Imagine a company you invest in as a kingdom. Most kingdoms wage wars against others hoping to expand their empires. Some succeed while others get wiped out. Now, visualise a kingdom with a massive moat around it, making it almost impossible to defeat. We just described two types of firms or companies - perfectly competitive firms and monopoly firms.

Perfectly Competitive firms have nothing to protect themselves against other firms in a market with fierce competition, like the bustling bazaars selling vegetables - all the sellers are selling the same goods and are forced to match the prices set by other sellers. In contrast, monopoly firms are like the kingdoms with massive moats - protected from rival firms, allowing them to dominate the market. Imagine a king who controls the only salt mine in his kingdom; he can set whatever price he deems fit and clearly no one else can open up a salt mine without permission of the king.

This fundamental difference underscores the power of monopolies. The unparalleled control and stability over their market lead to significant advantages in profitability and market influence.

What Makes a Monopoly Company?

Ownership of Strategic Raw Materials

The company might own specific materials (such as diamond mines or coal mines) which are essential for manufacturing some specific items.

Exclusive Knowledge/Patent Rights or Licences

The firm may have knowledge about a specific technique of production. The firm may obtain the exclusive right to produce a particular commodity or use a particular production process by getting a patent. The firm may acquire this right by way of licences issued by the government.

Tariff Barriers

A tariff barrier refers to the imposition of import duties by the government on goods or services brought into the country. This trade barrier excludes foreign competitors from the domestic market, allowing indigenous firms to have a shot at monopoly power.

Limited Market Size

At times, the limited size of the market may allow the existence of only one firm of the optimal size. The firm will be capable of producing the products at the lowest average cost as it will enjoy the benefits of economies of scale. Another firm entering would mean that the average cost would increase for each firm and both firms would face losses and have to exit.

Limit Pricing Policy

THe firm may follow a pricing strategy which limits the entry of new firms into the market. The firm because of its low average cost of production can keep its selling price at a low enough level which might not be possible for other firms.

Why are there so Few Monopolies?

Even though monopolies dominate their markets, achieving true monopoly power (100% market share) is almost impossible. Government regulations, potential competition, and advancement in technology and production processes ensure that no single company can have absolute control over an entire market. In the Indian context, there are only 2 complete monopolies - IRCTC and HAL.

IRCTC holds their monopoly thanks to the sheer vastness of the Indian Railways and is the only authorised entity for railway ticketing and catering services; it has been slowly transforming into a one stop shop offering tour packages, ticketing, water and catering.

Hindustan Aeronautics Limited (HAL) is a domestic monopoly owing to its government ownership, preferential treatment by the government and strategic importance.

In 2014, China ended the oldest monopoly with the abolishment of China Salt. It was a state-owned enterprise that had held exclusive rights over salt production, sale, and distribution for centuries.

Are Monopolies Good To Invest In?

Fundamentally, they should be excellent investments. The ‘economic moat’ protects them well enough against outside competition and allows them to charge chronically high prices for their goods and services which leaves room for great profit margins. As a result of which, they generate enough cash flow to distribute consistent dividends.

Exploring Monopolies in India and their Stock Market Returns

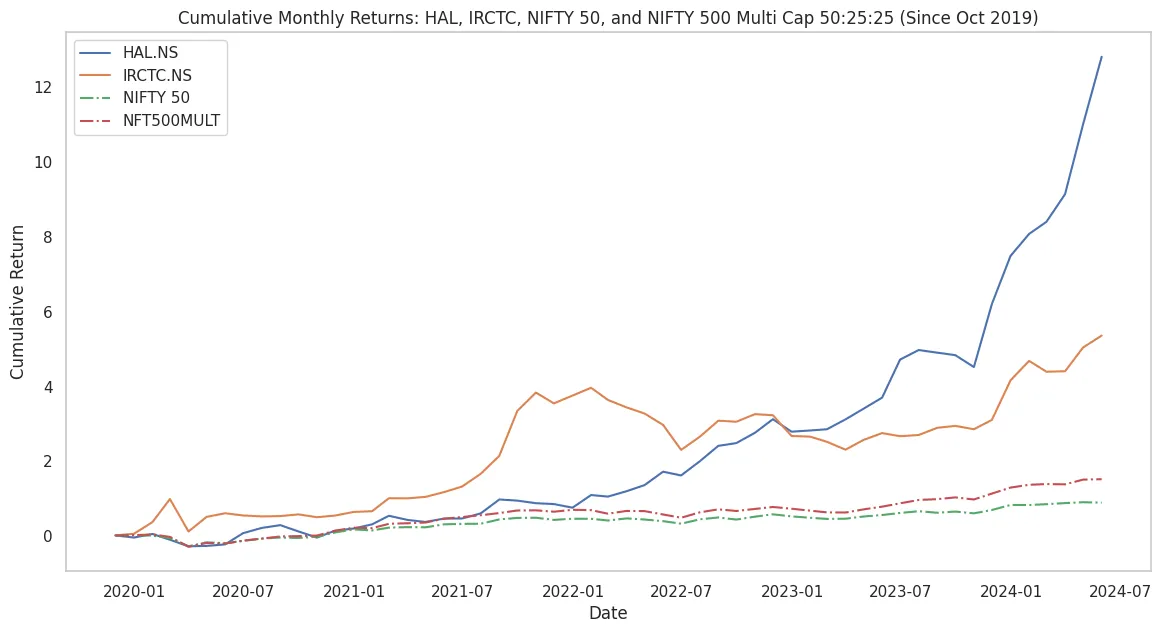

As we discussed beforehand there aren't many perfect monopolies but 2 examples in the Indian context are IRCTC and HAL. IRCTC owns 100% of the railway services and catering in India. HAL (Hindustan Aeronautics Limited) maintains a monopoly over defence aircraft production in India, a status it will hold until 2026 when Airbus is expected to commence the production of defence aircrafts at their new facility in Vadodara.

We looked at the cumulative monthly returns over the past 5 years for both IRCTC and HAL against the NIFTY 50 and the NIFTY 500 Multi Cap 50:25:25 (It assigns fixed weights of 50%, 25%, and 25% to large, mid, and small cap companies, respectively, rebalances quarterly and includes all NIFTY 500 companies, with segment weights varying between rebalances due to price changes).

As expected both monopolies outperformed both the indices over the 5 year time horizon from 2019 to 2024. Both IRCTC & HAL, being government owned monopolies, have also benefited from the Indian government's pro infrastructure, railways, and defence stance. And this is reflected in the high budgetary allocation to these sectors over the last few years.

Market Share of Near Monopolies in India

There are multiple near-monopolies in India that dominate their respective markets. Naturally, many of these companies have diversified businesses beyond just the monopolised segment. Based on online research we identified the following near monopolies -

IEX controls 95% of short-term electricity contracts, making it the leading platform for electricity trading.

MCX has a 92% share of the commodities exchange sector, serving as the primary trading platform for commodities.

Syngene International commands 50% of the contract research and manufacturing services (CRAMS) market, making it a key player in the pharmaceutical and biotechnology industries.

BKT 30% of the off-highway tire Indian market, highlighting its dominance in specialty tires.

DFL is India’s largest airport service aggregator platform.

AIS has a commanding 77% share in the automotive glass market and 50% in the architectural glass market, establishing its dominance in both sectors.

Nestle enjoys a 96.5% share in the Cerelac industry, making it the leader in baby food.

Coal India holds an 82% share in coal production, underscoring its critical role in meeting the country's energy needs.

Hindustan Zinc controls 78% of the zinc industry, making it a dominant player in mining and metals.

ITC leads the cigarette market with a 77% share, ensuring its stronghold in tobacco products.

Marico holds a 73% share in the oil products market, particularly in hair and edible oils.

CAMS has a 70% share in the mutual fund registrar and transfer agent industry, playing a crucial role in financial services.

Pidilite Industries dominates the adhesive market with a 70% share.

CONCOR holds a 68.52% share in the cargo carrier market.

BHEL dominates the power equipment sector with a 67% share.

Praj Industries leads the ethanol plant installation industry with a 60% share.

CDSL controls 59% of the depository business.

APL Apollo has a 50% share in the pre-galvanized and structural tube industry.

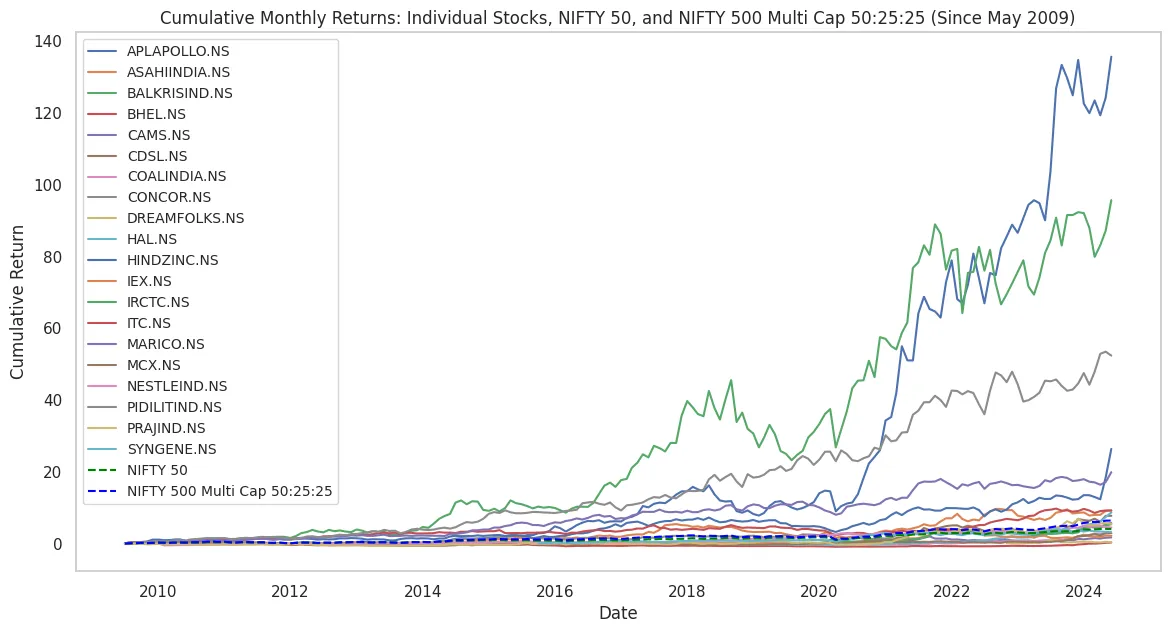

Out of the 20 monopoly stocks and near-monopoly stocks listed, 13 outperformed the NIFTY 50, and 9 outperformed the NIFTY 500 Multi Cap in cumulative monthly returns over a 15-year period. Interestingly, pure monopolies, IRCTC and HAL, were not top performers over the 15 year horizon.

Ticker | Cumulative Return | Ticker | Cumulative Return |

APLAPOLLO | 135.71 | PRAJIND | 5.47 |

BALKRISIND | 95.74 | IRCTC | 5.36 |

PIDILITIND | 52.37 | NESTLEIND | 4.47 |

HINDZINC | 26.36 | NIFTY 50 | 4.05 |

MARICO | 19.87 | SYNGENE | 3.25 |

ITC | 9.20 | COALINDIA | 2.92 |

ASAHIINDIA | 9.19 | MCX | 2.90 |

HAL | 8.63 | IEX | 2.14 |

CDSL | 7.72 | CAMS | 1.70 |

NIFTY 500 MULTI CAP | 6.40 | DREAMFOLKS | 0.39 |

CONCOR | 5.76 | BHEL | 0.27 |

We find no correlation between market share and cumulative returns. For instance, Indian Energy Exchange (IEX) holds over 95% of the market share but has only achieved a cumulative return of about 2.13% since its IPO in October 2017. Similarly, Multi-Commodity Exchange of India (MCX), with a 92% market share, saw a cumulative return of 2.89%. IRCTC, which went public in 2019 with complete market share of Indian Railways and Catering, appreciated by 5.36%. Meanwhile, HAL, which had its IPO in 2018, has appreciated by 8.63%.

However, there are macroeconomic events & market specific factors that we need to be aware of as well. For instance, IRCTC generated 85% in the last 1 year given strong budgetary support. Similarly, HAL has generated 223% in the last 1 year. Both of these companies & their respective stocks have benefitted from the government’s pro infrastructure, defence & railway stance. The question is whether this will continue post the elections in the near future as well.

Analysing Monopoly Stocks: Equal Weighted Basket

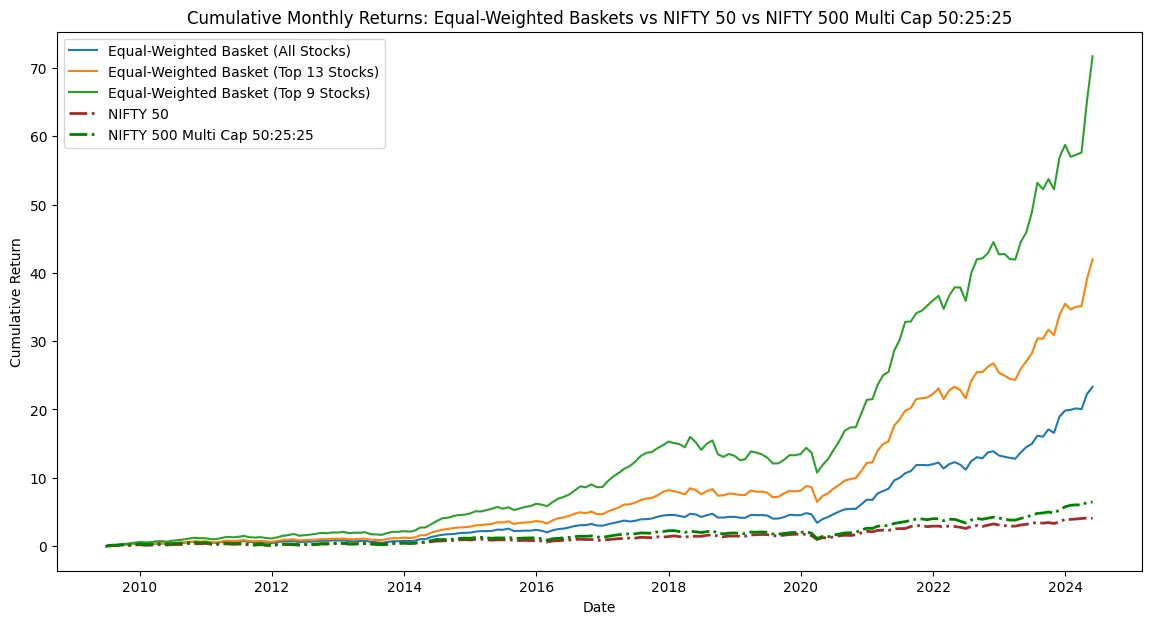

So how would a basket of monopoly stocks with equal weightage perform against the NIFTY 50 over the same 15 year period?

Here we compare 3 baskets to the NIFTY 50 and NIFTY 500 Multi Cap.

The first basket is an equally weighted basket of the 20 monopoly and near monopoly stocks we listed out above.

The second basket is an equally weighted basket of the 13 stocks within the 20 monopoly stocks that have outperformed the NIFTY 50 over the past 15 years.

The third basket is the set of 9 stocks out of the initial 20 which outperformed the NIFTY 500 Multi Cap.

Stocks were added to the baskets as their IPOs were released, maintaining an equal weightage throughout.

₹1,000 invested on the 20th of May, 2009, in the NIFTY 50 would have grown to ₹4,049 on the 20th of May, 2024 and ₹6,396 in the Nifty 500 Multicap. In the equal-weighted basket of 20 monopoly stocks, this would have grown to ₹23,316, ₹41,990 for the 13 monopoly stock basket, and ₹71,741 for the 9 monopoly stock basket. Simply put, during the 15-year period NIFTY 50’s CAGR was 9.66% & NIFTY 500 Multi Cap’s CAGR was 10.69%. While, the 20 monopoly stock basket gave 20.92% CAGR, the top 13 monopoly stocks basket gave 25.84% CAGR and the top 9 monopoly stocks basket gave an impressive 27.82% CAGR.

This suggests that companies with dominant market positions can generate higher returns due to their ability to leverage market power, achieve economies of scale, and sustain profitability over long periods.

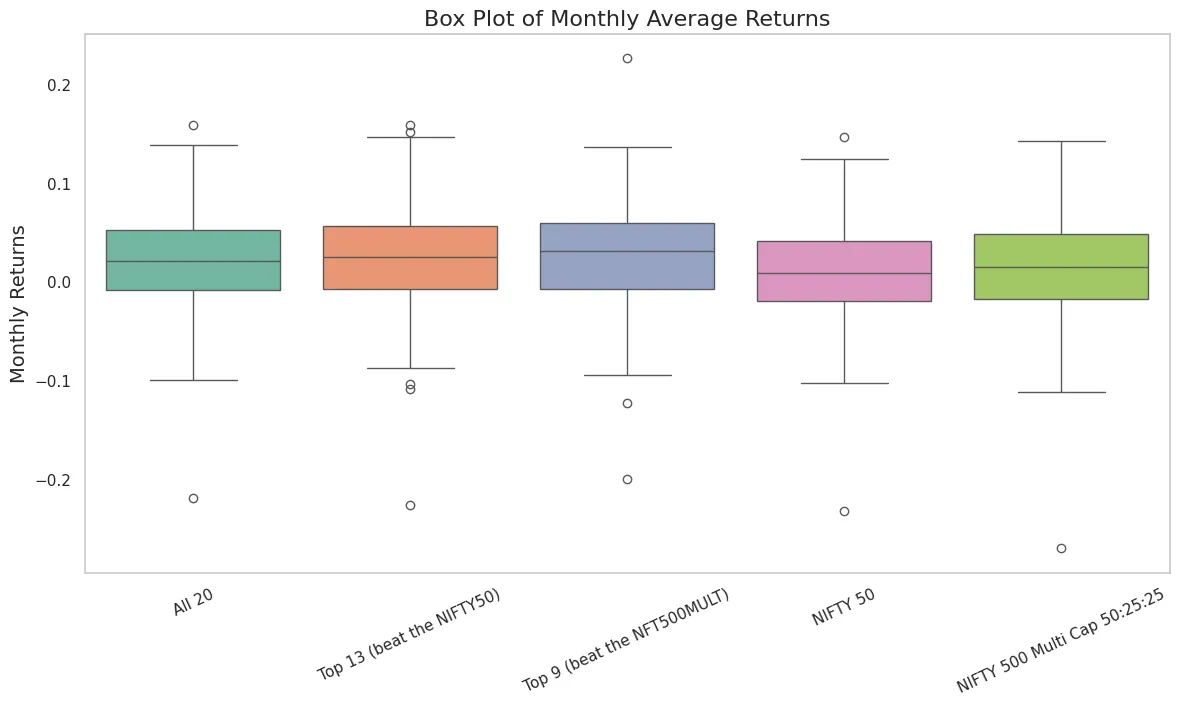

Variation Of Monthly Returns For Monopoly Stocks

We take a look at the variation of monthly returns of the NIFTY 50 and the NIFTY 500 Multi Cap and compare it to the average monthly returns of the basket of the 20 monopoly stocks, 13 monopoly stocks that beat the NIFTY 50 and 9 stocks that beat the NIFTY 500 Multi Cap.

Unsurprisingly, when we plot the average monthly returns over 15 years, we see that the monopoly baskets do better than the NIFTY 50 and the Nifty 500 Multi Cap both of which gave median average monthly returns of 0.86% & 1.47%, respectively. In comparison, all 20 basket’s median average monthly return was 2.05%, 2.53% for the top 13 basket and 3.07% for the top 9 basket.

Are These Returns Due To Random Luck or Chance?

We look at the mean monthly returns of the NIFTY 50 and the NIFTY 500 Multi Cap and compare it against the 3 equal weighted baskets of 20, 13 and 9 monopoly stocks basket. Analyzing data with and without outliers helps ensure accurate results by revealing the impact of extreme values and ensuring robustness and reliability of findings.

Performance of Monopoly Stock Baskets vs. NIFTY 50

Inclusive of Outliers

With outliers included, the 20-stock basket's outperformance over the NIFTY 50 is not statistically significant which means the observed performance difference could be due to random chance. While the 13 and 9 stock baskets show statistically significant higher returns, which means the higher returns are not due to random chance.

Exclusive of Outliers

Excluding outliers, the 20-stock basket's results are close to being statistically significant which means there is a tendency for higher returns but not enough evidence to confirm it definitively. While the 13 and 9 stock baskets continue to show statistically significant higher returns compared to the NIFTY 50, i.e. it is not random chance.

Performance of Monopoly Stock Baskets vs. NIFTY 500 Multi Cap

Inclusive of Outliers

With outliers included, the 20-stock basket's outperformance over the NIFTY 500 Multi Cap is not statistically significant, suggesting the observed performance difference could be due to random chance.

The top 13 stock basket's higher returns are close to being statistically significant, indicating a tendency for higher returns but not enough evidence to confirm it definitively.

In contrast, the top 9 stock basket shows statistically significant higher returns, meaning the performance difference is unlikely to be due to random chance.

Exclusive of Outliers

Excluding outliers, the 20-stock basket's results are close to being statistically significant, suggesting a tendency for higher returns but not enough evidence to confirm it definitively. While the 13 and 9 stock baskets show statistically significant higher returns, further confirming the performance difference is unlikely to be due to random chance.

Conclusion: Power of Monopolies

Investing in monopoly and near-monopoly stocks presents a compelling opportunity due to their significant market advantages and inherent stability. These companies often enjoy high-profit margins and stable cash flows, thanks to substantial barriers to entry.

Our analysis highlights the substantial potential of investing in monopoly and near-monopoly stocks. Despite the inherent challenges in achieving true monopoly status, companies with dominant market positions have consistently demonstrated the ability to deliver superior returns compared to broad market indices like the NIFTY 50 and NIFTY 500 Multi Cap. The 13 stock basket demonstrates statistically significant higher returns, even after removing outliers and the 9 stock basket exhibited the highest returns of the three equal-weighted baskets. Therefore, investing in these dominant companies, while considering the associated risks and the importance of diversification, can be a rewarding long-term strategy. Another important finding was that there is no correlation between market share and cumulative returns, indicating that factors beyond market dominance play a crucial role in determining returns.

Buffett loves monopolies and hates competition. Buffett has said at his investment meetings that, “The nature of capitalism is that if you’ve got a good business, someone is always wanting to take it away from you and improve on it.” And in his annual reports, he has approvingly quoted Peter Lynch, “Competition may prove hazardous to human wealth.” And how true that is. What is good for the monopolist is not good for capitalism. Buffett and his business partner Charlie Munger always tried to buy companies that have monopoly-like status. Once, when asked at an annual meeting what his ideal business was, he argued it was one that had “High pricing power, a monopoly.” The message is clear: if you’re investing in a business with competition, you’re doing it wrong. – The Myth of Capitalism by Jonathan Tepper, Denise Hearn

This underscores the advantages of monopolistic market power, economies of scale, and sustained profitability. However, while these findings are promising, investors should remain cognizant of market dynamics and regulatory factors that may impact the future performance of these stocks.

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox