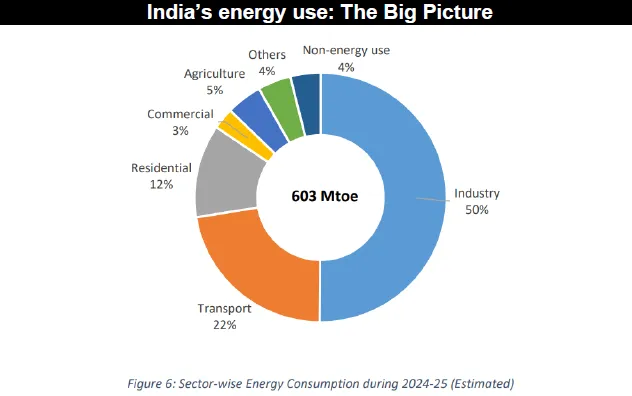

India consumes 603 million tonnes of oil equivalent of primary energy annually, making it the world’s third-largest energy consumer. Industry accounts for 50% of this consumption, transport for 22%, and residential use for 12%. Coal dominates the energy mix at 55–60%, followed by oil at 30%, natural gas at 6–7%, and a rapidly growing renewables segment.

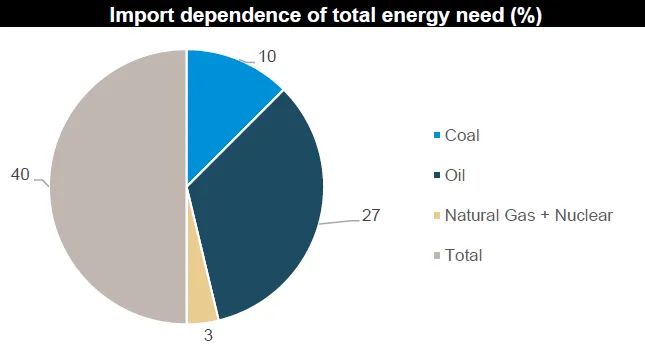

The country’s total energy import dependence stands at 40%, with crude oil imports alone at approximately 88–89%, natural gas at around 50%, and coal at 23%. This structural reliance on imported fuels leaves the economy exposed to price shocks, currency volatility, and supply disruptions, particularly from the Middle East, which accounts for roughly 45% of crude oil imports, 60% of natural gas imports, and over 90% of LPG imports.

Recent geopolitical developments, particularly the 2026 tensions around the Strait of Hormuz, have reinforced the urgency of this challenge. International crude oil prices surged nearly 75% in just six weeks during early 2026, from around USD 66 per barrel in late February to approximately USD 113 per barrel by early April. The LPG crisis that followed, affecting over 330 million Indian households, highlighted the direct link between geopolitical instability and domestic energy access. India’s energy policy is now shifting from a narrow focus on affordability and decarbonisation toward a broader framework centred on resilience, reliability, and self-reliance.

What Does India’s Energy Profile Look Like Today?

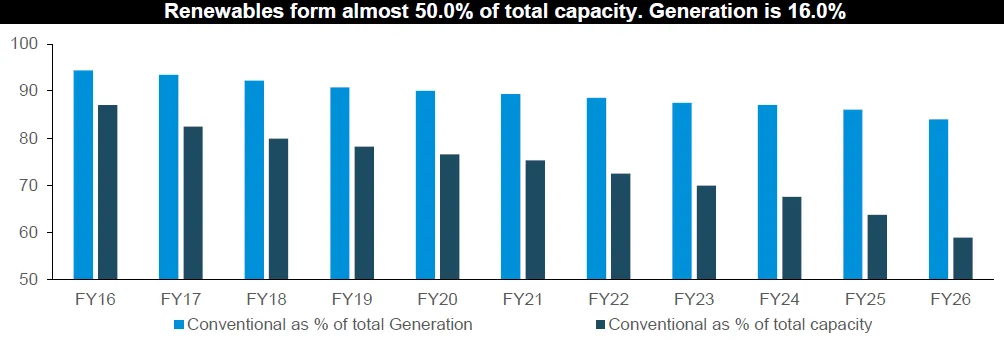

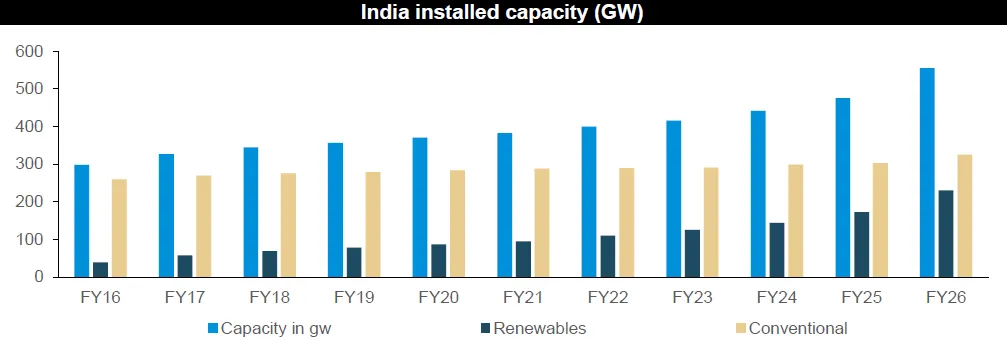

India’s total installed power capacity crossed 532 GW as of FY26, with renewables now forming close to 50% of installed capacity. However, renewables contribute only about 16% of actual electricity generation, while conventional sources (primarily coal and large hydro) continue to account for over 80% of power produced. This gap between installed capacity and generation underscores the intermittency challenge that renewables face, and explains why coal remains the backbone of India’s electricity system.

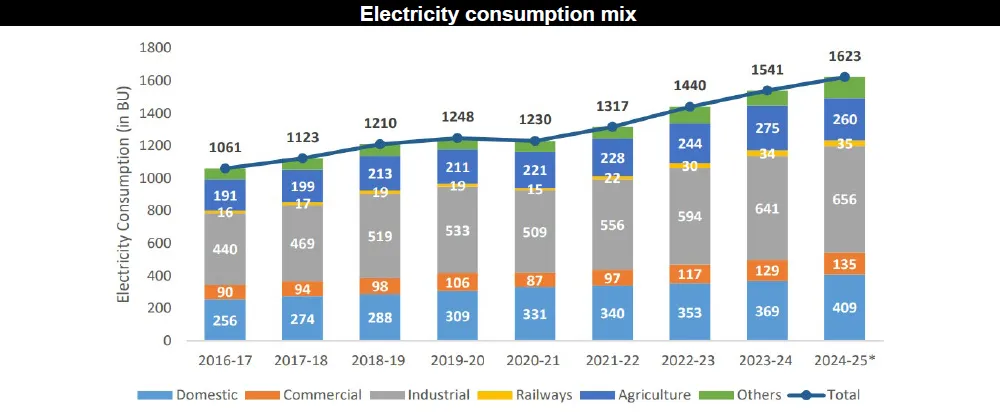

Total electricity consumption reached an estimated 1,623 billion units (BU) in FY25, up from 1,061 BU in FY17, representing a compound annual growth rate of approximately 5.5%. Industrial consumption is the largest segment at 656 BU, followed by domestic consumption at 409 BU and agriculture at 260 BU. Demand growth is being driven by urbanisation, industrial expansion, data centre proliferation, rising appliance penetration, and the electrification of transport.

Import dependence: where is the risk concentrated?

India’s 40% total energy import dependence creates macroeconomic vulnerability, but the risk is heavily concentrated in crude oil. The country imported 242 million tonnes of crude oil in FY25 against domestic production of only 29 MT. Crude oil imports as a percentage of GDP have declined from around 8% in FY14 to approximately 3–4% in FY26, partly due to GDP growth and partly due to periods of lower oil prices.

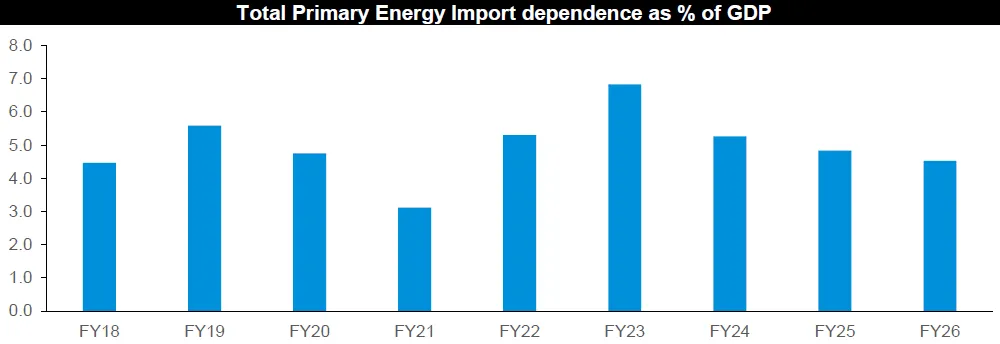

Total primary energy import dependence as a share of GDP has similarly moderated, from nearly 7% in FY23 to about 4.5% in FY26. These improvements, however, do not eliminate the underlying vulnerability; they reduce it in relative terms while absolute import volumes continue to rise.

India’s Energy Import Dependence

Energy Source | Import Dependence (%) | Share of Total Import Bill |

Crude Oil | ~88–89% | ~67% (Oil) |

Natural Gas | ~50% | ~8% (Gas + Nuclear) |

Coal | ~23% | ~25% (Coal) |

Total Energy | ~40% | 100% |

Source: MOSPI 2026

How Is India’s Energy Policy Shifting?

The policy reorientation is visible across multiple dimensions. Energy policy is being reframed from a narrow focus on affordability and decarbonisation toward a broader objective of resilience, reliability, and self-reliance. This shift changes how different parts of the energy value chain are prioritised and where capital allocation is directed.

The government has signalled that India could add up to 80 GW of new coal-based capacity by 2032, alongside its renewable expansion targets. This reflects a "Thermal + Renewable" framework where coal provides baseload stability and renewables address incremental demand growth. India is unlikely to choose between thermal and renewable generation; it needs both. Coal continues to account for over 70% of electricity generation and remains critical for managing baseload and peak demand, particularly during periods when renewable output is low.

On the renewable side, India has set a target of 500 GW of non-fossil fuel capacity by 2030. As of early 2026, approximately 271–272 GW of non-fossil fuel capacity has been achieved, according to Central Electricity Authority data. India achieved the milestone of 50% of its installed electricity capacity from non-fossil fuel sources in June 2025, five years ahead of the 2030 target set under its Nationally Determined Contribution to the Paris Agreement. Annual renewable capacity additions reached a record 44.5 GW in calendar year 2025, nearly double the 24.7 GW added in 2024. Solar energy leads with installed capacity crossing 132 GW by late 2025, while wind energy surpassed 56 GW by early 2026.

Ethanol blending has already reached 20%, and the government is pushing to move beyond that level through guaranteed pricing, interest-subvention schemes, and multi-feedstock flexibility. India has also launched the National Critical Mineral Mission with an outlay of Rs 34,300 crore to reduce dependence on imported minerals needed for clean energy technologies. The National Green Hydrogen Mission targets 5 million tonnes of annual green hydrogen production by 2030, with an investment pipeline of Rs 8 lakh crore.

Where Are the Investment Opportunities in Energy Security?

Direct energy security beneficiaries

This layer includes power utilities with fuel-secure thermal assets and scalable renewable platforms (NTPC, JSW Energy, Coal India), transmission infrastructure companies (APAR Industries, Siemens Energy, KEC International), battery energy storage system manufacturers (Waaree Energies, Exide Industries, Amara Raja), and power financiers (PFC, REC). India is targeting approximately 236 GWh of battery energy storage by 2032 from a negligible current base. Transformation substation capacity is expected to grow from 1,451 GVA in FY26 to 2,412 GVA by FY32, while total installed transmission lines above 220 kV are projected to increase from 507,000 circuit km in FY26 to 649,000 circuit km by FY32.

Enabling infrastructure beneficiaries

Cables, wires, pipes, and engineering equipment companies form this layer. KEI Industries, Polycab India, Welspun Corp, and Jindal SAW are positioned to benefit from the buildout of transmission networks, gas pipelines, and water infrastructure. India has approximately 10,400 km of gas pipelines under construction as part of the "One Nation, One Gas Grid" initiative. The cables and wires segment benefits from rising investment in inter-state transmission systems, growing adoption of HVDC corridors, data centre development, and industrial expansion.

Substitution and long-duration beneficiaries

Ethanol producers (Balrampur Chini Mills, Triveni Engineering, Praj Industries), nuclear energy players (BHEL, Larsen and Toubro, MTAR Technologies), and EV-linked companies (TVS Motor, Ather Energy, Tata Motors) form this layer. The government’s ambition to scale nuclear capacity materially by FY32 and further by 2047, combined with recent policy measures such as opening the sector to private participation and allocating funding for small modular reactor development, signals that nuclear is moving from aspiration to execution.

What Are the Key Risks to This Thesis?

Several risks could slow or disrupt the energy security buildout. First, renewable execution remains uneven. Despite record capacity additions, renewables contribute only 16% of generation against nearly 50% of installed capacity. Grid integration, land acquisition bottlenecks, and transmission constraints continue to limit the effective utilisation of renewable assets. Second, the transition from fossil fuel imports to critical mineral imports creates a new form of dependence. India currently imports the bulk of lithium, nickel, cobalt, and rare earths needed for batteries, solar panels, and wind turbines. Replacing oil dependence with mineral dependence carries its own geopolitical risks. Third, fiscal exposure to oil price volatility remains significant. India’s energy revenues, including those at both central and state levels, reached nearly Rs 10 lakh crore (USD 118 billion) in FY25, accounting for 14% of all government revenue. Fossil fuel subsidies were three times those allocated to clean energy in FY25, and the structural fiscal dependence on oil and gas revenues could slow the pace of transition.

Finally, many stocks aligned with the energy security theme have already delivered strong absolute and relative returns. The theme has room to run, supported by strong momentum, but valuations in certain segments may limit near-term upside.

What Is the Outlook for India’s Energy Security?

India’s energy security challenge is structural, not cyclical. The country’s energy demand will continue to grow, driven by a population of 1.4 billion, rapid urbanisation, industrial expansion, and the electrification of transport and digital infrastructure. The policy response is now oriented toward reducing the economy’s sensitivity to imported energy shocks through a multi-pronged approach: expanding domestic coal production and ensuring fuel availability for the thermal fleet, accelerating renewable deployment and storage infrastructure, building transmission capacity to integrate dispersed generation, advancing nuclear energy, scaling ethanol blending and green hydrogen, and strengthening strategic petroleum reserves.

The scale of the opportunity is significant. India’s installed power capacity needs to more than double from current levels to meet projected demand by 2037. NTPC alone plans to expand from 90 GW to 244 GW by that year. Transmission infrastructure needs to grow by nearly 30% over the next six years. Battery storage capacity needs to scale from near-zero to 236 GWh. This implies a broad, sustained domestic capex cycle across generation, transmission, storage, grid modernisation, and fuel substitution, creating a long runway of investment opportunities for companies with execution capability, policy alignment, and domestic competitive strength.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox