You have built a serious corpus, maybe ₹50 lakh or more, and the FD-and-index-fund routine no longer feels like enough. You want better returns, but you are caught between two paths: hand it to a professional through portfolio management services, or take charge yourself with active investing. Both promise to beat the market. Both carry real costs and real risks. So which one genuinely builds wealth for someone like you? This guide breaks down the trade-offs in plain language, covers PMS charges, risk, and control, and helps you decide with confidence. Wright Research builds quant-led portfolios for exactly this decision.

What Is the Difference Between PMS and Active Investing?

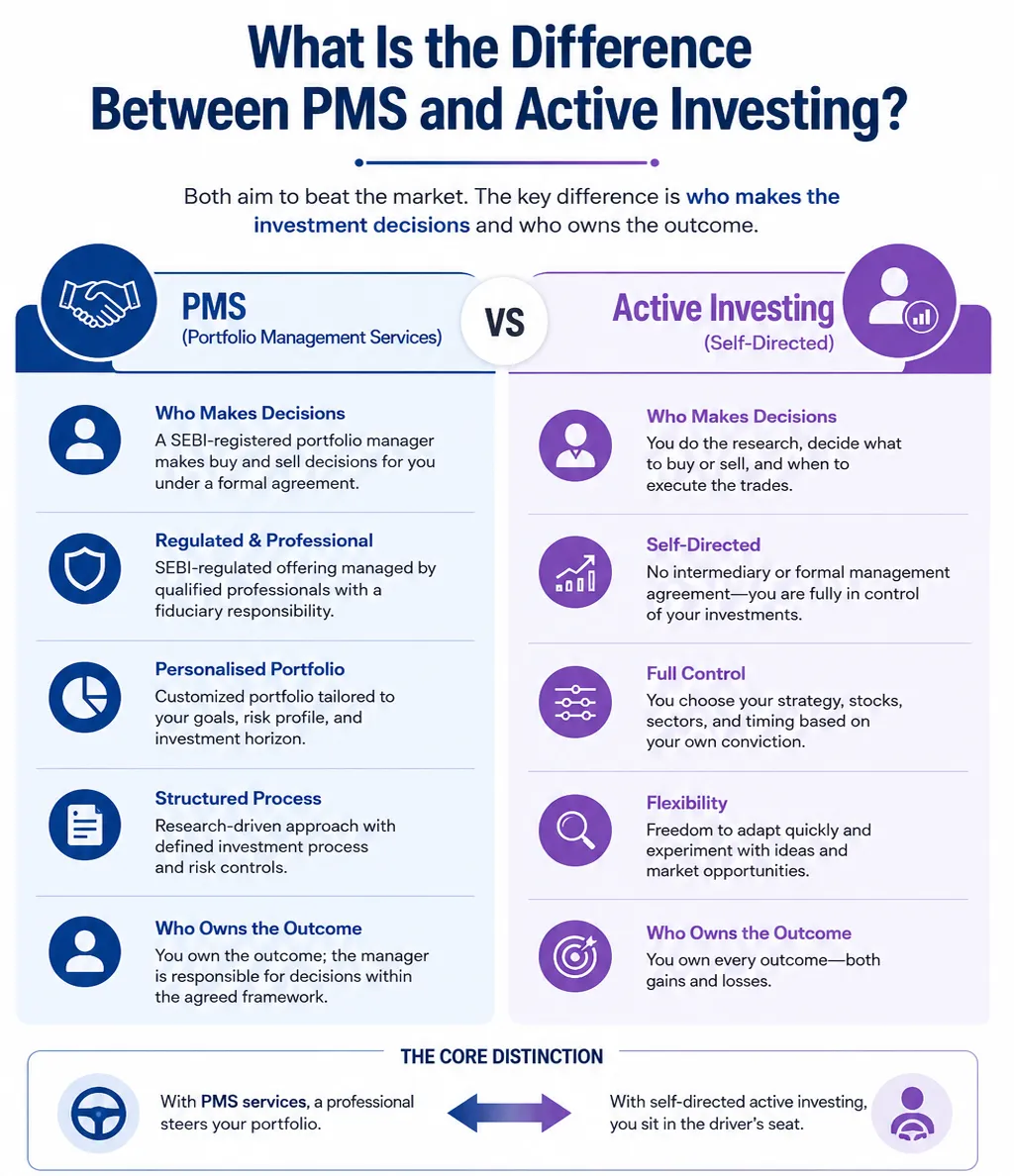

Portfolio management services are a SEBI-regulated, professionally managed offering where an expert builds and runs a personalised portfolio of securities held directly in your own demat account. Active investing is any strategy, run by you or a manager, that tries to beat a benchmark through deliberate stock selection and timing rather than simply tracking an index.

The core distinction is who holds the steering wheel. With PMS services, a registered portfolio manager makes the buy and sell decisions for you under a formal agreement. With self-directed active investing, you do the research, place the trades, and own every outcome.

Both sit on the same side of the active-versus-passive debate. Neither is content to merely match the Nifty. The real question is not active versus passive; it is whether professional active portfolio management through a structured PMS portfolio, delivered by registered PMS services, serves you better than running your own active book. That depends on your capital, time, temperament, and how you handle portfolio risk management under pressure.

How Do Portfolio Management Services Work?

A good PMS follows a disciplined, research-led cycle rather than ad hoc stock picking. Understanding this cycle shows why portfolio management services appeal to investors who want rigour without doing the work themselves.

It starts with profiling. The manager assesses your goals, risk appetite, liquidity needs, and time horizon, then frames an investment policy. Next comes construction: the portfolio manager selects securities and builds your PMS portfolio, which is held directly in your name. As your PMS buys Infosys, you own Infosys shares directly, not units of a pooled fund.

From there, it becomes ongoing active portfolio management: continuous monitoring, periodic rebalancing, and transparent reporting. You receive regular statements showing exactly what you hold and why.

PMS in India comes in three forms. Discretionary PMS lets the manager act without per-trade approval. Non-discretionary PMS needs your sign-off on each decision. Advisory or portfolio advisory services provide recommendations while you execute. This structure is what separates professional PMS services from informal advice, and it is backed by SEBI registration and a fiduciary duty to act in your interest.

How Does Active Investing Work?

Self-directed investing means you become the portfolio manager. You research companies, form a view, decide position sizes, execute trades, and review performance. The appeal is total control and no management fee. The challenge is that everything, including discipline, now rests on you.

Serious active investing is not random tip-following. It demands a repeatable process: screening for quality and value, sizing positions sensibly, and conducting honest portfolio analysis and management so you know what is working and what is dragging you down. Without that structure, most DIY portfolios drift into concentrated bets and emotional decisions.

The hidden cost is time and behaviour. Markets test conviction constantly, and the biggest enemy of returns is often the investor reacting to fear or greed. This is where many self-directed investors quietly underperform a disciplined PMS portfolio, not because they lack intelligence, but because consistent portfolio risk management is hard to sustain alone across years of volatility.

PMS vs Active Investing: The Honest Comparison

Neither path is universally better. The right choice depends on your situation. The table below lays out the trade-offs side by side so you can see where each one wins.

Parameter | Portfolio Management Services | Self-Directed Active Investing |

Who decides | SEBI-registered portfolio manager | You |

Minimum capital | ₹50 lakh (SEBI rule) | Any amount |

Ownership | Direct securities in your demat | Direct securities in your demat |

Time required | Low, the manager runs it | High, ongoing research |

Cost | Management and/or performance fees | Brokerage and your time |

Risk control | Professional, rules-based | Self-managed, varies |

Customisation | High, tailored to your goals | Total, but self-driven |

Best suited for | HNIs wanting expertise | Hands-on, experienced investors |

The honest takeaway is this. If you have the capital, portfolio management services buy you professional active portfolio management, structure, and time back. If you have the skill and discipline, self-directed active investing saves you fees but demands real effort. Strong portfolio analysis and management are non-negotiable in both.

Understanding PMS Charges and What You Actually Pay

Cost is where many investors get caught off guard, so let us be direct about PMS's charges. PMS fees are higher than mutual funds, and that is widely accepted because you get direct ownership and a personalised portfolio. The value holds only when net-of-fee returns beat the alternatives.

There are three common fee models. A fixed-only model charges a flat annual management fee, typically around 1% to 2.5% of assets. A performance-only model charges nothing fixed but takes a share of profits above a hurdle. A hybrid model, the most common in India, blends a modest fixed fee with a performance share.

Performance fees usually run 10% to 20% of returns above a hurdle rate such as 8%, 10%, or a benchmark like the BSE 500. Crucially, two safeguards protect you. The hurdle rate means you pay performance fees only on returns above a set threshold. The high-water mark means you never pay twice for recovering the same losses.

Always read the fine print on PMS charges, since GST, brokerage, custody costs, and exit loads can add up. Transparent PMS services spell out every charge clearly in the client agreement. For reference, Wright Research publishes its fee options openly, including a flat-fee plan and a performance-fee plan over a 10% hurdle with the high-water mark applied.

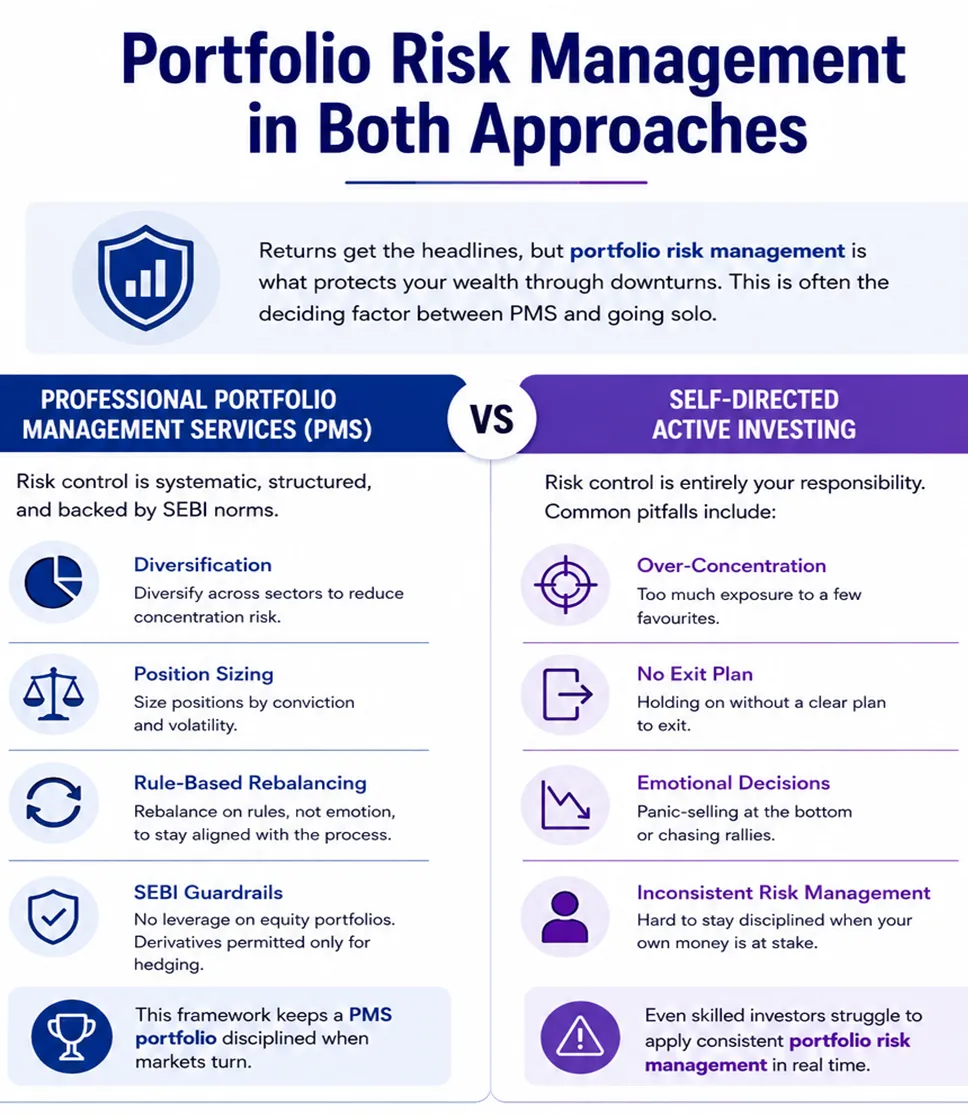

Portfolio Risk Management in Both Approaches

Returns get the headlines, but portfolio risk management is what protects your wealth through downturns. This is often the deciding factor between PMS and going solo.

In professional portfolio management services, risk control is systematic. Managers diversify across sectors, size positions by conviction and volatility, and rebalance on rules rather than emotion. SEBI norms add guardrails too: no leverage on equity portfolios, with derivatives permitted only for hedging. This framework keeps a PMS portfolio disciplined when markets turn.

In self-directed active investing, risk control is entirely your responsibility. The most common failures are over-concentration in a few favourites, no exit plan, and panic-selling at the bottom. Even skilled investors struggle to apply consistent portfolio risk management when their own money is swinging in real time.

This is the quiet edge of structured active portfolio management. A rules-based process removes the human bias that wrecks returns. Wright Research uses quant models that score stocks on momentum, quality, value, and low volatility, then rebalances systematically, turning portfolio analysis and management into a repeatable discipline rather than a gut call.

Who Should Choose PMS vs Self-Directed Active Investing?

The right path comes down to capital, time, and temperament. These short profiles should help you place yourself.

The HNI who wants expertise. You have ₹50 lakh or more and would rather have a professional run a customised PMS portfolio while you focus on your career or business. Portfolio management services with strong portfolio advisory services are built for you, whether you want full discretion or portfolio advisory services that leave the final call with you.

The time-poor professional. You earn well but cannot track markets daily. You want active investing outcomes without the daily grind. Discretionary PMS services hand the work to an expert while you stay informed through clear reporting.

The hands-on DIY investor. You enjoy research, have the time, and apply disciplined portfolio analysis and management yourself. Self-directed active investing may suit you, provided your portfolio risk management is genuinely consistent.

The cost-sensitive builder. If you are still building toward the ₹50 lakh threshold, disciplined self-directed investing or research-backed funds make sense now, with PMS as a future step once your corpus and PMS charges justify it.

How Wright Research Delivers Better Returns Through PMS Services

Better returns are not about chasing the hottest stock; they come from process, discipline, and risk control compounding over years. That philosophy sits at the heart of how Wright Research runs portfolio management services.

Start by being honest about your situation. Review your capital, your available time, and how you behave when markets fall. If a professional, quant-driven PMS portfolio fits, Wright Research builds and manages it with transparent active portfolio management and clear reporting at every step.

Lean on rules over emotion. Wright Research's factor models handle the portfolio analysis and management systematically, while disciplined portfolio risk management aims to soften drawdowns rather than chase every rally. You also get straightforward portfolio advisory services and fully disclosed PMS charges, so there are no surprises. Whether you prefer fully managed PMS services or guided portfolio advisory services, the process stays transparent.

Ready to explore a data-led path to better returns? Speak with a Wright Research advisor or explore our PMS strategies today.

Frequently Asked Questions

What is the difference between PMS and active investing?

Portfolio management services are a SEBI-regulated, professionally managed portfolio held in your own demat account, run by a registered manager. Active investing is any strategy, by you or a manager, that aims to beat a benchmark. PMS is essentially professional active portfolio management done for you.

What is the minimum investment for portfolio management services in India?

SEBI mandates a minimum of ₹50 lakh per investor for PMS services as of 2026. Some firms set higher thresholds. This rule keeps portfolio management services suited to investors who can absorb market volatility and meet the typical PMS charges that come with personalised management.

How are PMS charges structured?

PMS charges usually follow three models: fixed-only, performance-only, or hybrid. Fixed fees run roughly 1% to 2.5% of assets; performance fees are 10% to 20% of returns above a hurdle rate, protected by a high-water mark. Always confirm GST, brokerage, and exit loads in your agreement.

Is PMS better than self-directed active investing?

It depends on you. Portfolio management services offer professional portfolio risk management, structure, and saved time, suiting HNIs. Self-directed active investing saves fees but demands serious effort and discipline. Both rely on consistent portfolio analysis and management; the better choice matches your capital, time, and temperament.

How does portfolio risk management differ between the two?

In PMS services, risk control is systematic: rules-based diversification, position sizing, and SEBI guardrails like no equity leverage. In self-directed active investing, risk control rests entirely on you, where over-concentration and panic-selling are common pitfalls. Structured portfolio risk management is the quiet edge of professional management.

What are portfolio advisory services?

Portfolio advisory services are a form of PMS where the manager recommends investments while you execute the trades and retain control. It suits investors who want expert portfolio analysis and management but prefer the final say on their PMS portfolio, rather than fully discretionary management.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox