Every year, UNCTAD, the UN's trade and development body, publishes its World Investment Report, the most complete picture available of foreign direct investment: companies building factories abroad, buying businesses across borders, and funding infrastructure they will operate for decades. The 2026 report looks reassuring at a first glance. Global FDI rose 6% in 2025 to $1.6 trillion, after two consecutive years of decline.

However, the recovery was narrow, concentrated in a handful of countries and sectors, and driven by a small number of very large projects. Let’s look at why the money is flowing where it is, and where India fits in.

Global investment in 2025 at a glance

Indicator | Reading |

Global FDI inflows | $1.6 trillion, up 6% (up 4% excluding conduit flows) |

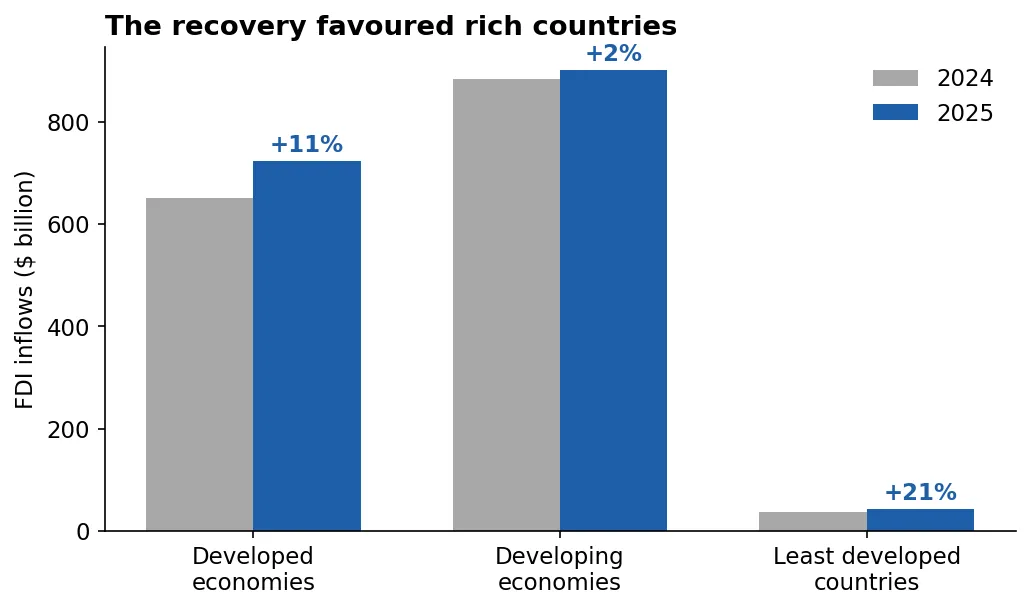

Developed economies | $723 billion, up 11% |

Developing economies | $901 billion, up 2% |

Least developed countries | $43 billion, up 21% (under 3% of the global total) |

Strategic sectors, share of greenfield investment | 44%, up from 16% in 2020 |

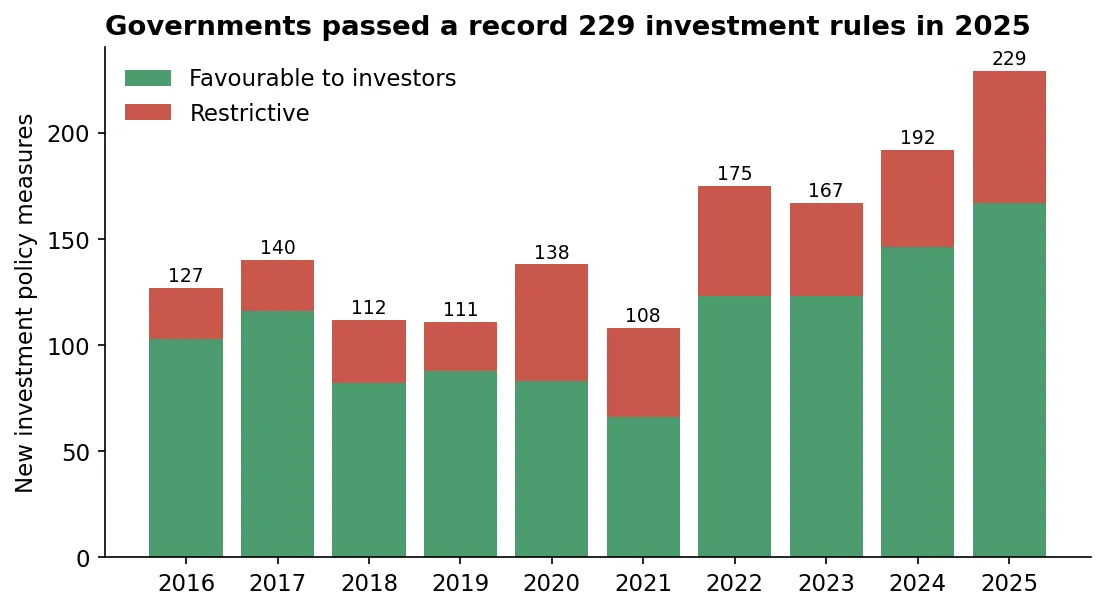

New investment policy measures | 229, the highest on record |

Economies with FDI screening regimes | 52, up from 21 in 2016 |

India, FDI inflows | $39 billion, up 44%, 11th largest recipient |

Did global investment really recover in 2025?

Partly. Two adjustments shrink the headline considerably.

The first is what economists call conduit flows. A large multinational routes billions through a financial hub such as Switzerland or Ireland for tax or treasury reasons. The money crosses a border, so it counts as investment, yet it builds nothing and employs nobody. UNCTAD strips these flows out and finds that underlying global FDI grew 4%, with Switzerland and Ireland accounting for most of the gap between the two figures.

The second is concentration. The top 20 host economies attracted more than 80% of global FDI in 2025. Inflows to developed economies rose 11% to $723 billion, lifted by a few megaprojects in AI-related infrastructure. Inflows to developing economies grew 2% to $901 billion.

The underlying activity data reinforces the caution. Cross-border mergers and acquisitions fell 7% to $421 billion, and while the value of announced greenfield projects edged up, the number of projects fell 10%. Fewer, larger commitments are propping up the totals. UNCTAD also notes that the rate of return on inward FDI dropped to 7% in 2025, from above 10% in the three preceding years, which weakens the incentive for the broad population of firms to expand abroad even as the largest multinationals keep reporting record profits.

FDI inflows by country group. Data: UNCTAD World Investment Report 2026

The poorest countries received the smallest slice

Flows to the 44 least developed countries rose 21%, which sounds encouraging until you see the base: $43 billion in total, under 3% of the global figure, concentrated in a few resource-rich economies and directed mostly at oil, gas and mineral extraction. This matters because FDI carries far more weight in poor countries. It supplies roughly half of all external finance reaching the developing world, and it is often the only realistic route to funding power grids, ports and factories. When it stalls, development stalls with it.

Why is AI swallowing global investment?

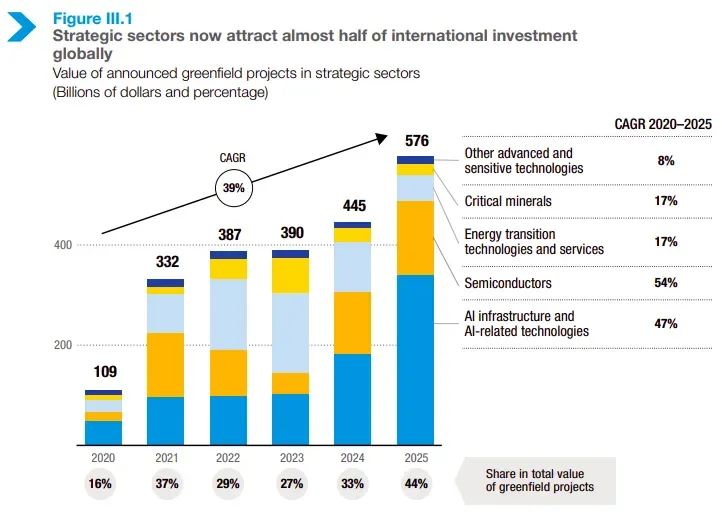

AI infrastructure, semiconductors, critical minerals, clean energy technologies and other sensitive technologies are grouped together under one strategic sector. The shift toward them is the central finding.

Announced greenfield investment in strategic sectors rose from $109 billion in 2020 to $576 billion in 2025. As a share of all new project investment worldwide, that is a jump from 16% to 44%. AI infrastructure alone, mainly data centres and the cloud and power systems around them, reached almost $350 billion, about three fifths of the strategic total. Semiconductors grew fastest, expanding 54% a year over the period.

This money clusters in very few places

A hyperscale data centre needs land, enormous and reliable electricity supply, water for cooling, and an ecosystem of engineers and suppliers. Few countries offer all of these at once, so the investment piles into the same locations. In 2025, the top three recipient economies captured an average of 56% of greenfield value in strategic sectors, against 34% in other sectors. On the source side the funnel is tighter still, with the top three investor economies supplying 72%. Low-income and lower-middle-income countries attracted only about 10% of strategic-sector investment during 2020 to 2025, compared with more than 20% of investment in everything else.

The old route to development is narrowing

For decades, the standard path for a poor country was to offer competitive labour costs, attract foreign manufacturers, and let jobs and skills accumulate. That path is contracting. Greenfield investment in manufacturing outside the strategic sectors, which covers textiles, garments, basic electronics and similar industries, has declined over the past decade. The capital that once sought low-cost production now seeks chips, compute and minerals, and those investments go where capabilities already exist.

The investors themselves are changing too. More than a quarter of the companies in UNCTAD's ranking of the world's 100 largest multinationals are now at least partly state-owned, and private equity firms account for roughly 20% of cross-border mergers and acquisitions.

How are governments redirecting the flow of money?

Actively, and on a record scale. Governments in 104 countries adopted 229 investment policy measures in 2025, the highest annual count UNCTAD has ever recorded. Around 73% of measures remained favourable to investors, but their character has changed. Half of all favourable measures were incentives, and these are now tightly targeted at clean energy, digital infrastructure, advanced manufacturing and critical minerals rather than offered economy-wide.

The direction of the incentives also differs by income level. Rich countries can afford to compete with cash, offering grants and tax credits worth billions to chipmakers and battery manufacturers on the condition that plants are built at home. Developing countries generally lose that kind of bidding war, so many are redesigning their offer instead. Rather than granting blanket tax holidays that drain revenue for a decade, they increasingly tie benefits to performance: the investor keeps the incentive only if it hires local workers, transfers technology or sources from domestic suppliers.

National investment policy measures by nature. Data: UNCTAD Investment Policy Monitor

Screening regimes have more than doubled

The restrictive side is growing faster. In 2016, 21 economies operated a mechanism to screen foreign investment on national security grounds. By 2025 that number had reached 52. The definition of a sensitive asset has widened alongside, and now routinely covers data centres, AI firms, telecom networks and lithium mines. Few transactions are formally blocked, but the reviews slow deals, raise legal costs and make some buyers walk away before a decision is ever issued.

Old treaties still bite, mostly for poorer countries

Older investment treaties allow a foreign company to sue a host government in international arbitration when policy changes hurt its profits. Investors filed 56 such cases in 2025, and about 80% were brought against developing countries, well above the historical average. Roughly a third involved extractive activities, including the mining of critical minerals. A poor country that tightens environmental rules around a mine can find itself defending a multi-billion-dollar claim.

What is India’s Outlook?

India looks strong. FDI inflows rose 44% in 2025 to $39 billion on UNCTAD's net measure, making India the 11th largest recipient in the world. India's own commerce ministry, which counts gross inflows including reinvested earnings, reported $58.85 billion for FY2025-26, up 18% on the year. Both series point in the same direction.

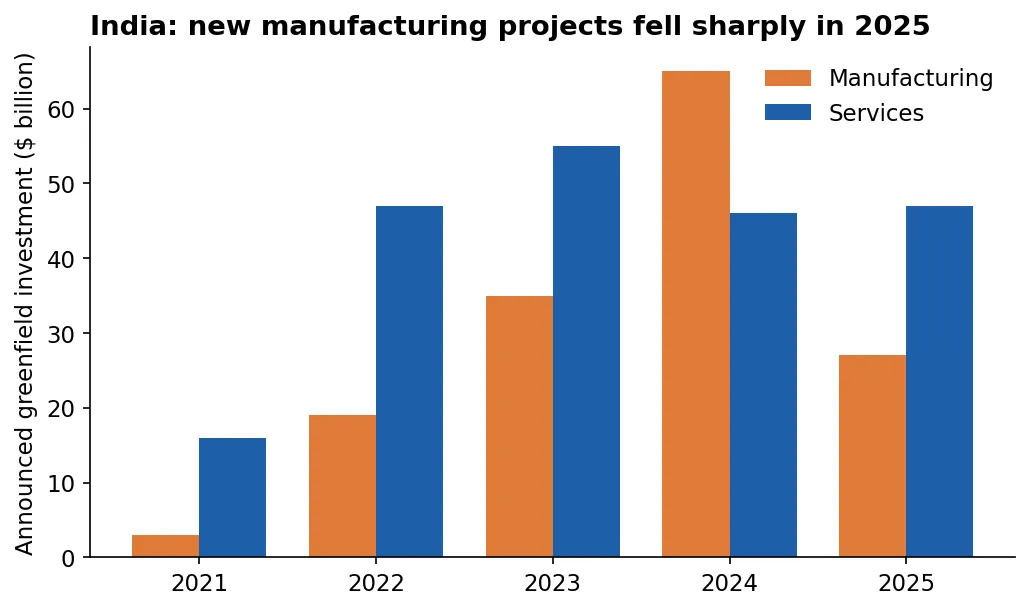

The project data tells a more cautious story. The value of announced greenfield projects in India fell from about $111 billion in 2024 to roughly $74 billion in 2025. Manufacturing accounted for almost the entire drop, sliding from $65 billion to $27 billion, while services held steady and information and communication technology became the largest single sector.

India: announced greenfield investment by sector. Data: UNCTAD, based on fDi Markets

India sits on the right side of two forces. Supply chain reconfiguration is bringing production out of concentrated hubs, and India gains from this alongside Malaysia and Thailand. The AI buildout is arriving as well: the largest greenfield project announced in developing Asia in 2025 was Alphabet's $14.5 billion data centre investment in India. The 2025 dip in manufacturing announcements reflects tariff uncertainty and weaker global sentiment rather than a reversal of these trends, though it is a reminder that announced intentions convert into factories only when the policy environment stays predictable.

Where does global investment go from here?

UNCTAD's outlook for 2026 is guarded. The escalation of conflict in the Middle East has raised shipping, insurance and energy costs, and trade policy remains volatile. Bankers expect cross-border dealmaking to recover as financing costs ease, but the deals will stay selective and heavily screened.

The strategic-sector pull will strengthen before it fades. The four largest cloud providers plan capital spending of as much as $630 billion in 2026, most of it on AI infrastructure, up from roughly $388 billion in 2025. Capital on that scale will keep flowing to the small set of countries able to host it.

A few developing countries are converting specific advantages into investment. Kenya generates almost 90% of its electricity from clean sources and is marketing that to data centre operators under pressure to decarbonise. Indonesia's ban on raw nickel exports forced battery makers to build processing capacity inside the country. These cases share a pattern: leverage came from a real asset plus a deliberate policy, and neither country tried to win a subsidy race it could never afford.

The world is investing more money in fewer places and fewer things, and the reasons have shifted from growth toward security. For most developing countries, the practical response is to attach conditions to the investment they do receive, build the power, skills and institutions that strategic investors require, and integrate regionally so that small markets can offer scale. $1.6 trillion is moving again, and most of the world will have to work harder than ever to attract it.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox