by Siddharth Singh Bhaisora

Published On Feb. 27, 2026

Many investors fall into the trap of "set-and-forget" investing, especially when you have mutual funds in your portfolio. The assumption is that a well-chosen selection of funds at the outset will remain optimal for many years and the primary work of investing is completed. However, the dynamic nature of global markets and the inherent internal shifts within fund management styles mean that a static portfolio is a decaying one.

A detailed, systematic mutual fund portfolio review is imperative for any investor seeking to ensure their investments are aligned and operating at peak efficiency. Without active oversight, even the most promising portfolios can succumb to style drift, where the original asset allocation and risk parameters become disconnected from the current economic reality. So let’s look at this in depth today.

Market shifts can lead to involuntary concentration in certain sectors which become dangerously overallocated due to price appreciation. Consistency of mutual fund managers is never guaranteed, a top-performing fund today may suffer from leadership changes or asset size that hampers its ability to generate meaningful alpha tomorrow.

By conducting a rigorous portfolio review, an investor moves from a reactive stance, often characterized by anxiety during market volatility, to a proactive strategy. This alignment ensures that the legacy structure of the portfolio is continuously audited against personal risk tolerance and the evolving benchmark landscapes. The objective is to transform a fragmented collection of assets into a synchronized, high-performance financial engine.

This transition requires a departure from subjective feelings about market trends and a move toward a cold, analytical assessment of performance metrics. To achieve this, we must look beyond simple trailing returns and investigate the quantitative pillars that define the true health and sustainability of an investment portfolio.

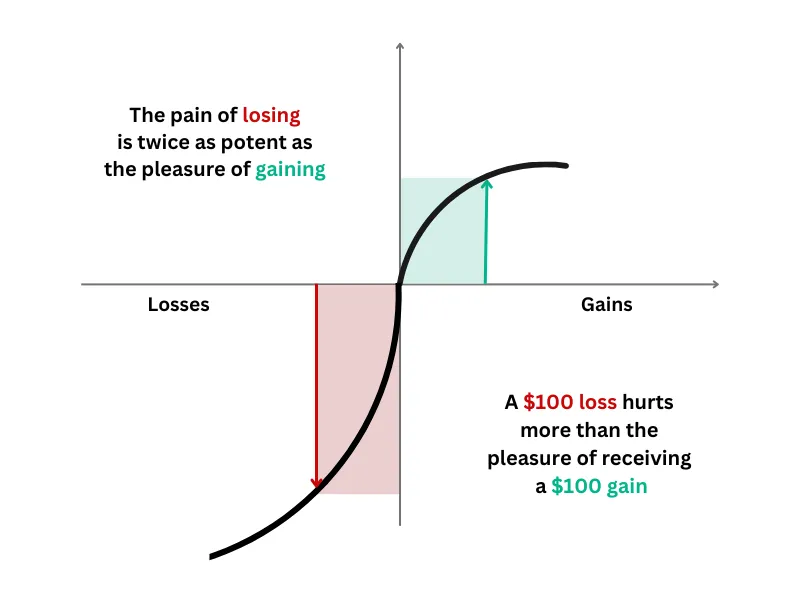

The behavioral finance literature has shown that the frequency with which investors evaluate their investments matters a great deal to their decision-making quality. Richard Thaler and Shlomo Benartzi’s work on myopic loss aversion famously demonstrated that when investors assess their portfolios very frequently, they experience gains and losses more often in their mental accounting, and this tendency can distort decision-making over longer horizons.

Investors with loss aversion preferences value losses more intensely than equivalent gains, and when they evaluate their investment outcomes frequently, they are exposed to short-term fluctuations that feel like losses, even if the long-term trajectory of the investment is positive.

Under these conditions, investors behave as if they are risk-averse in the short term and reduce their exposure to equities or other risky assets because the frequent negative feedback makes risk feel larger and more immediate than it intrinsically is. This effect was proposed initially to help explain the equity premium puzzle but has deep implications for how reviewing frequency affects real investment behavior.

Subsequent studies have corroborated the idea that evaluating outcomes more often leads to more conservative choices, even for identical underlying investments.

Classic experimental research where subjects were given repeated gambles but varied the frequency of feedback found that participants who saw outcomes more frequently tended to take less risk than those who saw aggregated outcomes over longer intervals.

Frequent feedback generates pings of negative outcomes that loom psychologically larger than equally probable positive outcomes, driving choices that avoid risk in a way that is inconsistent with an optimal long-term plan.

This repeated exposure to “loss frames” can fuel a desire to exit or alter holdings prematurely, even though the long-term expected returns of the fund remain unchanged.

Research examining investor flows in actual mutual fund markets also aligns with this theory. Studies on investor behavior have documented the strong sensitivity of flows to past performance, where investors, especially retail investors, tend to reduce contributions or switch funds based on recent poor performance signals. This behavior can be understood through the lens of myopic loss aversion - frequent evaluation makes investors overly responsive to negative short-term signals, leading to flow behaviour that exacerbates market volatility and harms long-term outcomes.

When investors adopt frequent performance checking as part of their review routine — for example, looking monthly at fund returns, they are implicitly inviting noise into their decision framework, where normal ups and downs in relative performance may be mistaken for meaningful changes in a fund’s prospects.

The point isn’t that investors should never check their portfolios. Rather, frequent performance evaluation is not neutral, it changes the psychological context in which decisions are made and tends to skew judgments toward pessimism and reactive behavior.

For mutual funds, where returns inherently fluctuate and short periods of underperformance are common, the psychological weight of those frequent evaluations leads not only to stress but to decisions that often lock in losses rather than contributing to better long-term wealth accumulation. The research therefore suggests that review routines should minimize unnecessary exposure to short-term noise and be designed to focus on structural, not momentary, changes to a fund’s characteristics.

Mutual funds, like any portfolio of risky assets, produce returns that vary over time due to a combination of market forces and specific portfolio choices.

Much of the variation in mutual fund returns over short horizons is attributable to common risk factors and randomness rather than persistent managerial skill. Apparent short-term performance continuation is often driven by exposures to systematic factors, and once these are accounted for, the amount of genuine persistence attributable to managerial skill shrinks dramatically. In practical terms, this means that a fund that hasn’t done well or has done well in the past 6 months has a high likelihood of reflecting market exposures over that period rather than something that will persist indefinitely.

If the return differences among funds over 6 months or 1 year are largely driven by transient market conditions or sampling variability rather than enduring skill, then reacting to those differences by rebalancing or switching funds is likely to amount to chasing luck rather than harvesting skill.

Early performance studies, including Fama and French’s work on luck versus skill, found that when expenses and factor exposures are properly controlled for, relatively few funds exhibit statistically significant skill that persists over time. Consequently, short-term performance is a noisy signal with poor predictive validity for future risk-adjusted returns.

Moreover survivorship bias, the tendency for poorly performing or closed funds to drop out of datasets and bias observed persistence upward, further clouds the reliability of short-term performance as a basis for decision-making. Mutual fund performance measurement has long warned that ignoring funds that have closed because of poor performance leads to an overly optimistic view of available funds. When such biases are corrected, the already limited evidence of meaningful persistence becomes even weaker. This reinforces the idea that short periods of relative outperformance should be interpreted cautiously and not as a robust reason to overhaul a portfolio.

Empirical work has found that investors’ flow responses to recent returns are highly sensitive to the volatility of those returns. In other words, investors tend to rush into funds with strong recent performance and flee from those with weak performance, but these flows are dampened when returns are more volatile, suggesting a recognition, whether conscious or not, that short-term performance becomes less informative under high volatility. This pattern supports the view that short-term performance rankings do not reliably reflect enduring quality differences among funds, and acting on them can lead to suboptimal trading behaviour.

When the psychological tendency to overreact to short-term losses (myopic loss aversion) is combined with the statistical reality that short-term mutual fund performance contains a high level of noise and limited persistence, a clear implication emerges: frequent performance-based reviews are counterproductive for most investors.

If a review routine focuses on recent returns, it increases the likelihood that decisions will be driven by short-term noise and emotional responses to perceived “losses” rather than structural changes in the underlying investment or investment strategy.

Academic research thus suggests that mutual fund portfolios should be evaluated over longer horizons that allow the signal (meaningful performance characteristics, process adherence, structural drift) to emerge more clearly against the noise of short-term fluctuations.

Because of this statistical property of mutual fund returns, reviewing mutual fund portfolios should happen no more often than once every 3 to 6 months, depending on the investor’s objectives and the investment style being assessed. Quarterly reviews are often cited as a balanced frequency because they allow investors to detect meaningful return patterns over time without being overwhelmed by short-term volatility that lacks predictive power.

Collectively, the data suggest that while observation can be frequent, decision-linked reviews should be spaced to match the statistical reliability of the performance signals, generally on a quarterly to annual basis.

Wright’s Mutual Fund Review tool provides a comprehensive, data-driven diagnostic for mutual fund portfolios, combining quantitative metrics with qualitative assessments to optimize investment health. By leveraging a multi-faceted analytical framework, users can achieve a clear understanding of their portfolio's current standing and necessary improvements.

The Health Score summarizes the quality of individual funds and the entire portfolio based on risk-adjusted returns, alpha generation, and consistency. This score acts as a "quality flag," allowing users to quickly see if their funds are leading their peers or lagging behind in the bottom quartile. We focus on several factors, among which are:

Sharpe Ratio – Are returns adequate for the level of risk?

Alpha – Is the fund outperforming its benchmark after adjusting for risk?

Standard Deviation & Maximum Drawdown – How volatile is the fund, and how well does it protect on the downside?

Consistency – Does the fund beat its benchmark in at least half of recent periods?

Risk profiling also guides optimal asset allocation, aggressive investors may lean toward small- and mid-cap funds, while conservative investors prioritize index funds and debt schemes. A review further detects overconcentration in high-risk categories, helping prevent major losses during market downturns.

Additionally, the tool identifies "Funds at Risk" schemes burdened by high volatility, high expense ratios, or persistent underperformance - offering clear Buy, Sell, or Hold recommendations to guide restructuring.

Users can detect hidden concentration risks through the Diversification Score, which evaluates fund count, sector exposure, and determines the “true" diversification. Penalties are automatically applied for overconcentration in single sectors or asset classes, revealing if a portfolio is dangerously reliant on a few holdings.

Finally, the tool enhances transparency and cost efficiency by flagging high expense ratios and identifying regular plans that could be converted to direct plans to increase net returns. With features like automated transaction imports and performance charts benchmarked against the Nifty 50, users receive a holistic Investment Score and actionable insights to rebalance their wealth effectively.

This deeper analysis exposes funds that may look strong in bull markets but underperform peers or benchmarks. When weighted by allocation, these factors generate a Portfolio Health Score that highlights whether restructuring or fund replacement is necessary.

Chief Marketing & Growth Officer | Wright Research

Learn more about our Chief Marketing Officer, Siddharth Singh Bhaisora. Siddharth is a highly experienced investment advisor.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart