China’s stock market, which experienced substantial declines, is now showing signs of recovery. Analysts believe the market may have reached its lowest point, with the recent government initiatives providing a much-needed boost. The property sector, a critical component of the Chinese economy, has seen several historic stimulus measures aimed at revitalizing the market.

The International Monetary Fund has revised its projection for China's economic growth in 2024 to 5%, up from the earlier forecast of 4.6%. The 5% growth projection aligns with the target set by the Chinese government for the world's second-largest economy, which is currently facing a slowdown triggered by a property sector crisis and industrial overcapacity. It has grown by 5.3% in the first quarter of 2024. Over the medium term, the IMF projects growth to decelerate to 3.3% by 2029 due to demographic shifts (ageing population) and slower productivity growth.

The recent challenges in the property market have highlighted the need for diversification among mainland investors. Traditionally, Chinese investors have heavily favored real estate, but the recent turmoil has underscored the risks of such concentrated investments. As a result, there is a growing inclination to diversify into stocks, which may lead to increased activity and stability in the equity markets. Let’s look China’s economy & stock market in depth and how it impacts us as investors in Indian stock markets.

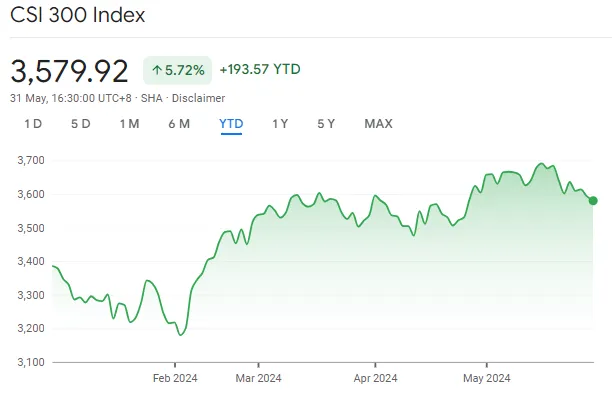

China’s Stock Market Rallies

Recent developments suggest a more positive outlook for Chinese stocks. The CSI300 equity benchmark reached an eight-month high and is up 5.72% so far this year. This improvement is attributed to government efforts to enhance market liquidity and curb malpractices. Despite these gains, the market remains one of the cheapest in the Asia Pacific region, indicating potential for further growth.

The CSI300 has faced challenges, being the third worst-performing stock market in Asia last year with an 11.38% loss, and recording consecutive losses in 2021 and 2022. Similarly, Hong Kong’s Hang Seng index saw a 14% decline in 2023, marking its fourth straight year of downturns.

The recent rally in Chinese stocks, although expected to pause in the short term, is backed by confidence in improved earnings in 2024. Earnings growth is a critical driver of share performance, and investors are likely to respond positively to signs of financial recovery.

The historical underperformance of China’s stock markets, combined with recent reforms and support measures, suggests a potential turning point. China's authorities have introduced measures aimed at increasing market liquidity and improving regulatory oversight. These include tighter rules for listing and delisting companies, and warnings to firms with inadequate dividend policies. Such reforms aim to create a more transparent and reliable market environment, potentially attracting more investors. These developments indicate that the market may have reached its lowest point and is now positioned for recovery. The shift from an overly pessimistic view to cautious optimism is supported by tangible government actions and regulatory improvements.

China’s Property Sector - Bankruptcy or Recovery?

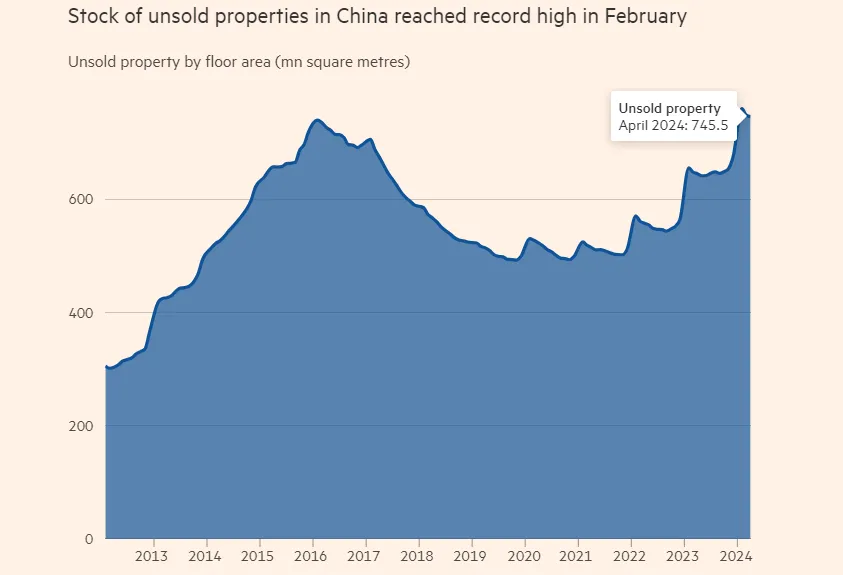

Chinese real estate market has been under severe strain, with a massive inventory of unsold housing weighing down the economy. According to estimates by Goldman Sachs, China has approximately 30 trillion yuan worth of unsold housing inventory, including land and completed apartments. This figure is about 10 times the amount of housing sold last year, indicating a profound oversupply issue.

China's property sector, a significant component of its economy, remains a major challenge, causing widespread crisis. The People's Bank of China has established a 300-billion-Yuan (approximately $42.25 billion) re-lending facility for government subsidized housing projects to buy back unsold homes and idle lands to stabilize the real estate sector. While this is substantial, it is insufficient to address the root of the oversupply problem. Goldman Sachs has highlighted the magnitude of the challenge, estimating that, in addition to the officially unsold housing stock, there are 90 million to 100 million units of "shadow supply." These units, often purchased as investment properties, remain unoccupied and contribute to the market’s oversupply issues.

In response to the persistent slowdown and falling house prices, Beijing has primarily focused on completing unfinished residential projects, which are typically sold in advance. The new measures announced include scrapping minimum mortgage rates and lowering down payments for first-time homebuyers. These steps aim to revive a market that has been a cornerstone of China’s economic growth and household wealth for decades.

China Tightens Capacity Controls For Key Metals

Industrial Profits Improve

Profits at China’s industrial companies rebounded in April, up 4% year-on-year after a 3.5% decline in March. YTD profits increased to 4.3% reflecting Beijing's targeted efforts to improve the manufacturing sector amid broader economic challenges. The uptick underscores the impact of government measures aimed at promoting "high-quality development" in manufacturing, which have spurred increased output and exports. Chinese exports grew by 1.5% year-on-year in dollar terms. Industrial production also saw a substantial 6.7% increase in April, indicating that the government’s push to enhance manufacturing capabilities is yielding positive results.

Developed economies have raised concerns over perceived overcapacity, leading the EU to investigate state support for Chinese EV production. In response to similar concerns, the U.S. has imposed 100% tariffs on EV imports from China, where fierce domestic competition has triggered a price war.

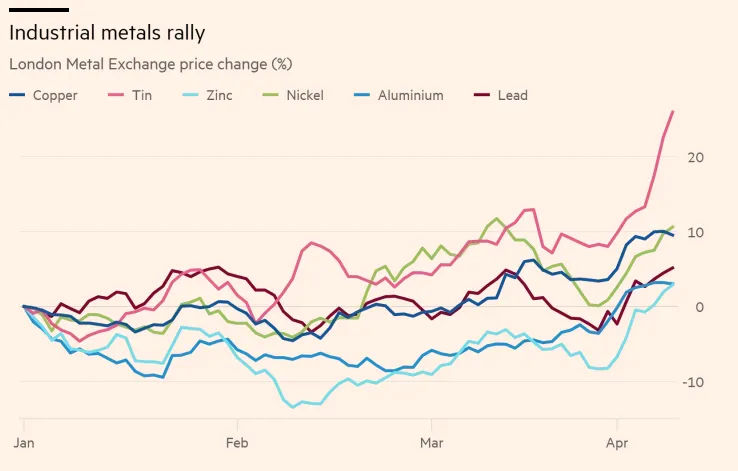

Are Metals Rallying?

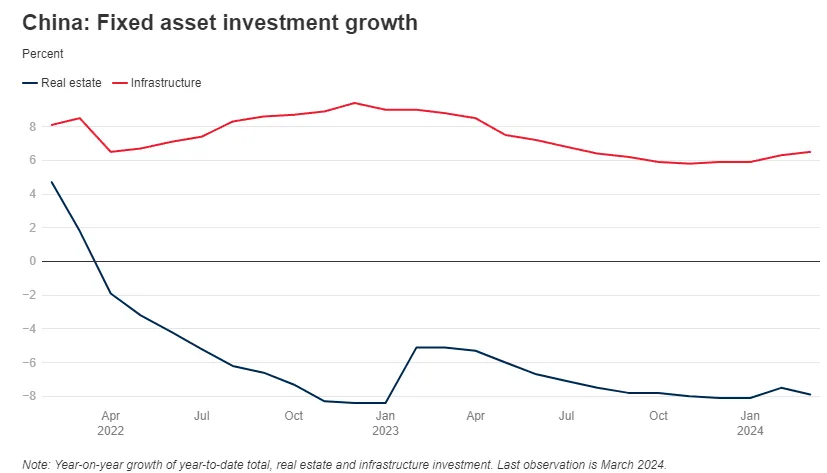

Subdued demand is likely to exert downward pressure on metal prices, particularly due to the ongoing weakness in China’s real estate sector. Despite this downturn, China’s robust industrial and infrastructure investments are anticipated to mitigate some of the demand decline for certain metals. Investments in these sectors are likely to bolster demand for metals such as copper, which is essential for various industrial applications and infrastructure projects. This internal investment strategy could provide a buffer against the broader declines in metal demand caused by the real estate slowdown.

Aluminium prices have surged to a two-year high as China, the world’s largest producer, tightens capacity controls across various metals to meet its emission-cutting goals. China has strengthened capacity limits in industries such as steel and alumina as part of a work plan for energy conservation and carbon reduction for 2024-2025. This decision comes at a critical time when the global transition to greener energy, increased demand from the use of Artificial Intelligence models is boosting demand for metals like silver, copper and aluminium. By controlling new capacity for copper smelters and alumina output, and carefully allocating capacity for silicon, lithium, and magnesium, China aims to balance supply and demand more effectively.

Emission-Cutting Goals Drive Aluminium Prices to Two-Year High

Aluminium is essential in products ranging from window frames to solar panels. Its price has climbed alongside other base metals this year. The increase is fueled by anticipated US monetary easing and China’s efforts to support its struggling property sector, with aluminium prices rising nearly 20% this quarter alone.

One significant policy reiterated by the government is the "aluminium swap scheme," which mandates that any new smelter capacity must be matched by the closure of an existing one. This ensures that new capacity for aluminium, alumina, polysilicon, and lithium batteries meets advanced energy efficiency standards. As a result, aluminium prices rose as much as 1.1% to $2,799 a ton on the London Metal Exchange, the highest since June 2022, before settling at $2,777 in Shanghai.

Analysts highlight aluminium's strong demand in China, driven by sectors such as ultra-high voltage power transmission, making it an attractive target for funds moving away from copper. Meanwhile, the steel industry will continue to face output controls to keep production levels below those of previous years, further impacting demand for iron ore. Consequently, iron ore futures fell 1.9% to $116.70 a ton in Singapore. These developments underscore China's strategic efforts to manage its metal production capacity while transitioning to a greener economy.

Silver Price Rises: Increased Investment in Solar & Renewable Energy

Global investment in solar PV manufacturing more than doubled last year to approximately $80 billion, accounting for around 40% of global investment in clean-technology manufacturing, according to the International Energy Agency (IEA). Notably, China more than doubled its investment in solar PV manufacturing between 2022 and 2023, consolidating its position as a leader in this sector.

Last year, global renewable capacity increased by 50% to nearly 510 gigawatts, marking the fastest growth rate in three decades. Solar PV energy contributed three-quarters of this growth. The demand for silver from solar PV panel manufacturers, especially those in China, is projected to increase by almost 170% by 2030, reaching approximately 273 million ounces, or about one-fifth of total silver demand, based on current trend projections.

China's aggressive expansion in the solar PV sector has significantly impacted the global market. The country's massive installation efforts and manufacturing capacity have led to a substantial supply glut, driving down spot prices for solar PV panels by nearly 50% last year. China's market dominance is expected to continue, with projections of maintaining an 80% to 95% market share of global supply chains and doubling manufacturing capacity again by the end of 2024.

Mining companies are positioning themselves to capitalize on the rising demand for silver. The recent surge in silver prices, which hit $28.84 an ounce last month—the highest in over a decade—reflects these market conditions. Currently, silver prices are around $27.50 an ounce. If silver prices continue to rise, manufacturers of solar PV panels may need to increase their prices, although this is not expected to dampen demand significantly due to the current low price levels.

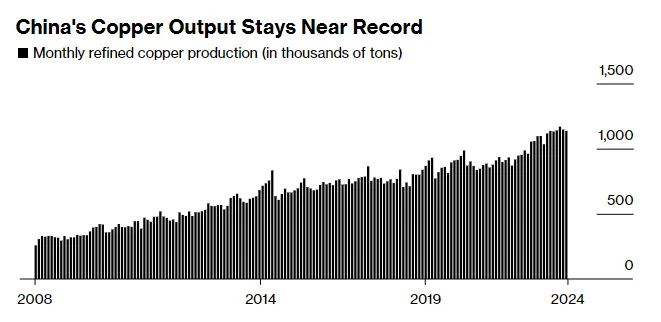

China's Copper Market: Defying Global Shortages with Near-Record Production

While the global copper market is experiencing significant shortages, leading to record-high prices and a $49 billion takeover battle, China, the world's largest producer and consumer of refined copper, is bucking the trend with near-record production levels.

China's copper smelters are maintaining high production rates despite a global scarcity of raw materials. This continued output is primarily driven by the availability of scrap metal, which has become more accessible as higher copper prices incentivize recycling. Scrap metal, derived from discarded items like pots, pipes, and wires, is being processed into blister copper, a semi-processed form of the metal. This blister copper is then used as a substitute for the increasingly scarce imported ore.

The surge in scrap copper’s supply has created a significant price differential between scrap and refined copper. Recently, this discount widened to 4,615 yuan ($637) per ton, the largest in at least 8 years. Despite the global copper shortage and the resultant price surge to over $11,000 per ton, China's abundant supply has created a price retreat to just above $10,300 per ton. This 21% increase for the year reflects the complex interplay between China's supply dynamics and global market trends. As long as China remains oversupplied, copper prices are likely to struggle to make further gains.

Indian Economy Will Grow Under China Plus One Strategy & PLI

China +1 strategy involves MNCs diversifying supply chains away from China and this is expected to drive substantial increase in exports and investment for these countries. As such India and Vietnam are emerging as significant beneficiaries of the China plus one strategy, unlocking new growth opportunities. India's exports are projected to surge from $431 billion in 2023 to $835 billion by 2030. This growth is attributed to its large domestic market, which attracts firms looking for supply chain alternatives to China. Sectors such as electronics, apparel, toys, automobiles, capital goods, and semiconductor manufacturing are seeing increased investment.

The electronics sector is expected to be the fastest-growing, with exports clocking a compound annual growth rate of 24%, nearly tripling to $83 billion by 2030. Machinery exports are also set to more than double, reaching $61 billion by 2030 from $28 billion in 2023. India's potential in global value chain integration is underrepresented by current low production linked incentive (PLI) disbursements. India's large market, rapid growth, lower labor costs, and political and economic stability make it an attractive destination for investment in consumer goods production for both domestic and export markets.

India's share of global trade will rise to 2.8% by 2030, driven by its competitive production capabilities. This competitiveness is likely to accelerate exports, improve the country's trade balance, and positively impact its current account.

Nomura surveyed 130 enterprises indicating growing interest in India and Vietnam, particularly from US-based companies in the electronics sector. Japanese and Korean companies are also investing in India's auto, consumer durable, and electronics sectors to capitalize on the growing domestic demand and leverage India as a manufacturing base. This influx of investment is expected to strengthen India's manufacturing sector and boost its export share, supporting sustained corporate earnings growth of 12-17% over the medium term.

Conclusion

Despite the positive trends in manufacturing and exports, China’s economy continues to face significant hurdles. The property sector remains in a historic slowdown, and domestic consumption is weak, posing risks to sustained economic recovery. Domestic demand is still "insufficient" and emphasizes the need to accelerate the development of new productive forces—a term referring to China’s focus on advancing its manufacturing capabilities. This suggests that while external demand and government policies have provided a boost, sustainable long-term growth will require stronger internal consumption and innovation. Outside of China, metal demand is expected to remain subdued due to the impact of elevated interest rates on economic activity. Higher interest rates generally suppress economic growth by increasing borrowing costs, which in turn can reduce investments and industrial output. As interest rates drop, overall demand is expected to improve which will also contribute to stronger demand for metals.

For Indian investors, while China's stock market is recovering due to government initiatives and improved liquidity, its property sector's persistent challenges highlight the importance of diversification. This lesson is crucial for Indian investors as India benefits from China +1 strategy & PLI, which is driving significant export growth and attracting foreign investment. With exports projected to nearly double by 2030 and substantial investments in key sectors, India's competitive production capabilities and large domestic market position it as a key player in global supply chains. As exit polls & elections results come out, do you think Indian stock markets are well positioned for growth?

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox