driving market share gains for Reliance Jio and Bharti Airtel.

New Age Companies: Consumption Fatigue

New age technology companies are expected to report muted numbers in Q4 due to consumption fatigue in online food and beauty segments. However, B2B e-commerce is expected to maintain its robust growth momentum in Q4.

Challenges for FY24

As we look forward to FY24, several challenges lie ahead. BFSI earnings are expected to normalize due to higher deposit costs and potential NIMs growth restriction. Weak global growth and higher interest rates will have implications for globally-linked sectors such as Commodities and Technology. The onset and progress of monsoons will be crucial for reviving rural consumption.

Conclusion

In conclusion, Q4 earnings for FY 2022-23 are expected to be positive overall, with BFSI, Automobiles, and Utilities driving growth, while FMCG and Healthcare deliver moderate results. Metals and Technology sectors may underperform, and new age tech companies might face consumption fatigue challenges. It is crucial to monitor macroeconomic factors, global conditions, and sector-specific trends as we move into FY 2024 to navigate potential challenges and opportunities in the ever-evolving financial landscape.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox