The Indian Information Technology (IT) sector is poised at a challenging crossroads as we enter the earnings season for the first quarter of the fiscal year 2024. Analysts tracking the sector have observed that the weakening demand, instigated by recession fears in the United States and recent wage hikes, is likely to exert pressure on Q1 earnings.

The banking and financial services sector, contributing nearly 30% to IT companies' earnings, is yet to see a rebound in orders. Adding to the prevalent scenario, declining consumer spending and weak demand from the North American region make the situation tougher for tech companies.

In this blog post, we will provide an in-depth analysis of the IT sector's earnings season for Q1 FY24, focusing on three industry giants - Tata Consultancy Services (TCS), HCL Technologies, and Wipro. We'll discuss their performance, management's outlook, and the future implications for the sector.

IT Sector Overview

The Indian IT sector, once heralded as a leading contributor to corporate profits and growth, has been navigating through some significant headwinds. Last fiscal year, its slice of the overall corporate profits pie shrunk to a 21-quarter low of 9.7% in Q4 FY23, down from a 34% share in Q4 FY20. This development can be attributed to a myriad of factors, including a global slowdown, macroeconomic uncertainties, and a banking crisis in US and European banks.

The Q4 FY23 earnings data indicated a significant slowdown in the IT sector. The quarterly profit contracted by 10.5% YoY, marking the first yearly decline in eight quarters. Sequentially, there was a drop of nearly 7% in the March quarter. Topline growth also slowed down to 12% from a massive 26.5% in Q4 FY22. This slowdown is reflected in the rising employee costs that continue to eat into the revenues, putting additional pressure on margins.

In a seasonally strong period for the IT sector, predictions for the June quarter earnings don't inspire much optimism either. Discretionary spending slowdown, reduced client budgets, higher costs, transition costs, and pricing pressures are expected to make a significant dent in the IT sector's earnings. Major players are anticipated to revise their sales growth outlook downward for FY24.

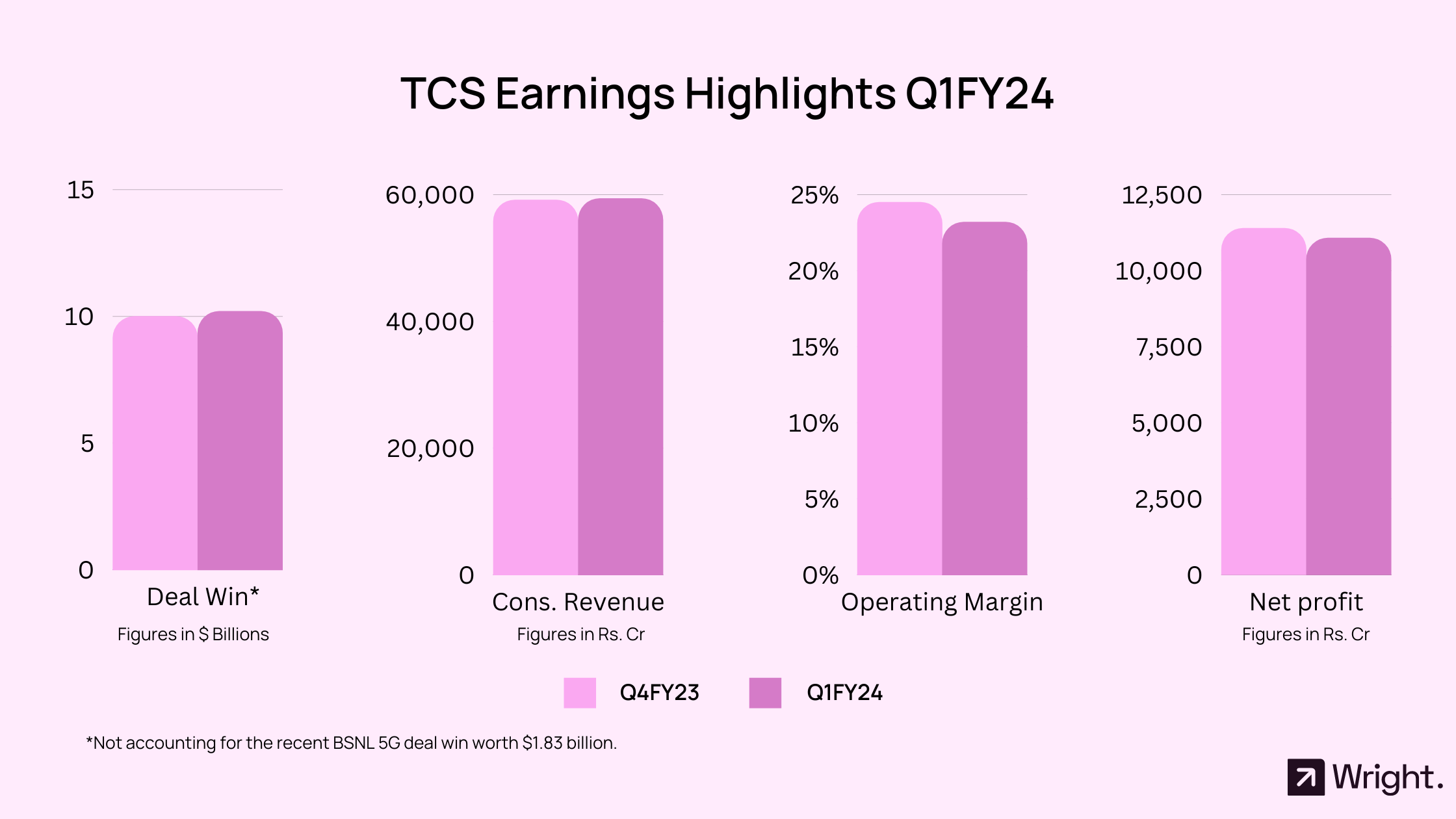

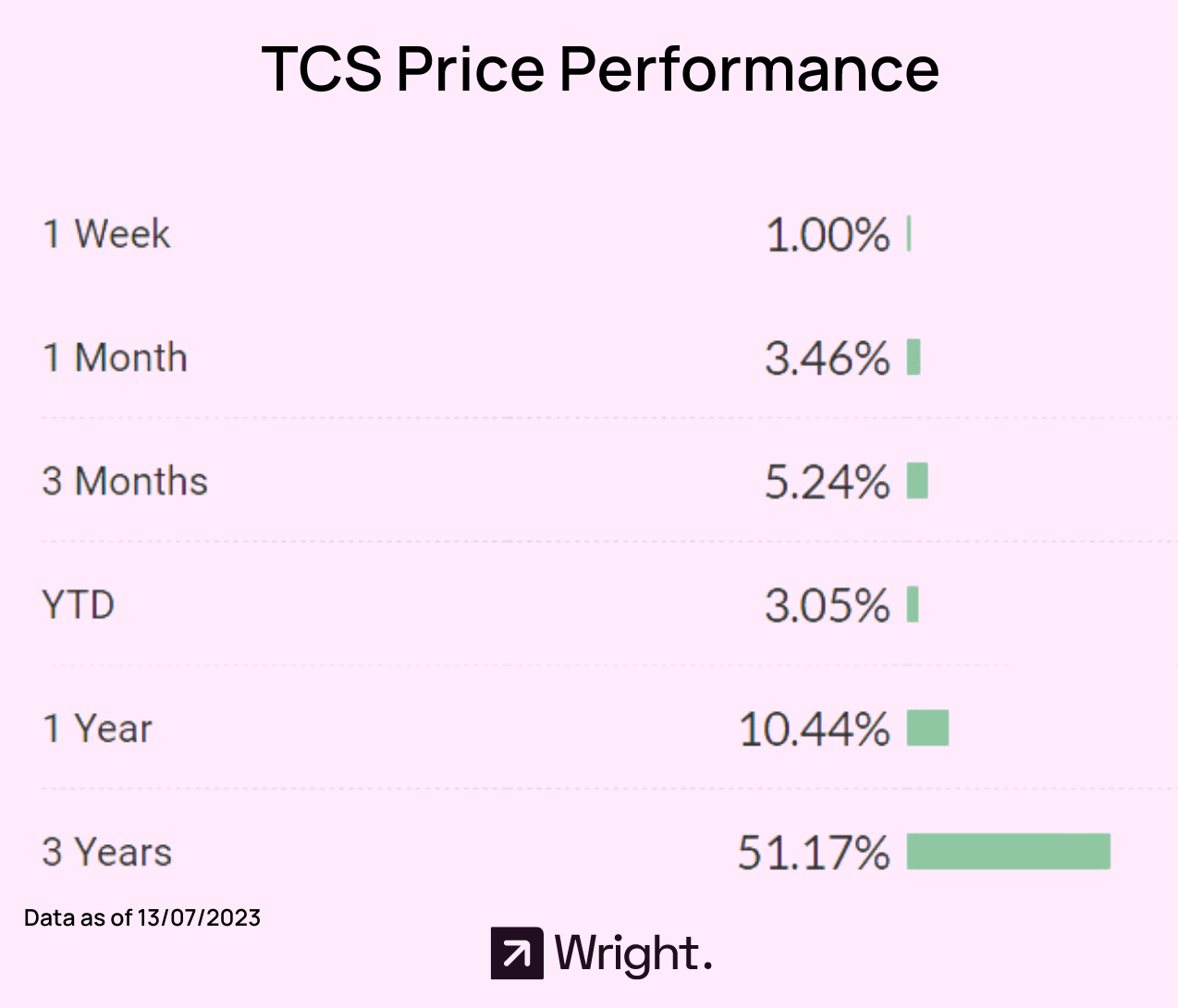

TCS Earnings Q1 FY24: Resilience Amid Global Challenges

Despite the globally challenging quarter, TCS started the earnings season on a promising note. The largest software services exporter in India reported a 16.8% growth in net profit and a 12.5% rise in revenue from operations, surpassing already muted analyst expectations for the first quarter. These numbers not only meet expectations but slightly exceed them, demonstrating the firm's resilience during a globally challenging quarter. Despite a slight quarter-on-quarter decrease in profits, the growth trajectory of TCS remains promising.

Even though the company's operating profit fell by 5% and its operating margin slid from 24.5% in Q4FY23 to 23.2% in Q1FY24. This 130 basis point drop in margin does indicate some pressure on profitability, likely due to salary hikes, various macroeconomic headwinds and ongoing global challenges. Based on the CFO’s commentary, the salary hikes resulted in a 200bps impact on the operating margin.

The total contract value (TCV) stands at a robust $10.2 billion, not accounting for the recent BSNL 5G deal win worth $1.83 billion. This robust TCV bodes well for TCS, suggesting healthy business demand and future revenue streams. Additionally, new deals in the UK Life and Pensions space (UK NEST deal worth $1 billion) reiterates TCS's competitive edge in this market. In terms of industry segments, it’s a mixed bag with growth in the BFSI sector being modest, and limited contributions coming from other areas, except perhaps the life sciences segment. and.

The comments from TCS's top management signal an optimistic outlook and strategic focus on emergent technologies, particularly in the realm of generative AI. Confidence in longer-term demand for their services and commitment to invest early in new technologies attests to TCS's forward-looking strategy. Management commentary reflects TCS's commitment to innovation, strategic investment in emerging technologies, and its aim to sustain its leadership position in the market.

Overall, despite a tough global economic environment, TCS has posted a robust performance in Q1FY24. The results underscore TCS's solid market position and its ability to navigate challenging market conditions. However, the drop in margin reflects pressure on profitability, hinting at the need for margin improvement strategies going forward.

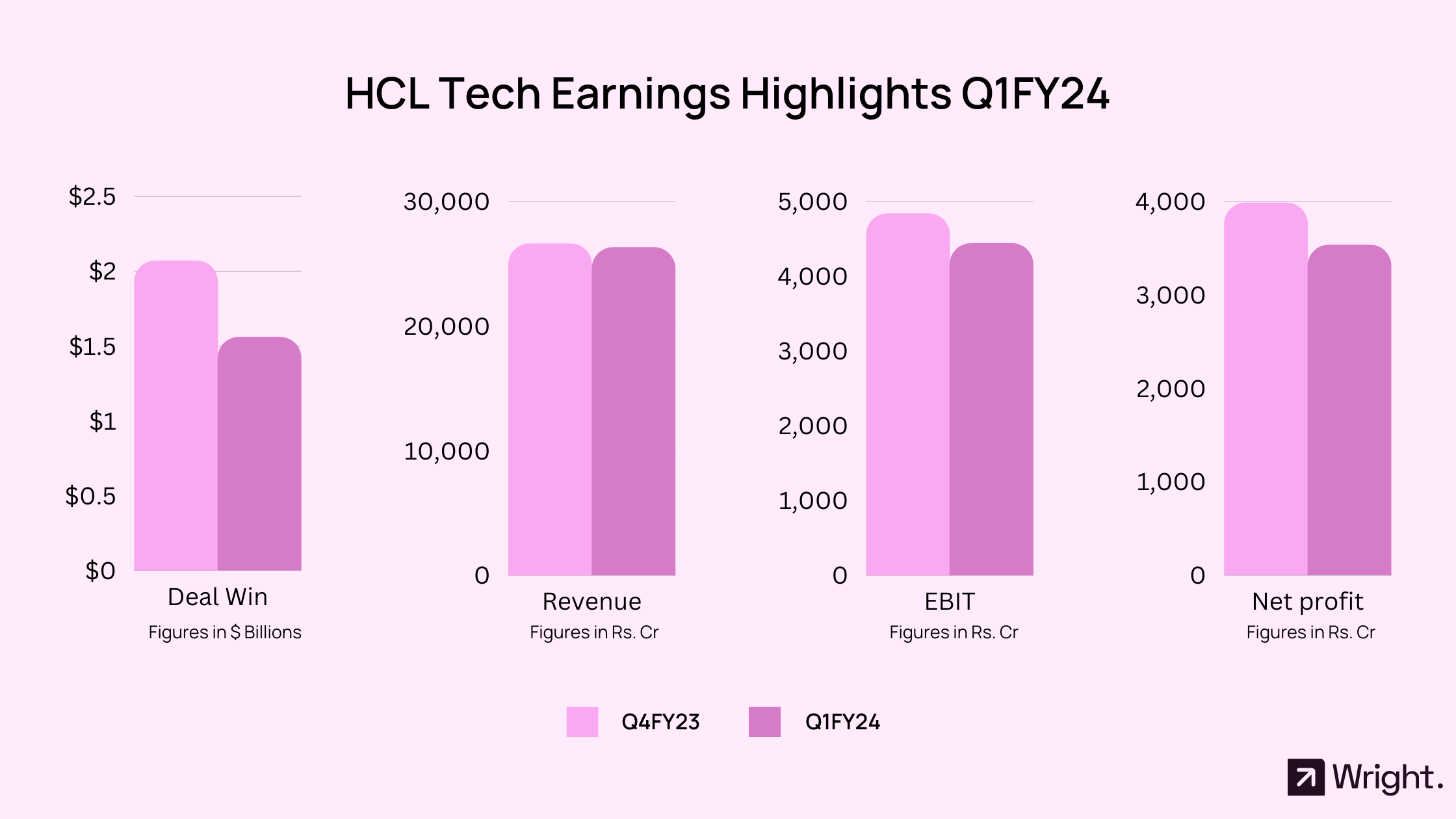

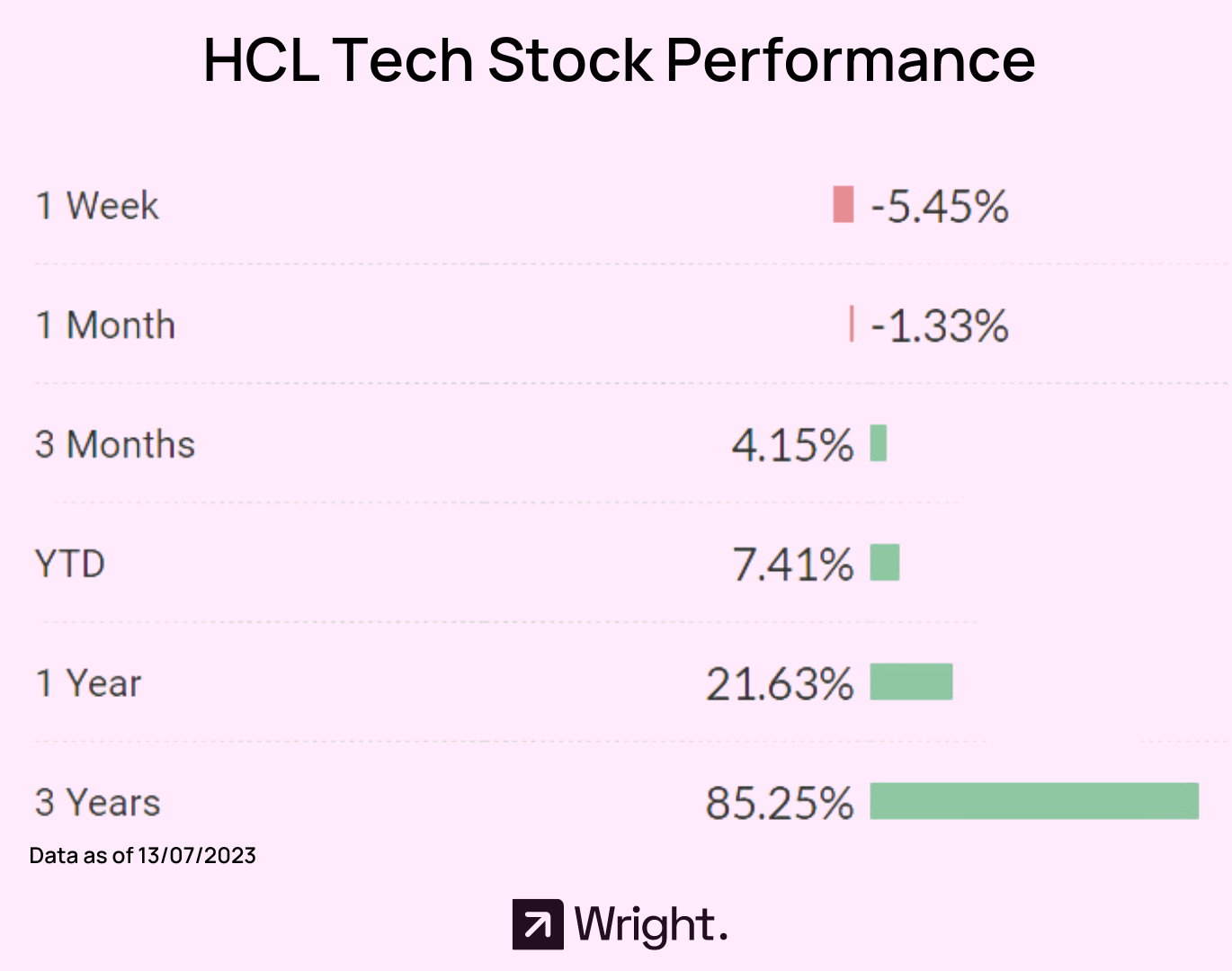

HCL Earnings Q1 FY24: A Mixed Bag

HCL Technologies' Q1 FY24 performance shows a mix of robust YoY growth and sequential downturns. The company reported a promising 7.6% YoY growth in net profit, but saw an 11.2% sequential drop. While its consolidated revenue showed a healthy YoY increase of 12%, the quarterly results indicate a minor sequential decline of 1.2%. This can largely be attributed to deal ramp-downs in sectors like Hi-tech and telecom.

A key area of concern was HCL's operating margins, slipping from 18.25% in the previous quarter to 16.9% in Q1 FY24, indicating a compression in profitability. On top of this slippage, HCL has also deferred annual salary review and compensation revisions by a quarter which would put further pressure on the operating margins. This slippage in operating margins along with a lower than expected net profit, could be a cause for concern.

In terms of verticals, there's a clear slowdown with engineering and R&D services witnessing a 5.3% decline in revenue QoQ, however, IT and Business Services have shown a marginal uptick. Deal wins also experienced a dip compared to the previous quarter, adding to the lukewarm results.

However, CEO's commentary sheds light on the company's coping mechanisms in the face of a challenging demand environment. His assurance of other verticals picking up, buoyed by large deals that have helped counterbalance cuts in discretionary spending, paints a somewhat optimistic picture for the near future. Furthermore, the retention of its guidance of 6-8% constant currency revenue growth for FY24, and an operating margin at 18-19%, signals a certain level of confidence in its business strategies for the fiscal year.

While there's no denying that HCL Tech's Q1 FY24 performance shows some signs of struggle, with profit and revenue taking a hit, the management's outlook indicates that the company is actively navigating these challenges. However, their strategies would need to be monitored closely in the forthcoming quarters for signs of actual recovery and growth.

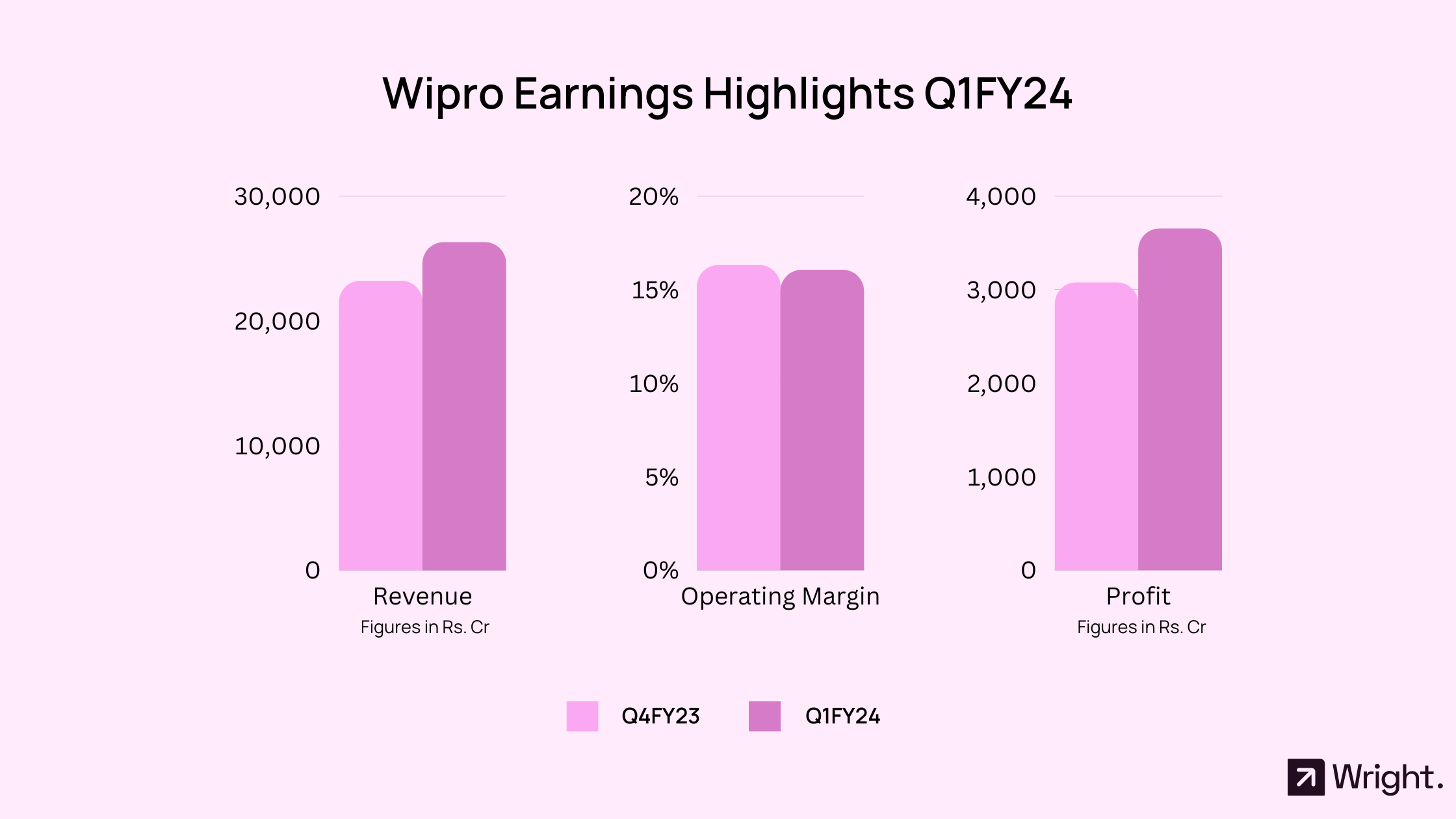

Wipro Q1 FY24 Earnings: A Mix of Performance and Bold Future Investments

The Azim Premji-backed IT giant reported a consolidated net profit of ₹2,870.1 crore, an 11.95% YoY increase, suggesting a strong ability to manage costs and maintain profitability even in the face of weakened demand. In terms of revenue, the company reported a 6.0% YoY growth, reaching ₹228.3 billion ($2.8 billion). The IT Services segment revenue saw a slight increase of 0.8% YoY to $2,778.5 million. This slow growth was anticipated, given the ongoing economic headwinds, and should be viewed as a positive indicator of Wipro's resilience.

The decrease in Non-GAAP constant currency IT Services segment revenue by 2.8% QoQ, however, indicates a slowdown that needs to be closely monitored in the coming quarters. Conversely, the YoY increase of 1.1% is in line with the broader IT services industry's performance. The Total Bookings and large deal bookings numbers, $3.7 billion and $1.2 billion respectively, were up by 9% YoY. These figures highlight Wipro's ability to secure major contracts in a competitive environment, setting the stage for potential future revenue growth.

Looking ahead to Q2 FY24, Wipro expects the IT Services business segment revenue to fall within the range of $2,722 million to $2,805 million. This prediction translates to a sequential guidance of -2.0% to +1.0% in constant currency terms. This cautious stance reflects the ongoing macroeconomic uncertainties and the potential impacts on Wipro's business. Wipro’s management has acknowledged the reduction in clients’ discretionary spending but also highlighted the company's new business momentum.

Notably, Wipro announced a significant $1 billion investment in AI over the next three years. This capital will be dedicated to strengthening the company's foundation in AI, data, and analytics capabilities, and constructing new consulting capabilities. The company has also unveiled Wipro ai360, an AI-first innovation ecosystem, promising to train its entire workforce of about 250,000 employees on AI within the next 12 months. These initiatives place Wipro at the forefront of the AI revolution, driving innovation, and fostering an AI-centric culture internally.

In conclusion, Wipro's Q1 FY24 performance was a blend of resilience, strategic growth initiatives, and some minor challenges. The company’s strategy of focusing on AI and operational improvements seems to be laying the groundwork for sustainable growth in the future, but the softening revenue environment could pose challenges. Thus, Wipro's management would need to continue leveraging their strengths and address any vulnerabilities to navigate the path ahead.

Tier 1 vs Tier 2 IT Companies

Interestingly, as we saw during the March quarter, analysts once again anticipate Tier-2 IT companies to outperform their Tier-1 peers. According to the trends, the Tier-2 IT companies have shown resilience and are expected to outperform their Tier-1 peers, registering a higher QoQ revenue growth. Motilal Oswal predicts Tier-2 IT companies to record a 2.8% quarter-on-quarter revenue growth, while Tier-1 companies' growth lags at a mere 0.2%.

Despite the expected outperformance of Tier-2 companies, many brokerages prefer to place their bets on Tier-1 companies. This preference stems from the anticipation that Tier-1 companies would have better profit margins, even though their revenue numbers may disappoint. From a profitability perspective, the ongoing wage hikes and weak topline are expected to exert margin pressure on IT companies. Yet, some, like LTI Mindtree, are expected to showcase margin expansion.

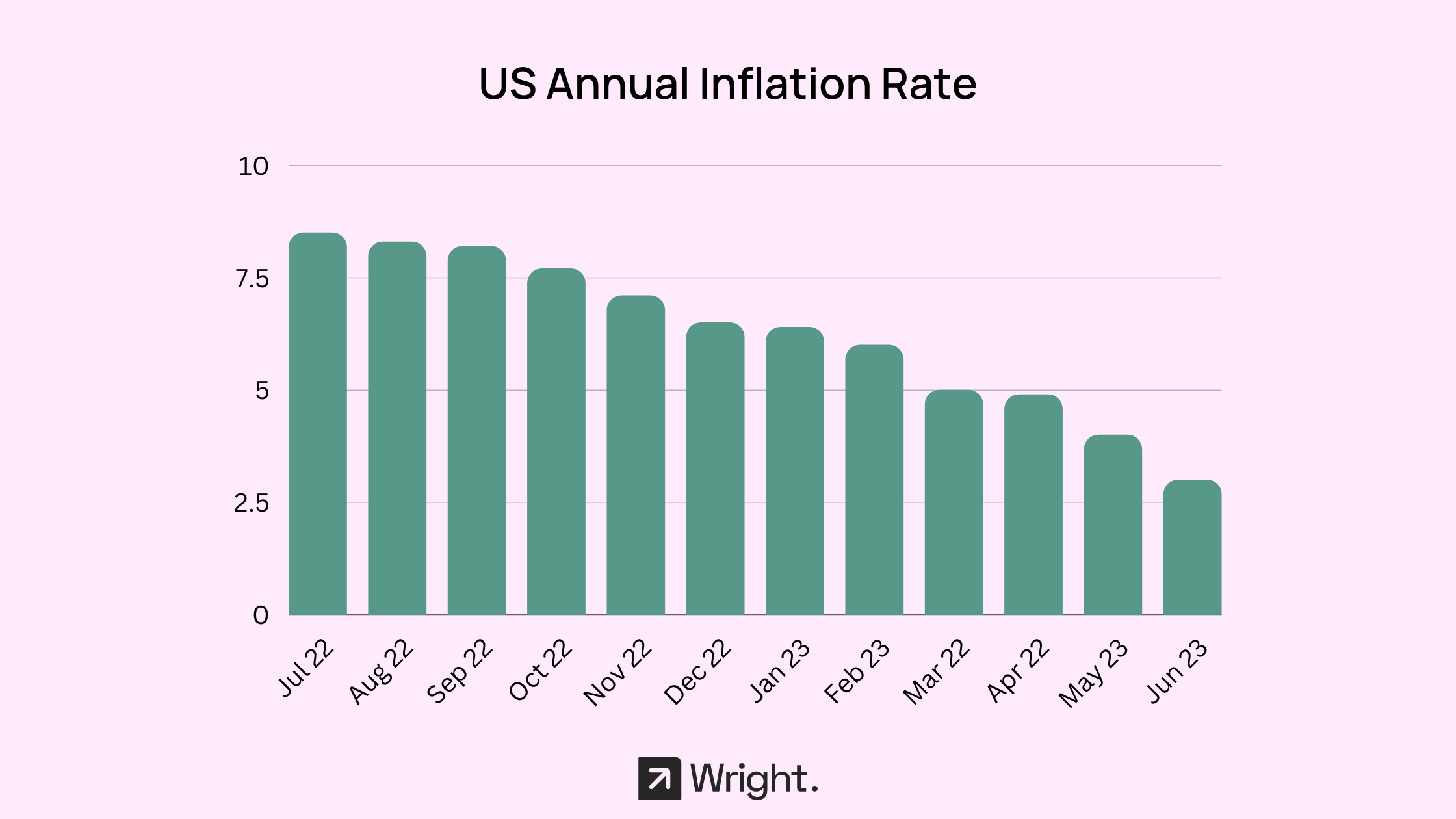

Finally, we cannot ignore the overarching global economic factors at play, such as inflation, which can considerably influence the business environment. On July 12, US inflation cooled more than expected last month. The consumer price index (CPI) measure of inflation eased to 3% annually — its lowest level since March 2021. This data fuels the likelihood that the US Federal Reserve will meet its 2% long-term inflation target sooner than predicted, potentially abbreviating its aggressive campaign of interest rate hikes.

Such dynamics bear significant implications for the Indian IT sector, given considerable exposure of Tier 1 IT companies to US markets. The cooler-than-expected inflation in the US could moderate the urgency of rate hikes, offering some relief to IT companies contending with cost pressures and potentially affecting the sector's earnings in the coming quarters

What to expect this earnings season for the IT Sector?

While the immediate outlook seems challenging, it's crucial to remember that the IT sector remains at the heart of digital transformation efforts worldwide. The demand for new technologies such as cloud, artificial intelligence , cybersecurity, and digital transformation initiatives continues to grow. The need for these services might alleviate some of the pressures faced by the sector, providing future revenue visibility

In a challenging global economic environment, the Indian IT sector's Q1 FY24 performance shows signs of resilience, adaptability, and strategic foresight. Despite pressures on profitability and slowdowns in certain verticals, companies are actively navigating these challenges, focusing on innovation and strategic investments in emerging AI technologies. The forthcoming quarters will be critical to watch as they may provide a clearer indication of actual recovery and growth in the sector.

The path to recovery for the IT sector remains a subject of debate. Some analysts predict a quicker recovery by the second half of this fiscal, while others anticipate a more gradual recovery, extending into FY25. This divergent outlook reflects the uncertainties that still surround the sector.

Therefore, as we navigate through this earnings season, it would be wise to adopt a cautious yet optimistic approach. It's worth noting that these cycles of ups and downs are inherent to any industry, and what matters most is the industry's ability to adapt and innovate amidst these challenges.

Stay tuned for updates as the sector's heavyweights, TCS and HCL, have released their results, and Wipro is set to announce theirs shortly. These announcements will undoubtedly offer a more precise understanding of the current state and the future direction of the Indian IT sector.

To invest in Alpha Prime , use code ALPHA25 to get a special discount!

WEBINAR + Q&A with Sonam Srivastava & Smallcase on Unleashing the Power of Momentum: Factors to Consider before Investing in Small Cap

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox