Smallcase, mutual funds, and direct stocks differ in ownership, cost, and tax treatment. Portfolio management services, active portfolio management, and a well-built diversified mutual fund portfolio each serve distinct investor profiles. This guide compares PMS services, high-return mutual funds, balanced mutual funds, and PMS in investment to help Indian investors choose the structure that builds the most wealth long-term.

Introduction

You've probably had this thought at least once: "Should I just buy the stocks myself, put money in a mutual fund, or try one of those Smallcase portfolios I keep seeing ads for?" It's a fair question, and the answer matters far more than most people realise.

Because what looks like a simple choice between three investment options is actually a choice between three fundamentally different ownership models, cost structures, taxation regimes, and long-term wealth outcomes. The best financial advisor in India will tell you that getting this choice right early can mean the difference of several crores by the time you retire.

Whether you are a salaried professional exploring a mutual fund portfolio, an HNI looking into PMS services, or a curious investor evaluating the Smallcase ecosystem, this guide will give you a clear, honest breakdown of each option so you can make a decision grounded in facts, not marketing.

What You Actually Own: Mutual Fund Units vs Smallcase vs Demat Holdings Explained

In a mutual fund, you do not own stocks. You own units. The AMC pools your money with thousands of other investors, buys stocks on your behalf, and represents your stake through a Net Asset Value (NAV).

Your mutual funds portfolio is reflected as units of this NAV. You have no direct ownership of the underlying companies, no AGM voting rights, and no control over what gets bought or sold.

A Smallcase works very differently. When you invest in a Smallcase, the stocks are credited directly to your demat account. You are the legal owner of every share in the basket.

The Smallcase manager, a SEBI-registered investment advisor or research analyst, designs and rebalances the portfolio, but ownership always rests with you.

Direct equity investing gives you the same demat-level ownership as a Smallcase, but without the guided structure.

Portfolio management services sit at an entirely different level.

Under a formal SEBI-regulated PMS agreement, the portfolio manager invests directly in your demat account on your behalf.

You hold the actual securities. The manager makes buy/sell decisions, but all assets remain in your name.

This is the clearest form of professional management with direct ownership.

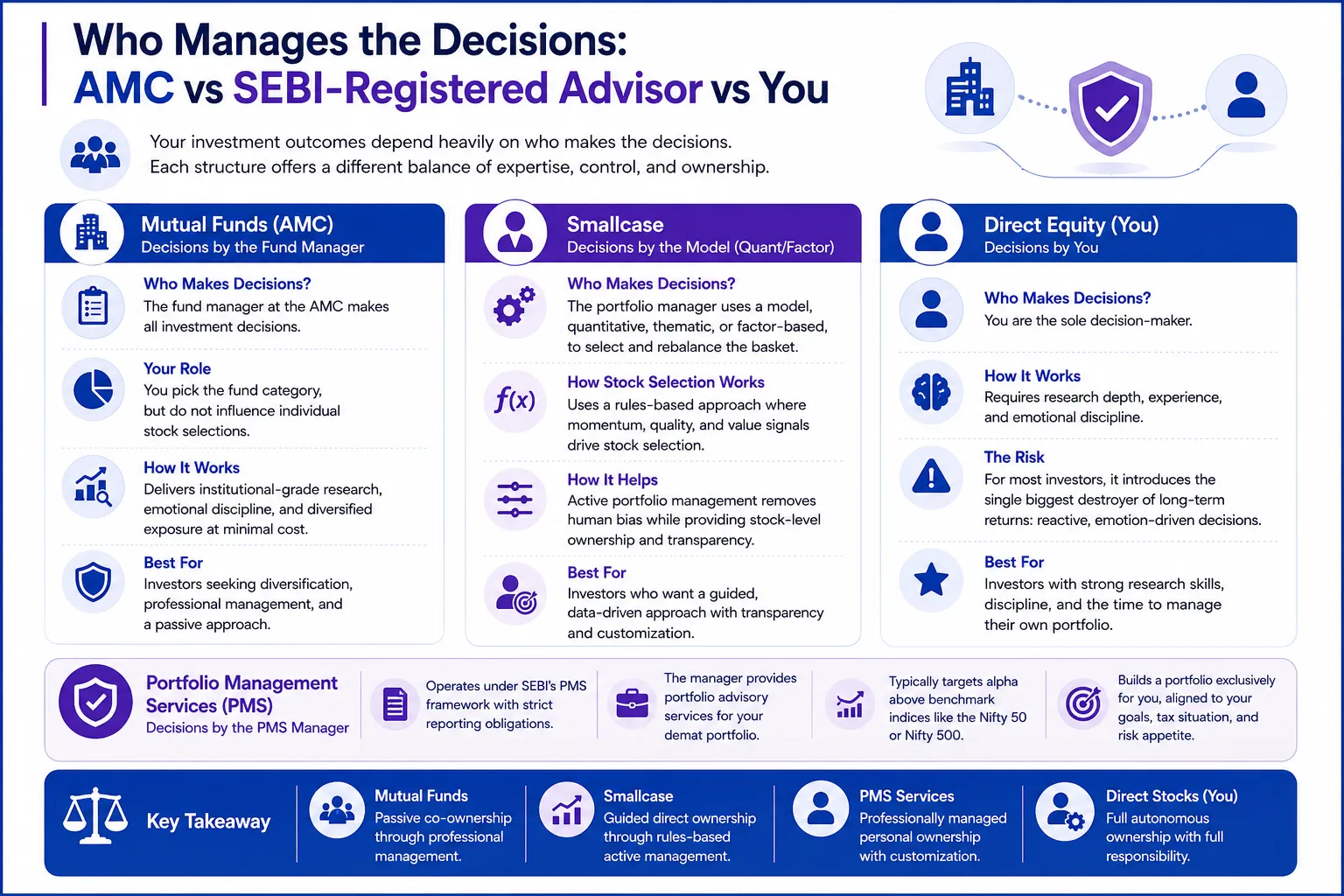

Who Manages the Decisions: AMC vs SEBI-Registered Advisor vs You

In a mutual fund, a fund manager at the AMC makes all investment decisions. You pick the fund category, but you do not influence individual stock selections. For investors building a diversified mutual fund portfolio, this is actually an advantage; it removes emotional decision-making and delivers institutional-grade research at minimal cost.

In a Smallcase, the portfolio manager uses a model, quantitative, thematic, or factor-based, to select and rebalance the basket. Wright Research, for instance, uses a quant/factor-driven approach where momentum, quality, and value signals drive stock selection. This form of active portfolio management removes human bias while giving investors stock-level ownership and transparency.

In direct equity, you are the sole decision-maker. For investors with genuine research depth and emotional discipline, this works well. For most others, it introduces the single biggest destroyer of long-term returns: reactive, emotion-driven decisions.

Portfolio management services providers operate under SEBI's PMS framework with strict reporting obligations. The manager applies portfolio advisory services to manage your demat portfolio, typically targeting alpha above benchmark indices like the Nifty 50 or Nifty 500. The distinction is critical: unlike a mutual fund manager who manages pooled capital, a PMS manager builds a portfolio exclusively for you, aligned to your specific goals, tax situation, and risk appetite.

Think of it this way, mutual funds give you passive co-ownership, Smallcase gives you guided direct ownership, PMS services give you professionally managed personal ownership, and direct stocks give you full autonomous ownership.

Cost Comparison: PMS Charges, Expense Ratios and Brokerage Across All Three

Cost is where most investors get surprised, and where the choice between these three structures often gets made.

A mutual funds portfolio built on regular plans carries an expense ratio of 1% to 2.5% per annum. Direct plans reduce this to 0.1%–1%. The cost is embedded in the NAV, so you never see it as a line item, but it silently compounds against your returns every year.

High return mutual funds in the active mid-cap and flexi-cap categories tend to have higher expense ratios but aim to justify them through outperformance. Balanced mutual funds (hybrid or balanced advantage funds) typically have expense ratios between 0.5%–1.5% for direct plans.

Smallcase investing incurs brokerage on each stock transaction plus a subscription fee to the manager, typically Rs. 100–Rs. 500 per rebalance or an annual subscription. These costs are explicit and visible, which is a strength (no hidden fees) but can add up meaningfully if rebalances are frequent.

PMS charges are the most complex to decode and the most important to understand before committing to Rs. 50 lakh. A standard PMS fee structure includes a fixed management fee of 1%–2% per annum and a performance fee of 10%–20% of gains above a defined hurdle rate.

PMS charges are SEBI-regulated, and providers must disclose every charge in the disclosure document. While PMS charges appear high relative to mutual fund expense ratios, the value lies in personalised active portfolio management that targets returns commensurate with the premium.

A category worth separate attention is FIPMS, Fixed Income Portfolio Management Services. FIPMs refers to PMS strategies built around debt instruments: bonds, debentures, structured credit, and other fixed income assets.

Fipms is designed for HNI investors seeking predictable income streams with professional management, sitting between a debt mutual fund and direct bond investing. If you are exploring fixed income options beyond balanced mutual funds, FIPMs solutions offer a structured, professionally managed alternative.

Parameter |

Mutual Funds |

Smallcase |

PMS |

Annual Cost |

0.1%–2.5% (expense ratio) |

Rs. 200–Rs. 2,000/yr + brokerage |

1–2% fixed + 10–20% performance fee |

Minimum Investment |

Rs. 500 SIP |

Rs. 1,000–Rs. 50,000+ |

Rs. 50 lakh (SEBI mandated) |

Cost Visibility |

Hidden in NAV |

Explicit per transaction |

Explicit, disclosed in agreement |

Tax Efficiency |

Moderate |

Lower (per-stock events) |

Moderate–High |

Transparency: Can You See Exactly What You Hold in Your Mutual Funds Portfolio?

This is where mutual funds fall short for investors who want to understand their own portfolios. A mutual funds portfolio shows you the NAV and returns, but to see what stocks the fund holds, you need to dig into the monthly factsheet, and even then, you're looking at last month's data with a 30-day lag.

Smallcase offers real-time visibility. Since the stocks live in your demat account, you can log in at any moment and see every holding. Leading investment research firms in India that manage Smallcase portfolios provide detailed rebalance notes with clear rationale, which stocks were added, which were removed, and why.

Portfolio management services deliver the gold standard in transparency. SEBI mandates detailed monthly reporting for all PMS providers, every stock, every transaction, every fee, and portfolio performance versus the benchmark, all in a single report.

If you work with the right portfolio advisory services provider, transparency extends to the decision-making process itself, not just the outcomes.

Direct equity gives you full ownership visibility. But without the analytical infrastructure that investment research firms in India and a reliable best stock advisor in India bring, that visibility can be more intimidating than useful for most investors.

Wright Research publishes rebalance rationale and portfolio commentary for its smallcase portfolios and provides full reporting for its PMS services, so investors are never left wondering why a decision was made.

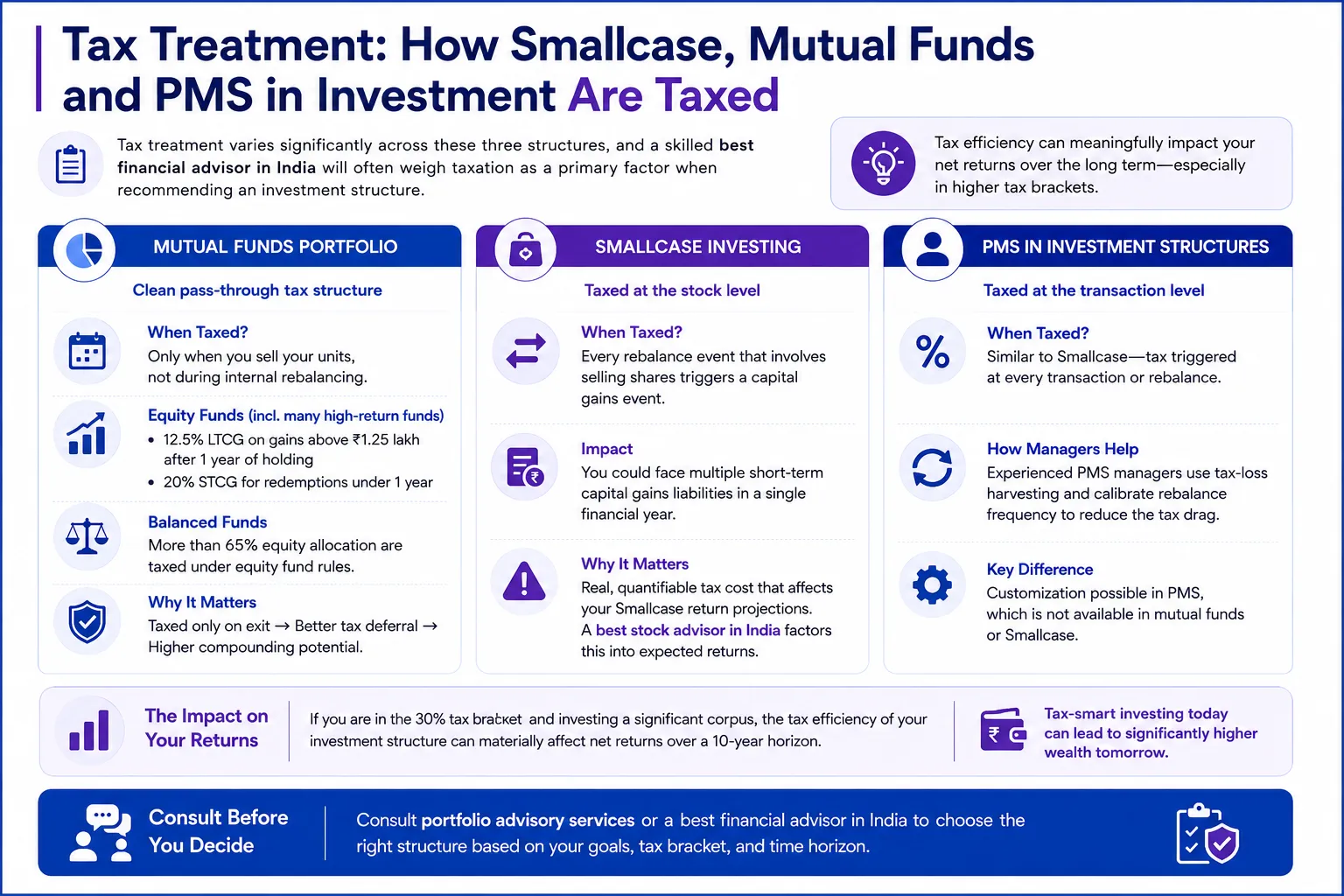

Tax Treatment: How Smallcase, Mutual Funds and PMS in Investment Are Taxed

Tax treatment varies significantly across these three structures, and a skilled best financial advisor in India will often weigh taxation as a primary factor when recommending an investment structure.

A mutual funds portfolio benefits from a clean pass-through tax structure; you are taxed only when you sell your units, not when the fund internally rebalances. Equity mutual funds (including many high-return mutual funds) attract 12.5% LTCG on gains above Rs. 1.25 lakh after one year of holding, and 20% STCG for redemptions under one year. Balanced mutual funds with more than 65% equity allocation are taxed under equity fund rules.

Smallcase investing is taxed at the stock level. Every rebalance event that involves selling shares triggers a capital gains event, which means you could face multiple short-term capital gains liabilities in a single financial year. This is a real, quantifiable cost that the best stock advisor in India factors into their Smallcase return projections.

PMS in investment structures are also taxed at the transaction level, similar to Smallcase. However, many experienced PMS managers build tax-loss harvesting strategies and calibrate rebalance frequency to reduce the tax drag, something a mutual fund or Smallcase manager typically cannot customize for you individually.

If you are in the 30% tax bracket and investing a significant corpus, the tax efficiency of your investment structure can materially affect net returns over a 10-year horizon. This alone is a reason to consult portfolio advisory services before deciding.

Minimum Investment, Liquidity, and Exit Terms Compared

Mutual funds are the most accessible investment structure available to Indian investors. SIPs start at Rs. 500, and even lump sum investments can begin with Rs. 1,000. Building a best mutual fund portfolio is genuinely within reach for anyone with a bank account.

Smallcase entry points vary; some portfolios start at Rs. 2,000–Rs. 5,000, while premium or diversified Smallcase portfolios may require Rs. 25,000–Rs. 1 lakh depending on the stocks in the basket.

A diversified mutual fund portfolio across four or five fund categories requires less capital than a comparably diversified Smallcase.

Portfolio management services, as mandated by SEBI, require a minimum investment of Rs. 50 lakh. This positions PMS squarely for HNI investors. On liquidity: open-ended mutual funds allow full redemption on any business day. Smallcase stocks can be sold anytime markets are open. PMS agreements include lock-in periods and exit load clauses that must be read carefully before signing.

Which Structure Builds More Wealth Over 10 Years? A Data-Driven Look

Here is the honest, data-grounded answer: the structure alone does not determine your wealth outcomes. The quality of the fund, the manager, and, most critically, your consistency in staying invested does.

High return mutual funds in the active flexi-cap and mid-cap categories have historically delivered 12%–16% CAGR over 10-year rolling periods, according to AMFI data. A best mutual fund portfolio combining an index fund core with active mid-cap and small-cap satellite positions has the potential to outperform inflation substantially over a decade.

Diversified mutual fund portfolio strategies that use SIPs across fund categories benefit enormously from rupee-cost averaging and compounding, the power of time in the market over timing the market.

Smallcase portfolios built on systematic, factor-based models have shown the potential to deliver returns above benchmark indices in certain market conditions. However, the transaction costs and tax drag from rebalancing can erode the gross return advantage meaningfully over long periods.

Portfolio management services , given the ability to concentrate capital in high-conviction positions and apply disciplined active portfolio management, have the structural potential to generate the highest risk-adjusted returns for large corpus investors. But this comes with commensurate risk and a higher minimum investment.

Both the best stock advisor in India and the best financial advisor in India agree: for investors with Rs. 50 lakh or more, PMS services offer personalisation that no pooled vehicle can match.

What consistent data across all three vehicles shows is this: investors who stayed fully invested through market cycles, regardless of structure, significantly outperformed those who timed, switched, or exited during corrections.

Which Is Right for You? A Decision Table by Investor Profile

Investor Profile |

Recommended Structure |

Why |

First-time investor, Rs. 500–Rs. 10,000/month |

Mutual Funds (SIP in index + active flexi-cap) |

Lowest entry, diversification, zero effort |

Salaried professional, Rs. 25,000–Rs. 1L/month |

Smallcase + diversified mutual fund portfolio combo |

Direct ownership with guided management |

HNI investor, Rs. 50L+ to deploy |

Portfolio management services |

Personalised active portfolio management, full transparency |

Experienced DIY investor |

Direct Stocks |

Full control, no intermediary cost |

HNI seeking fixed income |

Fipms (Fixed Income PMS) |

Fipms offers professional debt management for large corpuses |

An investor wanting structured guidance |

Portfolio advisory services |

Research-backed, SEBI-registered advice |

No single structure is universally correct. The right answer for most investors is a combination, often a core mutual funds portfolio for systematic wealth building and a satellite allocation to Smallcase or PMS services as corpus grows. If you are uncertain which profile fits you, a conversation with one of the leading investment research firms in India is the most efficient next step.

Conclusion

Choosing between Smallcase, mutual funds, and direct stocks is not really a question of which is "better" in isolation; it is a question of which is right for you, at this stage of your financial journey, with your specific corpus, tax profile, and return expectations.

Mutual funds are the foundation most investors should build on, accessible, diversified, and professionally managed at minimal cost. Smallcase adds a layer of direct ownership and thematic focus for investors ready to go beyond the standard mutual funds portfolio. Portfolio management services represent the pinnacle of personalised wealth management, suited for HNI investors who want their Rs. 50 lakh or more actively managed by a SEBI-registered expert applying institutional-grade active portfolio management to their individual demat account.

What ties all three together is the principle that no investment structure compounds well without time, consistency, and the right portfolio advisory services guiding your decisions. Wright Research, as one of the trusted investment research firms in India, is built precisely to help investors navigate this choice, with quant-driven rigour, full transparency, and the depth you would expect from the best financial advisor in India. The right structure, aligned to the right strategy, executed with discipline, that is where long-term wealth is built.

Frequently Asked Question

What is the difference between a Smallcase and a mutual fund?

A Smallcase is a basket of stocks held directly in your demat account, curated and rebalanced by a SEBI-registered advisor. A mutual fund pools investor money and issues units; you don't own individual stocks. Smallcase offers direct ownership and real-time transparency. Mutual funds provide greater liquidity, lower entry costs, and a tax-efficient pass-through structure. Each serves a different investor need.

Is investing in direct stocks better than mutual funds in India?

Direct stocks can deliver higher returns for investors with deep research capability and emotional discipline. However, most retail investors lack the tools that portfolio advisory services and leading investment research firms in India deploy. Without this infrastructure, behavioural errors, buying at peaks, and selling in corrections, typically erode direct stock returns versus a consistent mutual fund SIP over 10+ years.

How is a Smallcase taxed compared to a mutual fund?

Smallcase investments are taxed at the individual stock level, each rebalance event involving a sale triggers short-term or long-term capital gains tax. A mutual funds portfolio is taxed only when you sell your units, making it more tax-efficient for long-term, buy-and-hold investors.

Can I lose money in a smallcase?

Yes. A Smallcase consists of actual equity stocks, so it rises and falls with both the market and individual company performance. There are no capital guarantees. Active portfolio management by the Smallcase manager aims to reduce risk through diversification and systematic rebalancing, but market downturns will affect portfolio value.

What is the minimum amount needed to invest in a smallcase?

The minimum investment in a Smallcase depends on the constituent stocks and the specific portfolio. Some start as low as Rs. 2,000–Rs. 5,000, while more diversified or premium Smallcases may require Rs. 25,000–Rs. 1 lakh or more. This is significantly more accessible than portfolio management services, which require a SEBI-mandated minimum of Rs. 50 lakh per investor account.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox