NEW INVEST WITH QUANT & AI STRATEGIES

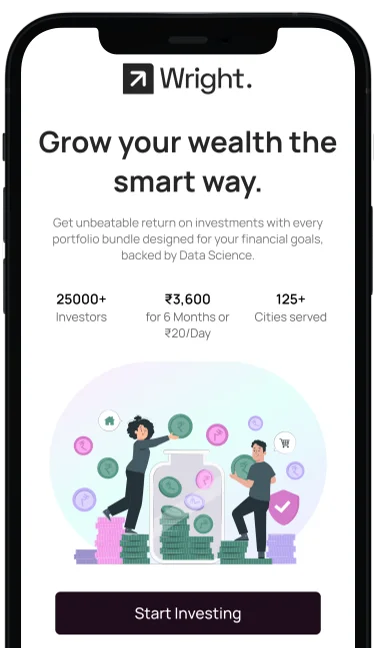

Grow Your Wealth

Grow Your Wealth

the Smart Way.

We're revolutionizing the way India invests with data and AI-driven quantitative models.

25,000+

Investors

₹3,600

for 6 Months or ₹20/Day

₹500 Cr+

Invested (AuA)

Our Trusted Financial Partners

Top Performing

Most Subscribed

15 Years +

Investing Experience

1

2

3

Why Invest with Wright Research?

Momentum Investing

Momentum is the strongest factor in India and an important part of our philosophy

Artificial Intelligence

We use AI & machine learning models to forecast risk and reward in the market.

Explore Our Portfolios

Find the best investment portfolios built for maximum returns at low risk.

Featured In

Trusted by 25k+ users

Other Blogs

Tracking Your Investments

On The Go

Unlock the power of research backed investment strategies. Download Now.

10K+ DOWNLOADS