The closure of the Strait of Hormuz in late February 2026, triggered by the US-Israeli air war against Iran, has plunged India into its most severe energy crisis in decades. The International Energy Agency has called this the largest supply disruption in the history of the global oil market, with roughly 20% of the world's seaborne oil trade and 20% of global LNG exports blocked. For India, the world's third-largest oil importer and a country that depends on imports for 88% of its crude oil, the consequences have been immediate, widespread, and deeply damaging.

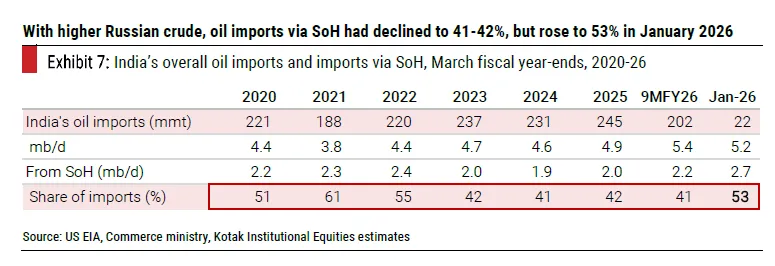

India's energy supply chain runs directly through the Strait of Hormuz. The Strait of Hormuz accounted for approximately 41% of India's crude oil imports, 55% of its LNG imports, and 88% of its LPG imports during the first nine months of FY2026.

In January 2026, the share of crude imports via the Strait rose sharply to 53%, up from 41-42% in prior years, as Indian refiners increased purchases from Gulf producers.

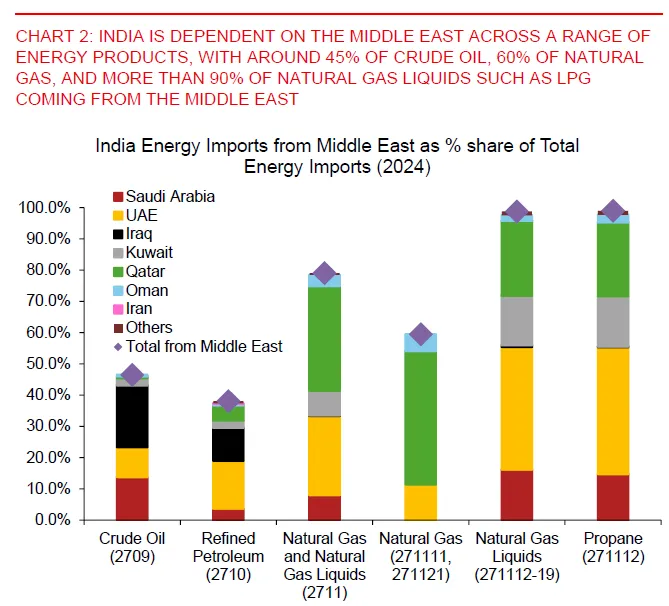

The dependency extends across fuel types such as crude oil, refined petroleum, natural gas, propane and others. Saudi Arabia, Iraq, the UAE, and Kuwait together supply more than half of India's crude oil, translating to roughly 2.5 to 2.8 million barrels per day.

Qatar and the UAE account for over half of India's LNG imports. Most critically, approximately 90% of India's LPG imports transit the Strait. Since India imports about 60% of its total LPG consumption, this means that roughly 54% of all LPG used in Indian households for cooking passes through this single chokepoint.

India's strategic petroleum reserves cover only about 9.5 days of consumption. The government has stated that combined crude oil and refined product inventories provide approximately 50 days of cover, but signs of stress have already appeared, particularly in LPG, where import dependence is most acute.

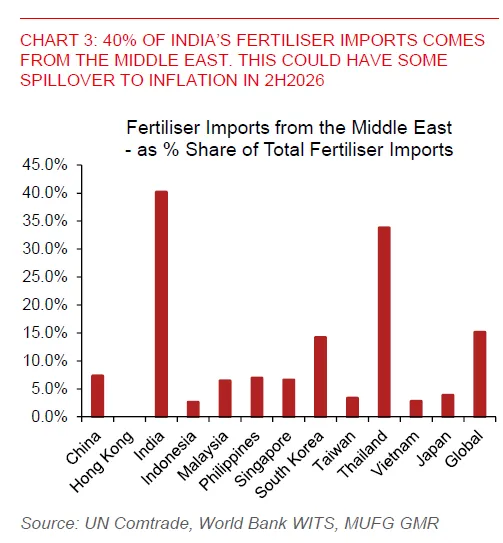

Beyond oil, India is also dependent on the middle east for its fertilizers. 40% of India’s fertiliser imports come from the middle east . Farmers in key agricultural states are already panicking and stockpiling fertilisers, fearing reduced crop yields and financial losses.

This is especially worrying because the Kharif season (monsoon planting season) is crucial for crops like rice, pulses, and oilseeds, which depend on timely monsoon rains and adequate fertiliser use. Any shortage or delay can directly reduce yields and farmers’ incomes. Experts warn that if fertiliser supply does not stabilise quickly, it could impact overall food production in India, potentially driving up food prices and affecting food security for millions.

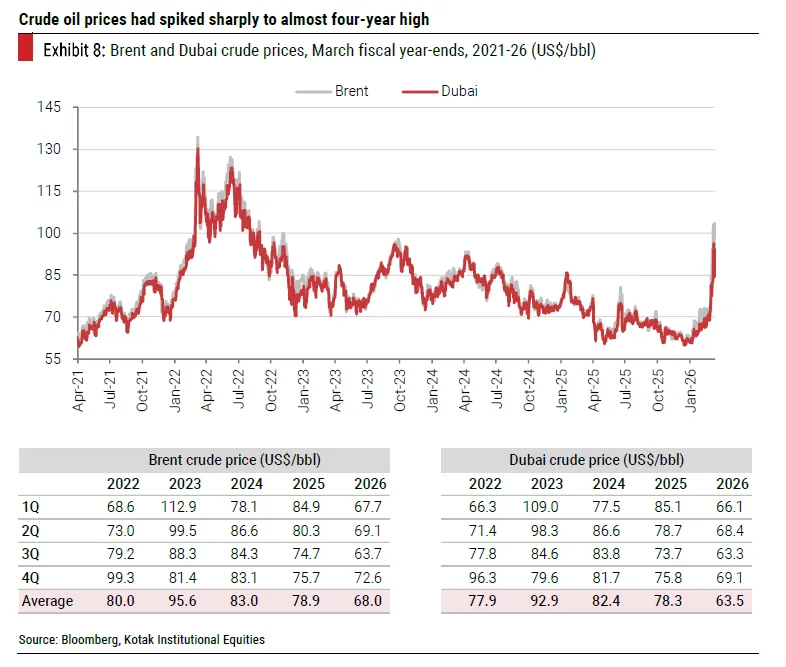

Crude oil prices surged from around $69 per barrel in February 2026 to $113 per barrel in March. Brent crude briefly crossed $100 per barrel, reaching levels not seen in nearly four years. Analysts are raising their FY2027 oil price assumption to $85 per barrel from $65, and long-term estimate to $75 per barrel from $70.

The price impact on India's economy is significant.

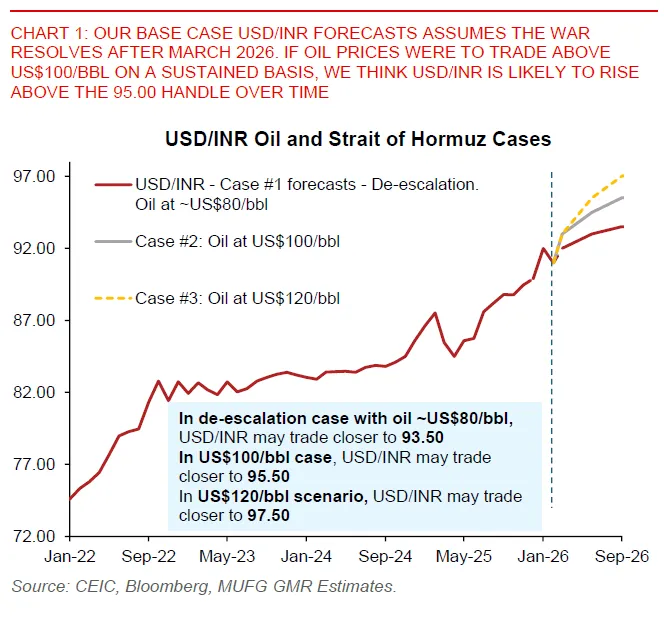

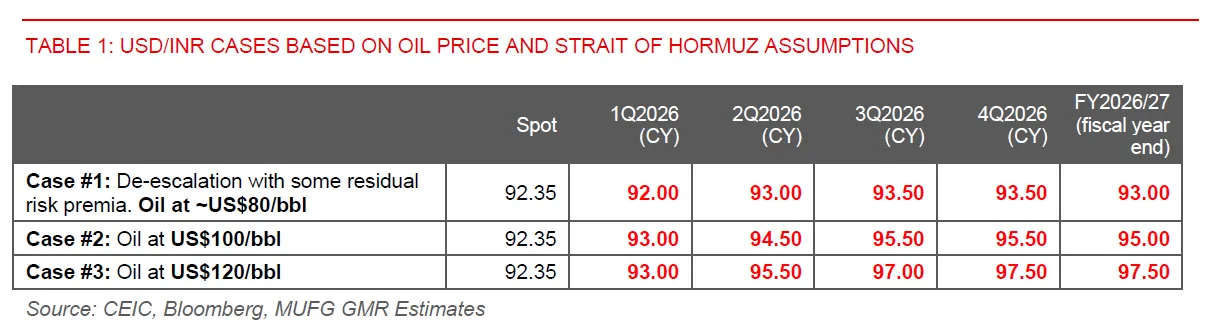

Case 1 (de-escalation), oil prices stabilize around US$80/bbl, with only residual risk premia. This scenario assumes limited disruption to energy supplies and a gradual normalization of conditions. The impact on India’s GDP is relatively mild, with growth remaining close to the baseline forecast of around 7%, as lower energy costs help contain inflation and support consumption and investment.

Case 2 (moderate escalation), oil prices rise to around US$100/bbl, reflecting sustained geopolitical tensions. Here, higher import costs and widening current account deficits begin to weigh on the economy, pushing GDP growth below 6.5%, alongside rising inflation and weaker currency dynamics.

In Case 3 (severe disruption), oil prices surge to US$120/bbl with potential energy shortages, making this scenario structurally different from typical oil shocks. Beyond direct price effects, disruptions in LPG and natural gas supplies, on which India is heavily dependent, create spillovers across sectors such as manufacturing, fertilizers, food production, and transportation. This leads to a stagflationary environment characterized by sharply higher inflation and significantly weaker growth.

MUFG Research estimates that every $10 per barrel increase in oil prices widens India's current account deficit by 0.4-0.5% of GDP and reduces GDP growth by 0.1-0.2 percentage points. But in extreme scenarios, the impact could be larger due to supply-side constraints and indirect effects.

At $100 per barrel, the current account deficit would move toward 3% of GDP, compared with a baseline forecast of around 1.5%. As a result, GDP growth could fall well below baseline levels, reflecting both demand compression and supply disruptions across the economy

LPG has been the first and most visible casualty of the crisis. With 33 crore (330 million) LPG connections across the country, cooking gas is a daily necessity for hundreds of millions of Indian households. The disruption in Hormuz transit has led to booking gaps of up to 45 days, cylinder shortages in multiple cities, and black-market prices reportedly reaching Rs 4,000 to Rs 5,000 per cylinder.

The government has responded with emergency measures. Under the Essential Commodities Act, the Ministry of Petroleum and Natural Gas ordered households with piped natural gas (PNG) connections to surrender their LPG cylinders within 90 days. Oil marketing companies have been directed to digitally map addresses and block LPG bookings for households where piped gas is available.

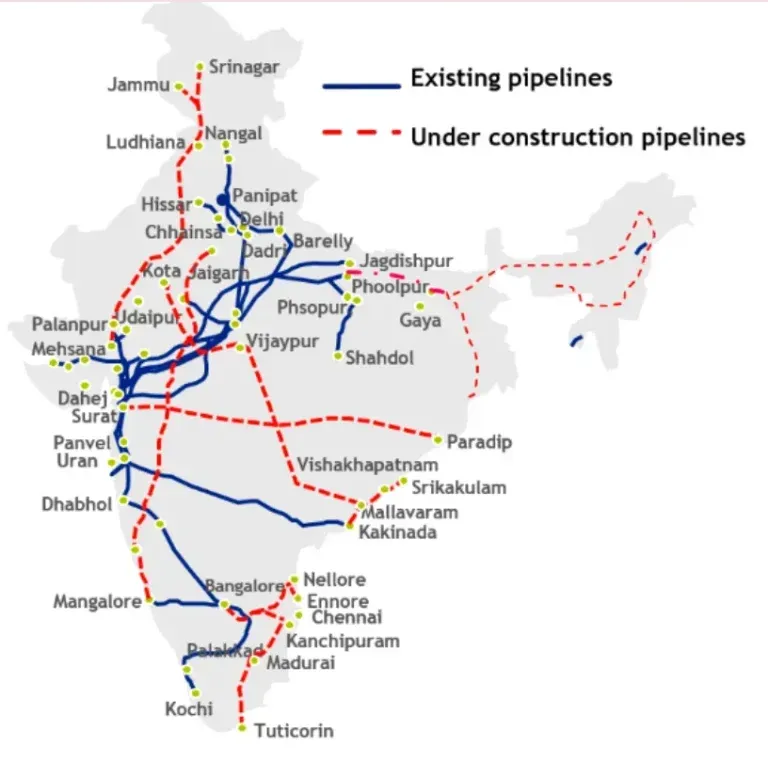

In March 2026, India installed piped gas connections to 580,000 new households, a sharp acceleration from the usual pace. The rationale is clear: PNG is primarily sourced from domestic gas fields, making its supply chain independent of the Hormuz chokepoint. India produces roughly half the natural gas its PNG network consumes, compared to relying on Gulf imports for most of its LPG. However, the gap remains enormous. India has only 1.6 crore piped gas connections against 33 crore LPG connections. Bridging this gap in months rather than decades is the government's stated ambition, but the infrastructure buildout required is massive.

Many Indian households have resorted to kerosene, coal, and wood as stopgap cooking fuels, reversing years of progress under the Ujjwala scheme that had brought clean cooking fuel to rural India.

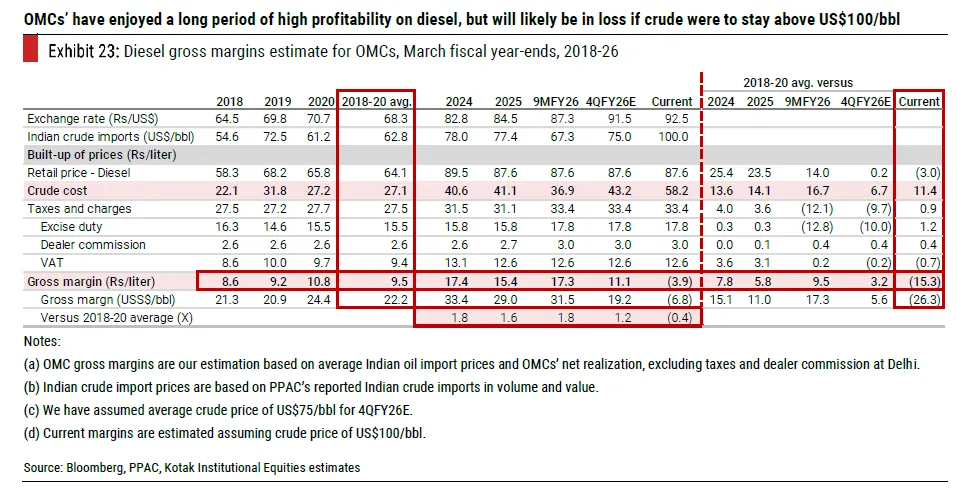

India's three public sector oil marketing companies, Indian Oil Corporation (IOCL), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL), are bearing the financial brunt of the crisis. With retail petrol and diesel prices frozen by the government, OMCs cannot pass through the higher crude costs to consumers.

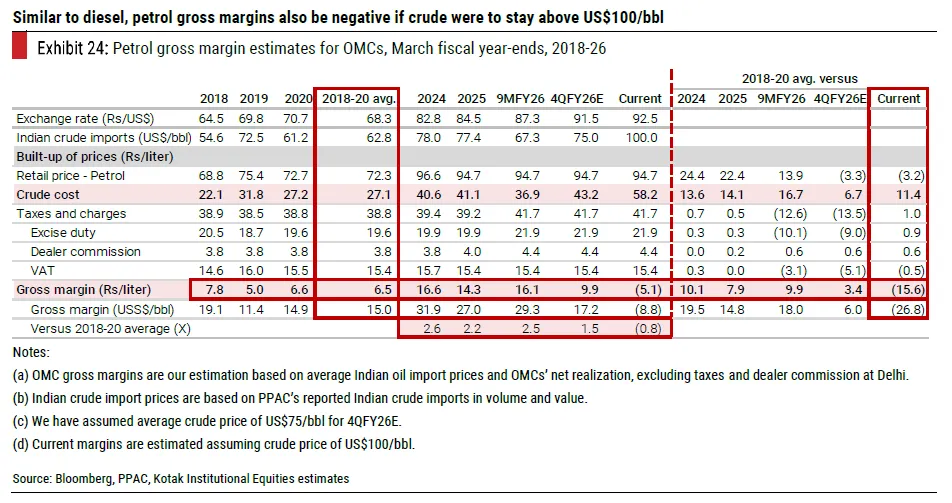

Kotak estimates that at $100 per barrel crude, diesel gross margins for OMCs turn negative at Rs 3.9 per liter, and petrol margins at Rs 5.1 per liter. The brokerage has cut FY2027 EBITDA estimates by 45-47% for BPCL and HPCL, and 28% for IOCL.

Paradoxically, the elevated refining cracks (the spread between crude and product prices) that normally benefit refiners are harmful to OMCs in this environment. Higher cracks mean higher refinery transfer prices, but frozen retail prices mean OMCs absorb the entire difference. Emergency LPG imports at spot prices are expensive, and government compensation is historically delayed and partial.

OMCs had benefited from elevated marketing margins during the previous low-oil-price period (FY2024-FY2026), building up balance sheet cushions. IOCL's 9-month FY2026 EBITDA was higher than all prior years except FY2024. BPCL's net debt-to-equity ratio had fallen to 0.06. These buffers are now at risk of being eroded rapidly.

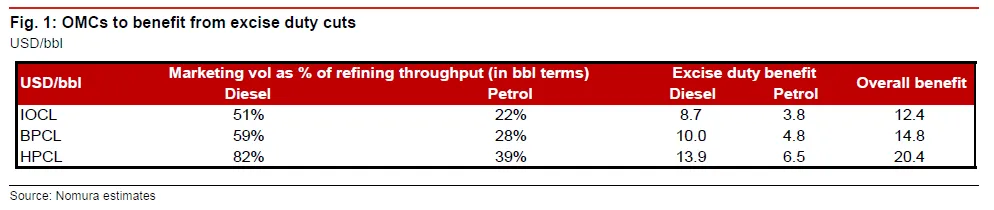

On March 27, 2026, the government announced two significant measures. First, it cut excise duty on petrol and diesel by Rs 10 per liter, providing direct margin relief to OMCs. Nomura estimates the excise duty cut benefits IOCL by $12.4 per barrel, BPCL by $14.8 per barrel, and HPCL by $20.4 per barrel on an integrated basis.

Second, the government imposed a windfall tax (Special Additional Excise Duty) of Rs 21.5 per liter on diesel exports and Rs 29.5 per liter on ATF exports. This measure is designed to disincentivize refined product exports and keep fuel available domestically. Nomura expects domestic standalone refineries to sell diesel and ATF to OMCs at export-parity prices adjusted for the windfall tax, effectively lowering procurement costs for OMCs. HPCL benefits the most, as roughly 40% of its diesel retail sales are sourced from standalone refineries.

The fiscal cost to the government is substantial. With approximately 165 billion liters of annual retail petrol and diesel sales, the excise duty cut implies a revenue loss of approximately Rs 1.65 trillion, or about 0.45% of GDP.

India has moved quickly to diversify its crude sources away from the Gulf. The government has stated that Indian refiners now secure crude from more than 40 countries. Most notably, India has resumed purchases of Iranian crude oil for the first time since 2019, following a US waiver. A vessel carrying 44,000 metric tons of Iranian LPG was received at Mundra Port in mid-March.

Russian crude, which had already become a significant part of India's import mix following the 2022 Ukraine war, has gained further share. Indian refiners have also increased purchases from West Africa and Latin America. However, diversification has limits. The butane-heavy LPG blend used in most Indian households is produced almost exclusively in the Gulf, making supplier substitution for cooking gas particularly difficult.

India has chosen to negotiate bilaterally with Iran for safe passage through the Strait rather than joining the US-led naval coalition. The Indian Navy launched Operation Urja Suraksha in late March, deploying over five warships to escort Indian-flagged cargo ships in the region. As of March 2026, 28 Indian-flagged vessels were operating in the Persian Gulf area with 778 Indian seafarers onboard.

The crisis has created a strong price signal favoring clean energy alternatives. Electric car registrations in India jumped 50% year-on-year in March 2026, with part of the increase attributed to the relative cost advantage of EVs as petrol prices remain elevated.

The broader energy transition picture is complex. India's relationship with LNG as a transitional fuel was already limited, since imported LNG was never cheap enough to compete with domestic coal and renewables in the power sector. The Hormuz disruption has further undermined the case for LNG as a bridge fuel, reinforcing India's trajectory of a more direct transition from coal to renewables.

The crisis has also accelerated India's interest in coal gasification, where domestic coal is converted into gas, reducing import dependence. Meanwhile, the push to convert households from LPG cylinders to piped natural gas represents another facet of the energy security response, though it addresses fuel source diversification rather than a shift to clean energy per se.

The IEA has described this as the greatest global energy security challenge in history. For India, the crisis underscores a vulnerability that decades of economic planning did not adequately address. Whether it catalyzes a structural transformation comparable to the 1991 liberalization, triggered partly by the Gulf War's impact on oil prices, depends on how long the Strait remains closed and how aggressively India acts on long-term energy security.

The Reserve Bank of India held interest rates steady at its April 2026 meeting as the war upended the economic outlook. The central bank faces a difficult trade-off: higher oil prices create inflationary pressure, but the growth slowdown from the energy shock argues against tightening.

The Dallas Federal Reserve estimates that a one-quarter closure of the Strait would raise WTI oil prices to $98 per barrel and reduce global GDP growth by an annualized 2.9 percentage points in Q2 2026. If the disruption persists for three quarters, oil prices could reach $132 per barrel, with significantly larger growth impacts.

For India specifically, the crisis threatens multiple channels simultaneously: a wider current account deficit, a weaker rupee, higher inflation (particularly in food, given fertilizer supply disruptions), reduced consumer spending as fuel costs rise, and fiscal pressure from subsidies and excise duty cuts. The ceasefire announced on April 8 offers some hope, but the Strait remains effectively closed, with Iran limiting the number of ships that can cross. A return to normal oil trade could take at least three months, according to industry executives, due to slow vessel movement, limited ship and insurance availability, loading constraints, and production shut-ins at major Gulf fields.

India's energy crisis is far from over. The near-term focus remains on managing supply shortfalls, securing alternative sources, and protecting the most vulnerable households from cooking fuel shortages. The longer-term imperative, reducing structural dependence on a single maritime chokepoint for the country's energy lifeline, has never been clearer.

Kotak Institutional Equities, "Oil, Gas & Consumable Fuels: Party is over; now it's time to pay back," March 17, 2026

Nomura, "India Oil & Gas: Excise duty cut and windfall tax to benefit OMCs," March 30, 2026

Financial Times, "Energy crisis offers boon for Chinese exporters," 2026

Economic Times, "India Presses Iran to Expedite Movement of Oil & Gas Cargoes," 2026

MUFG, “India - Strait of Hormuz closure: Not just about oil prices for INR”, 2026

Chief Marketing & Growth Officer | Wright Research

Learn more about our Chief Marketing Officer, Siddharth Singh Bhaisora. Siddharth is a highly experienced investment advisor.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart