We can expect muted earnings for Q4 compared to the strong performance for corporate India over the first 9 months of FY24. The first 9 months showed profit growth of around 17% - but expectations for Q4 earnings for the stock market are projected to decelerate to around 10%. The Nifty earnings are projected to grow by 5% year on year in Q4FY24, marking a significant slowdown from the 20% growth that we saw during the first 9 months of FY24. As companies' profit margins shrink, it will become important to look at management guidance and forecasts for corporate revenue growth to meet overall profit expectations. Let’s look at this in depth in today’s article as we discuss the earnings expectation for Indian stock markets for Q4 FY24.

Key Insights For Earnings Expectation For Q4

Demand outlook also remains a critical factor, with domestic-oriented sectors potentially facing vulnerabilities due to weak consumption and slow down in private capital expenditure & government capital expenditure. Moreover, rising oil prices could exert additional pressure on profitability. However, with Indian elections coming up shortly along with interest rate cuts expected on the horizon, the outlook for the Indian market looks strong in the medium to longer term horizon. Why is profit growth slowing down?

There are 2 main reasons why profit growth is slowing down:

Subdued top-line growth: Top-line growth refers to the growth in a company's revenue. Revenue growth is expected to be modest, which means that companies will need to find ways to improve their efficiency in order to maintain profit growth.

Margin pressure: Companies are facing margin pressure, which means that their profit margins are shrinking. This is due to a number of factors, such as rising input costs and increasing competition.

Outlook for Nifty Earnings For Q4

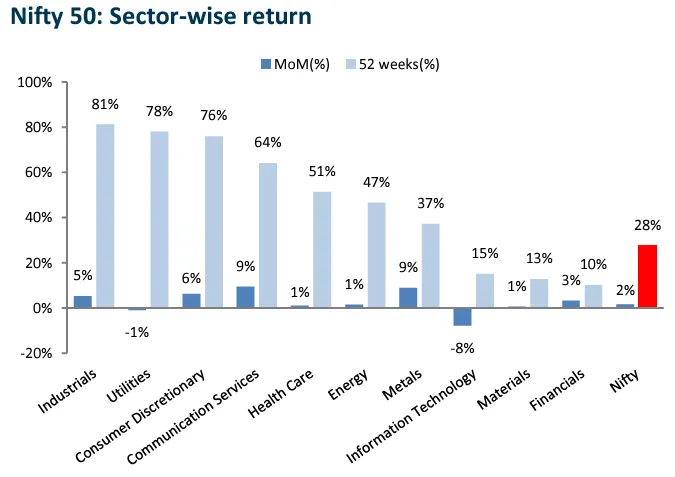

While businesses have seen increasing profit margins, these margins are expected to even out. This means that the rapid growth in profits observed in the first half of the year is likely to slow down, aiming towards a more modest 10% growth for the year, compared to the 15% growth seen in the initial 9 months. Within Nifty, we have seen certain sectors do really well such as Industrials, Utilities, Consumer Discretionary and more.

Overall, sales for Nifty companies in Q4 earnings are expected to increase by around 5-6% on average. However, a few companies are expected to grow their sales by more than 10%. In the past, companies were able to make more profit on each sale they made (margins). This helped profits grow faster than sales. But that's not happening as much anymore, so profit growth is slowing down to match sales growth.

Overall Sector Outlook & Analysis for Q4 FY 24

High Growth Expectations: Autos, consumer services, and private banks are anticipated to witness robust revenue growth exceeding 15% YoY.

Moderate Growth Sectors: Industrial, cement, durable goods, construction, NBFCs, and non-lending financials are expected to post moderate revenue growth ranging from 10–15% YoY.

Sectors Facing Headwinds: IT, FMCG, metals, energy, power, chemicals, and PSU banks are likely to experience weak growth, falling below 10% YoY. Majority of the focus here will be on FY25 management guidance.

Let’s look at each of these sectors in depth.

Agrochemical Sector Outlook for Q4 FY 24

Mixed outlook for the agriculture sector as domestic agrochemical companies see growth, while fertiliser and global agrochemical players face slowdown challenges.

Domestic agrochemical players are expected to report healthy growth despite potential demand impact from reduced reservoir levels in southern regions. Growth supported by stable agricultural commodity prices.

Fertiliser Sector Under Pressure: Anticipated volume growth offset by price falls and reduced subsidies leading to sharp profitability contraction.

Global Agrochemical Companies Facing Headwinds: Continuation of inventory destocking and price pressures on generic products to affect margins. High rebates and discounts necessary for sales, leading to a significant drop in EBITDA margins.

Explore our detailed agriculture sector dashboard .

Automobile Sector Outlook for Q4 FY 24

Strong Q4FY24 performance with positive outlook for the automotive sector , let’s break it down:

Sales momentum continues with a forecasted 14% YoY revenue surge in the auto sector. EBITDA growth expected to outpace revenue at 25% YoY due to scale, net pricing, and favorable currency effects.

Growth Forecast FY24–26: Strong growth across most segments. 2W and tractors are predicted to grow in high single digits, while Passenger Vehicles PV and Commercial Vehicles in low single digits.

Outlook and Valuations: While the short term appears positive, especially for certain high beta stocks, the focus for a volatile upcoming fiscal year should be on stocks expected to deliver sustained earnings.

2W Automobile Sector: Significant volume growth (~25% YoY), with robust demand driving expected revenue increases across key players

PV & CV Auto Sectors: PV Sector expected to show ~11% YoY volume growth, with strong revenue growth anticipated for key players. The CV Sector is expected to show Volume contraction (~5% YoY), yet revenue growth is expected for certain players.

Tractors Automobile Sector: Decline (~18% YoY) due to weak sentiment and a high base, leading to expected revenue contraction for key players.

Explore our in depth automotive sector dashboard .

Banking & Finance (BFSI) Sector Outlook for Q4 FY 24

Strong deposit growth amidst rising loan demands for the banking & finance sector :

The sector has experienced notable deposit growth, spurred by regulatory guidance to balance loan and deposit growth rates. This trend is not limited to major banks but is also evident in non-reporting private banks, which are expected to showcase strong deposit growth and lower Loan-to-Deposit Ratios.

Healthy Loan Growth with NIM Stability as Key: Loan growth has rebounded, with expectations of stable Net Interest Margins for several key players in the sector. The revival in loan growth, despite previous constraints like liquidity tightness and regulatory stances, highlights the sector's resilience.

Seasonal Variations and Competitive Dynamics: The fourth quarter traditionally shows strong growth due to seasonal factors, including the utilization of unused overdraft limits and increased Certificate of Deposit issuances. The competitive dynamics have also shifted, with private banks gaining share at the expense of state-owned entities in the deposit market.

Asset Quality and Performance Expectations: There have not been significant concerns regarding asset quality, and a reversal of provisions is expected for most lenders. Certain banks and Non-Banking Financial Companies are projected to outperform expectations, attributed to their strong growth and robust asset quality.

Deep dive with our banking & finance sector dashboard .

Consumer Staples Sector Outlook for Q4 FY 24

Consumption continues to be a challenge, with subdued YoY growth for the Consumer Goods sector :

Consumer staples sector is expected to see modest growth in revenue, EBITDA, and PAT, with slight acceleration in revenue but deceleration in profit growth compared to the previous quarter. This points to a continuing trend of cautious expansion in the consumer market.

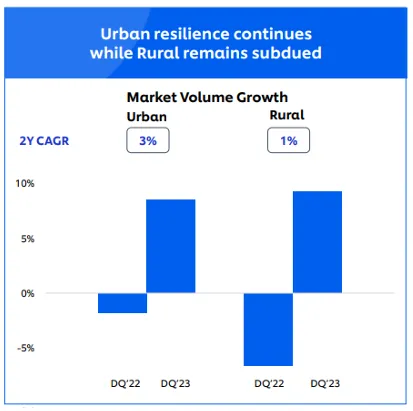

Volume Growth Concerns: Volume growth remains a significant challenge, with low-to-mid-single-digit growth driven mainly by urban demand. Rural demand is particularly sluggish, showing flat to low single-digit growth across various categories.

Gross Margin Expansion: While gross margins are anticipated to expand YoY, the pace of this expansion is relatively small. External factors such as shipping costs and delays, notably due to the Red Sea crisis, could impact margins in certain instances.

Increased Advertising Spend: In response to the slow pace of margin expansion, companies have notably increased their advertising expenditures, aiming to stimulate demand and counteract the adverse effects of heightened competition and subdued volume growth.

Rural Demand: Persistent concerns over rural demand highlight a significant challenge for the sector, with urban demand outstripping rural. However, factors such as expected good monsoons and political spending due to upcoming general elections could potentially revive consumer demand in these areas.

Explore our detailed Consumer Goods sector dashboard .

Infrastructure Sector Outlook for Q4 FY 24

The infrastructure sector is poised for an uptick in execution:

Improved Execution Expected: A robust order book and government initiatives aimed at enhancing cash flows for construction companies.

Revenue and Margin Outlook: Anticipated revenue growth of 16% YoY/QoQ is on the horizon, although EBITDA and PAT margins may see slight declines. The focus on execution efficiency and new order acquisitions remains critical.

Road Sector Slowdown: Road awarding has been slow but showed signs of acceleration in Q4FY24, particularly from the Ministry of Road Transport and Highways.

Railways Sector Boom: The railways sector is witnessing significant activity with the awarding of wagon orders and extensive procurement plans, indicating a robust growth trajectory for rolling stock manufacturers.

Challenges and Opportunities: Despite concerns over competition, commodity price volatility, and high interest rates, the sector is buoyed by healthy order intake in metro rail, buildings, and liquidity-boosting government measures.

Visit our detailed infrastructure sector dashboard .

Insurance Sector Outlook for Q4 FY 24

Let’ explore the outlook for the insurance sector :

Life Insurance Growth: Despite a strong base, life insurers are expected to see aggregate Annual Premium Equivalent growth, albeit with a shift towards linked business affecting margins and Value of New Business.

General Insurance Stability: Growth in the health and motor segments is expected to propel Gross Written Premium growth, with improvements in Combined Operating Ratios enhancing earnings.

Sectoral Optimism: The positive regulatory developments and balanced product mix present a promising outlook for life insurers, with general insurers benefiting from steady market segments and improved underwriting performance.

Explore our detailed insurance sector dashboard .

Industrial and Capital Goods Sector Outlook for Q4 FY 24

Strong Order Inflow and Revenue Growth: The sector has seen significant growth in order inflows and revenues, driven by robust demand across various segments, including power generation, T&D, and railways.

Capex Super-Cycle: A government-led public capex super-cycle, along with emerging private sector investments in new-age industries, is set to drive the sector's growth.

Market Dynamics: While the sector benefits from diverse growth drivers, concerns over premium valuations, global economic slowdown risks, and commodity price volatility persist. Sustainability of margins and the capacity to justify premium valuations through improved execution and order inflows are crucial.

IT Sector Outlook for Q4 FY 24

Modest growth expectations for the IT Hardware & IT Software sectors :

The IT sector is anticipated to report muted growth during the March quarter, largely due to the gradual reversal of furlough effects and reduced discretionary tech spending.

Mixed Largecap Performance: Largecap IT companies are expected to show varied results, with some leading in growth due to specific advantages, while others may face challenges due to cuts in discretionary spending and project ramp-downs.

Midcap Outperformance: Continuing the trend from recent quarters, midcap IT companies are predicted to outperform their largecap counterparts, showcasing stronger sequential revenue growth.

Deal Wins and Margins: Despite the volatile demand environment, deal flows are expected to remain robust for certain players, contributing to moderate margin expansion. However, there could be margin declines in some companies.

Attrition and Supply-Side Dynamics: The improvement in supply-side dynamics, with attrition rates bottoming out, is likely to aid margin expansion for several companies.

Financial Year 2025 Outlook: Management guidance for FY25 will be closely related to FY25, looking for signs of improvement in growth trajectories following a challenging year. With cautious spending by clients, especially highlighted by Accenture's commentary, IT companies are expected to offer conservative guidance for FY25.

Explore our detailed IT Hardware & IT Software sectors dashboards.

Metals and Mining Sector Outlook for Q4 FY 24

Let’ explore the outlook for the mining & metals sector :

Non-Ferrous vs. Ferrous Performance: Non-ferrous metals are anticipated to outperform ferrous metals in the upcoming quarter. This is due to challenges in the ferrous sector, including lower steel prices and higher coking coal costs, which are expected to impact EBITDA negatively. Conversely, non-ferrous EBITDA is expected to see slight improvements due to stable or decreasing costs of production (CoP) and a marginal increase in LME aluminium prices.

Recovery in Steel Prices: Looking ahead to Q1FY25, there's optimism that steel companies’ EBITDA per tonne will improve, driven by a decrease in coking coal prices. This could help offset the adverse effects of lower steel prices.

Mining Sector Gains: Specific segments within the mining sector, particularly those involved in iron ore and coal, are expected to benefit from increased prices and higher volumes, alongside lower employee costs.

Explore our detailed metals sector dashboard .

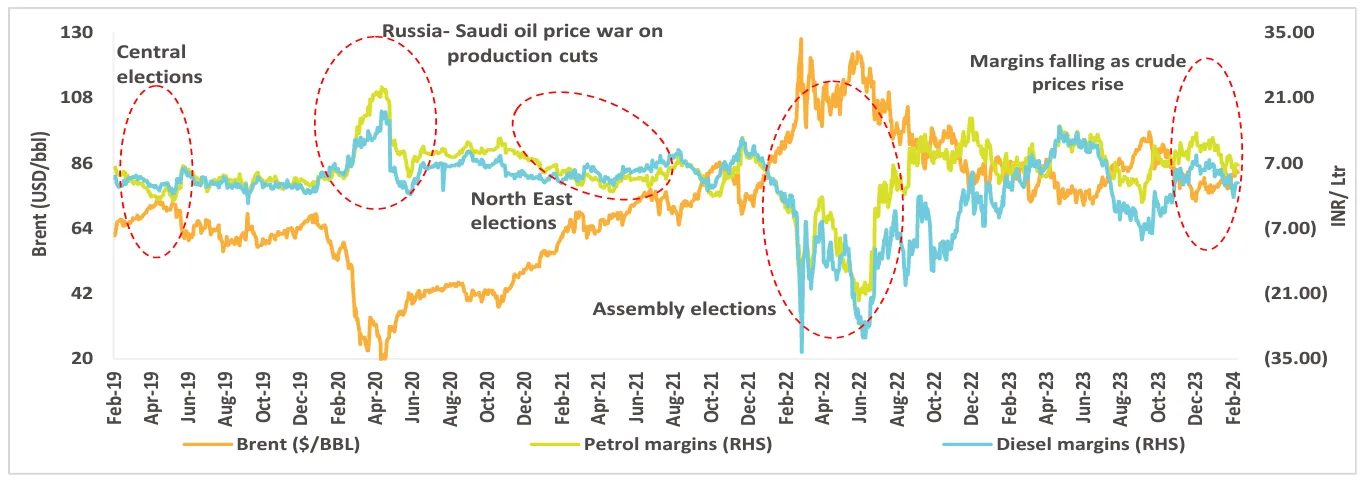

Oil and Gas (O&G) Sector Outlook for Q4 FY 24

Moderate Aggregate EBITDA Growth: The O&G sector is expected to witness a modest 3% year-on-year growth in EBITDA, supported by strong performances across various sub-verticals, albeit offset by underperforming Oil Marketing Companies.

Refining Margins and Retail Fuel Margins: There's a notable decline in refining margins due to weaker global product cracks. However, retail margins for diesel and petrol have seen significant improvements, expected to bolster the performance of OMCs.

Gas Transmission and Distribution: Expected to experience solid volume growth, driven by price reductions and a significant decrease in spot LNG prices. Despite a slight reduction in EBITDA margins, they remain high, indicating a robust demand for natural gas and related services.

Pharmaceutical & Healthcare Sector Outlook for Q4 FY 24

Pharmaceutical sector expected to see revenue and EBITDA growth with Diagnostic companies in the healthcare sector expected to do well.

Anticipated 14% YoY revenue growth and 29% YoY EBITDA growth, with sequential increases of 4% and 8% respectively.

US Market: Expected benign price erosion to favor generic players, particularly ARBP. Lower active pharmaceutical ingredient (API) prices are predicted to enhance gross margins, despite potential challenges from high inventory levels and Red Sea logistical disruptions.

Indian Market: Domestic business projected to grow at 11% YoY. Companies like Torrent Pharma (TRP) and SUNP are likely to perform well due to their focus on chronic therapies and medical representative additions. Alkem might face challenges due to flat anti-infective growth.

Diagnostics Performance: Q4 traditionally offers better performance for healthcare, with diagnostic companies expected to shine particularly bright. Diagnostics to experience a seasonal uplift, with companies like Vijaya and Metropolis set to outperform due to strategic acquisitions and recent price hikes, respectively.

Explore our detailed Pharmaceutical sector & healthcare sector dashboards.

Real Estate Sector Outlook for Q4 FY 24

Let’ explore the outlook for the real estate sector :

Surge in Residential Sales: Anticipated 14% YoY increase in residential sales in Q4FY24, marking the highest-ever quarterly demand despite rising housing prices. This surge is contrasted with a modest 1% YoY increase in new launches, indicating a strong demand-supply dynamic.

Office Space Leasing Gains: Gross office space leasing expected to have jumped 33% YoY to 20 million square feet in the same period.

Retail and Hospitality Resurgence: Both segments are likely to have experienced strong performance in Q4FY24, with hotel occupancies returning to pre-COVID levels and both Average Daily Rates and Revenue Per Available Room seeing significant upticks from pre-pandemic figures.

Price Trends and Inventory Liquidation: Residential property prices expected to have increased by 10-12% YoY, with companies benefiting from inventory liquidation and an uptick in launches to leverage festive demand.

Commercial Segment's Comeback: After facing challenges due to weak economic conditions in developed markets, the commercial segment is poised for a recovery, with improved absorption rates forecasted.

Explore our detailed real estate sector dashboard .

Specialty Chemicals Sector Outlook for Q4 FY 24

Let’ explore the outlook for the agriculture sector : Explore our detailed agriculture sector dashboard .

Sequential Growth Anticipation: An expected 8% QoQ revenue growth and 10% EBITDA growth across the specialty chemical sector, indicating recovery from a bottomed-out Q3FY24. Companies serving diversified end-user industries are likely to see better growth compared to those focused on agrochemicals, which are still grappling with high channel inventories.

Sectoral Recovery Signs: Improved demand in sectors like fluoropolymers and consumption-led industries, despite challenges in agrochemicals due to ongoing inventory and price pressures.

Agrochemical Inventory Challenges: Persistent demand pressure for specialty chemical players in the agrochemical sector, with specific companies facing continued margin pressure despite a slight improvement in pricing environments.

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox