For over five decades, the global oil trade has been conducted almost exclusively in US dollars. This arrangement, known as the petrodollar system, gave the United States an extraordinary structural advantage: every country that needed oil first had to acquire dollars, and every country that sold oil accumulated dollars that were then recycled into US Treasury bonds. This feedback loop financed American deficits at artificially low interest rates, underpinned the dollar’s reserve currency status, and gave Washington unmatched geopolitical leverage.

That system is now under severe stress. The 2026 Iran - USA & Israel War, a global oil glut, the expansion of BRICS, and China’s growing role as the world’s largest oil importer have combined to accelerate a shift that was already underway. The petrodollar is not dead, but its dominance is eroding. In its place, a new contender is gaining traction: the petroyuan.

The petrodollar system was born out of two crises. In 1971, President Richard Nixon ended the dollar’s convertibility to gold, dismantling the Bretton Woods system and causing the dollar to lose value rapidly. Two years later, the 1973 Arab–Israeli War triggered an oil embargo by OPEC members against the United States and its allies. Oil prices quadrupled. The American economy, already struggling with inflation, was hit by fuel shortages.

Washington turned the crisis into an opportunity. In 1974, US Treasury Secretary William Simon brokered a deal with Saudi Arabia. The terms were straightforward: Saudi Arabia would price all its oil exports exclusively in US dollars and invest its surplus oil revenues in US Treasury bonds. In return, the United States would provide military protection and guaranteed weapons sales. The arrangement was never formally published, but its effects were immediate and far-reaching.

Other OPEC members followed Saudi Arabia’s lead. Within a few years, virtually all global oil trade was denominated in dollars. Any country that wanted to buy oil, whether Japan, Germany, India, or Brazil, first had to hold dollars. This created permanent, structural demand for the US currency. The recycling of oil revenues into US Treasuries allowed Washington to borrow in its own currency at low interest rates, a privilege the French economist Valéry Giscard d’Estaing called America’s “exorbitant privilege.”

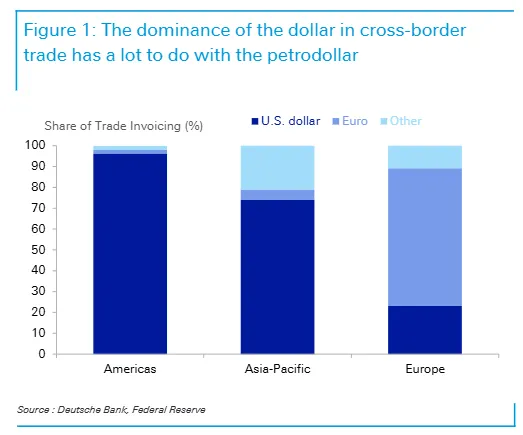

At its height, the petrodollar system operated as follows: oil-exporting nations earned dollars from their exports, deposited those dollars in Western banks or US Treasuries, and the US used that capital inflow to finance its trade and fiscal deficits. Gulf states became the largest buyers of American weapons. Saudi Arabia’s sovereign wealth holdings grew into the hundreds of billions. The US dollar accounted for roughly 80% of all global oil transactions.

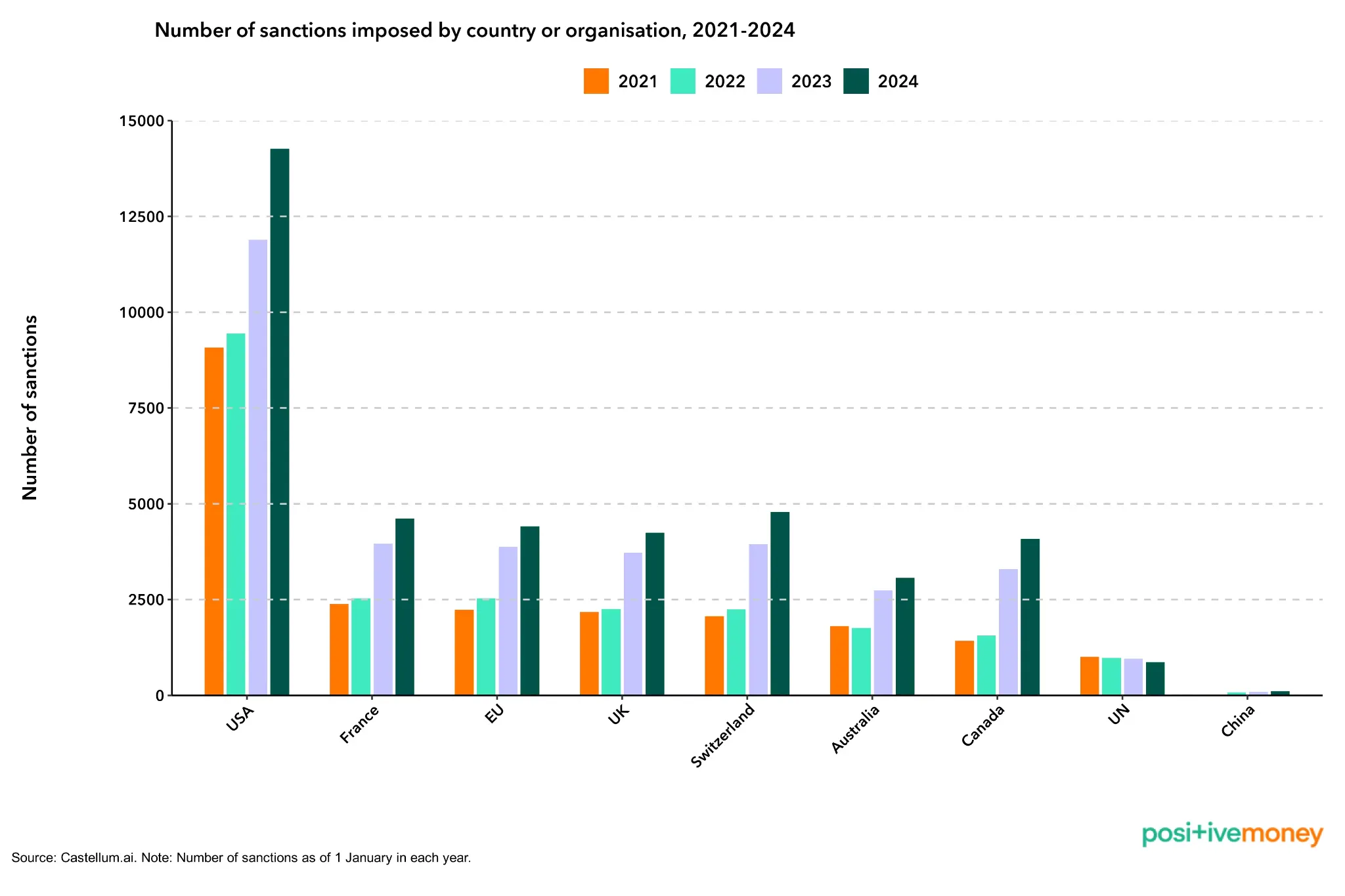

The system also enabled the “weaponisation” of the dollar. Because global trade was so dependent on dollars and the US-controlled SWIFT payment network, Washington could impose financial sanctions on any country and effectively cut it off from the global economy. This leverage was used against Iran, Russia, Venezuela, North Korea, and others.

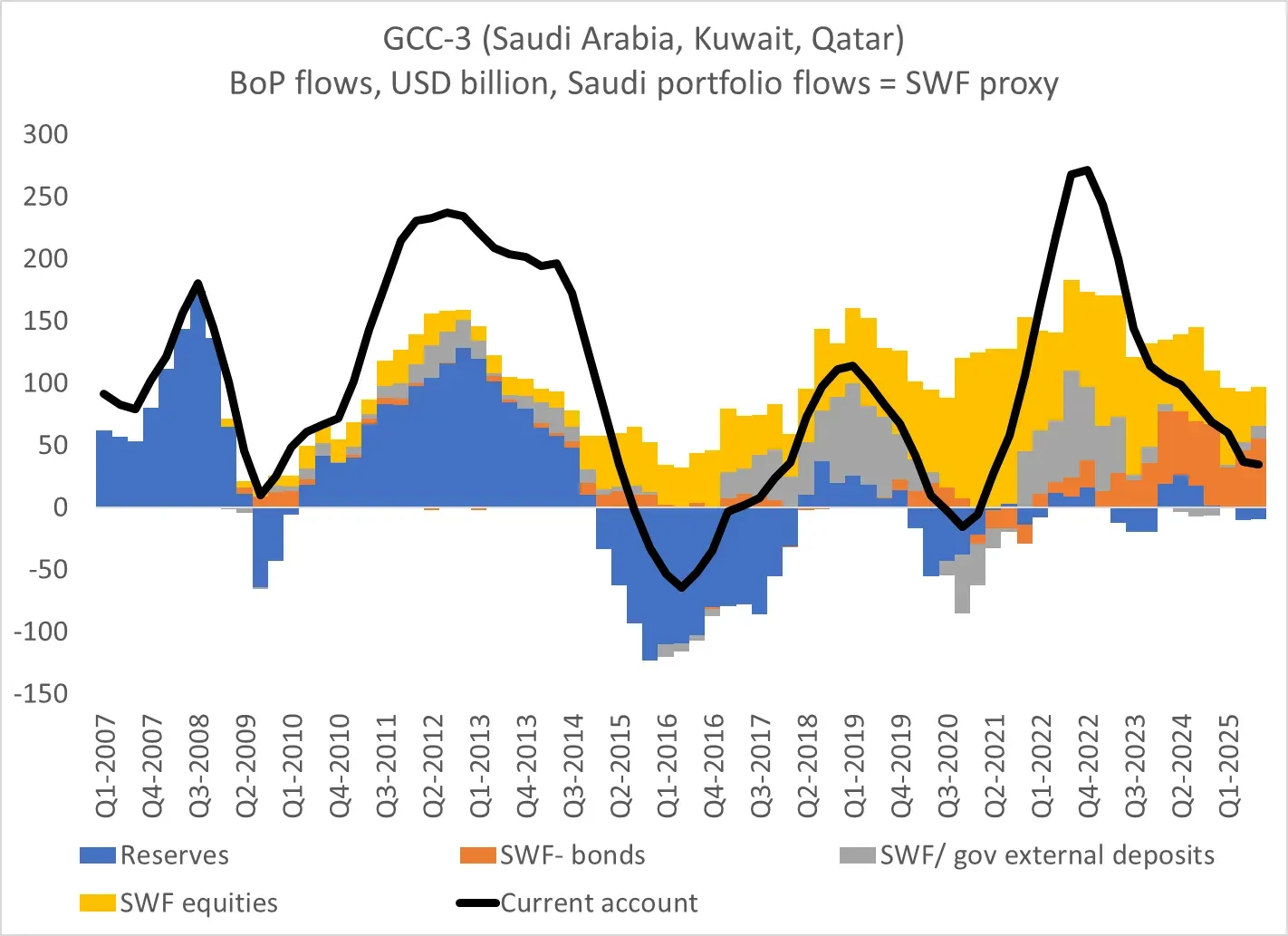

Gulf states collectively accumulated over $4–5 trillion in sovereign wealth fund assets, with the Saudi Public Investment Fund alone becoming one of the largest investors in the world. These funds held significant positions in US equities and fixed income.

By 2025, the mechanics of petrodollar recycling had changed substantially. Brad Setser, a former US Treasury economist, documented that petrodollar flows had “more or less dried up.” Saudi Arabia was running an external deficit. Oil prices had fallen to $60–70 per barrel, below Saudi Arabia’s fiscal breakeven price. The 2 largest oil producers are Saudi Arabia and Russia which together generated essentially zero petrodollars in 2025.

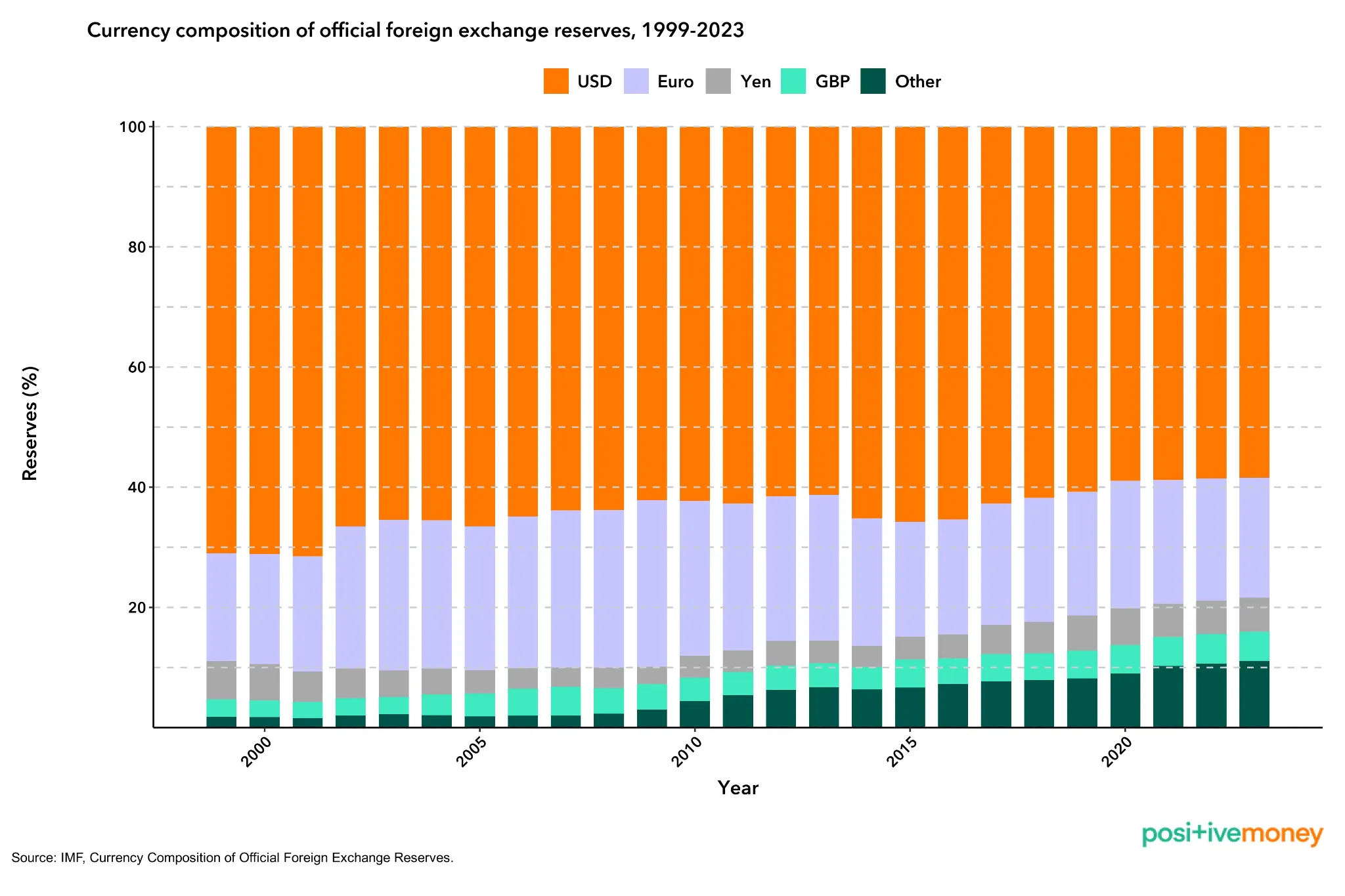

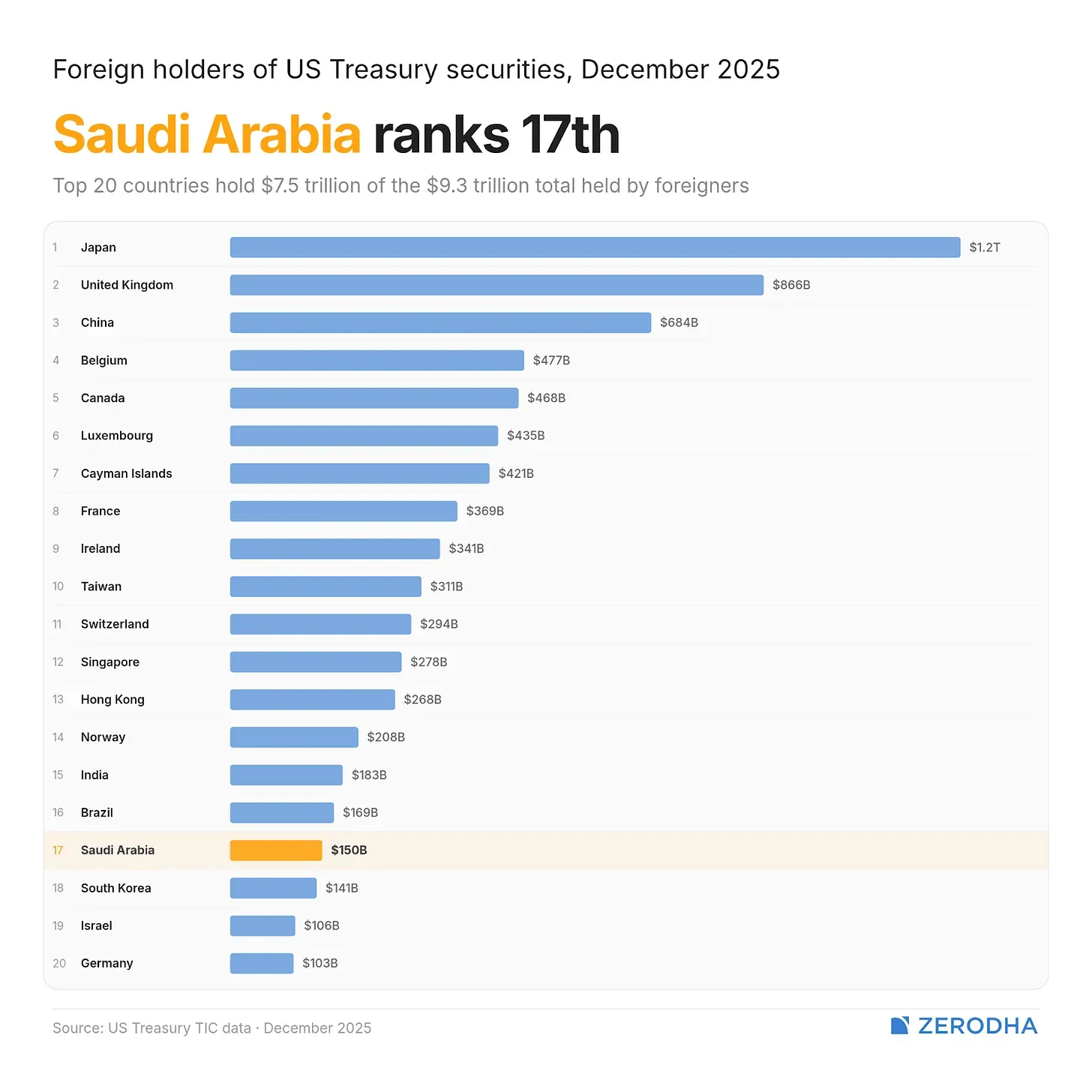

Gulf states stopped parking most of their oil revenues in US Treasuries. Saudi Arabia, despite being the largest Gulf economy, ranked only 17th globally in US Treasury holdings. Instead, sovereign wealth funds channelled reserves into global equities, what some analysts call “petro-equities.”

Roughly 70% of Gulf SWF assets were in equities, not fixed income. The money was still in dollar-denominated assets (Apple, NVIDIA, etc.), but the traditional Treasury-recycling loop had broken down.

In June 2024, the 50-year anniversary of the original US–Saudi petrodollar agreement passed without renewal. Under its Vision 2030 programme, Saudi Arabia signalled it would no longer tie its economic future to a single superpower.

Riyadh began accepting payments in Chinese renminbi, euros, and even digital assets for some transactions. Saudi Arabia joined BRICS in 2024, alongside Iran, the UAE, Egypt, and Ethiopia - a bloc that now represents a significant share of global oil production.

The weaponisation of the dollar through sanctions had also pushed oil-exporting nations to seek alternatives. After Western sanctions froze Russian central bank reserves in 2022, many governments concluded that dollar-denominated reserves could be seized at any time. This eroded trust in the system.

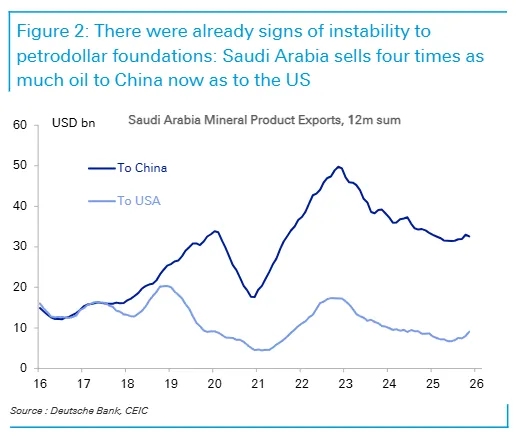

The centre of gravity in global oil demand has moved from the West to Asia. China is now the world’s largest oil importer, purchasing 11.55 million barrels per day in 2025. China posted a record $1.189 trillion trade surplus in 2025.

Asian manufacturing economies such as China, India, South Korea, Taiwan collectively hold trillions of dollars in reserves and have become the primary engine of global dollar liquidity, not the Gulf.

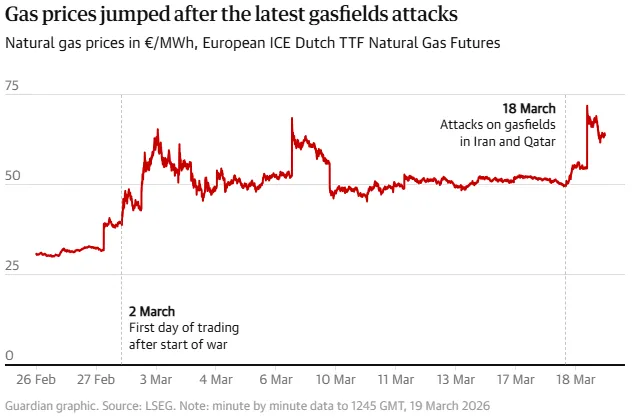

On 28 February 2026, the United States and Israel launched Operation Epic Fury, a coordinated military campaign against Iran. The strikes targeted Iranian leadership, military infrastructure, and energy facilities, including the South Pars gas field, one of the largest natural gas reserves in the world, shared with Qatar.

Iran responded with asymmetric warfare, orchestrating a “soft closure” of the Strait of Hormuz, a waterway through which approximately 20% of the world’s oil passes daily. Shipping insurance premiums surged by 500%. Oil prices spiked from $66 to $120 per barrel within weeks. The IMF projected that a prolonged standoff could erase $2.2 trillion from global GDP.

The 2026 Gulf War triggered the most severe energy price shock since the 2022 Russia-Ukraine crisis. Brent crude rose by as much as 60% since the US-Israeli war on Iran started on 28 February, briefly surging above $119 a barrel. European gas prices more than doubled, with the Dutch wholesale gas price hitting €68 per megawatt hour the highest since late December 2022. We are also seeing gas shortages hitting India.

The war exposed the fragility of the petrodollar system. Gulf allies of the United States , whose petroleum exports were curbed, energy facilities damaged, and airspaces disrupted, refused to allow Washington use of their territory or airspace for strikes against Iran.

The very nations whose security was supposedly guaranteed by the petrodollar pact were now bearing the costs of a war they did not start, while questioning whether US protection was worth the price.

This conflict is testing the “foundations of the petrodollar regime.” If the Gulf moved closer to Asia in trade and investment relationships and priced less oil in dollars, there would be significant downstream effects on the dollar’s usage in global trade and savings.

The petroyuan refers to the use of the Chinese yuan (renminbi) to price and settle crude oil transactions. China formally launched yuan-denominated oil futures contracts on the Shanghai International Energy Exchange (INE) on 26 March 2018. The goal was to create a pricing benchmark for Asian oil demand that rivalled the dollar-based Brent and WTI benchmarks.

China backed these contracts with gold convertibility: foreign holders of yuan-denominated oil contracts could convert their yuan into gold on the Shanghai Gold Exchange. This was designed to address concerns about the yuan’s limited convertibility and give oil exporters confidence that their earnings would hold value.

China also built parallel financial infrastructure. The Cross-Border Interbank Payment System was established as an alternative to SWIFT. By late 2025, the mBridge project, a digital currency platform backed by the central banks of China, the UAE, Saudi Arabia, Thailand, and Hong Kong, had processed over $55.5 billion in transactions, with the digital yuan accounting for 95% of the volume.

Several countries have adopted the petroyuan for oil transactions. Russia’s Gazprom Neft has settled all of its crude oil sales to China in renminbi since 2015. Iran, under heavy US sanctions, routes its oil to China via a “dark fleet” of tankers, with settlements conducted entirely outside the US banking system. Venezuela and Indonesia have also settled portions of their China-bound oil trade in yuan. As of early 2026, approximately 166 million barrels of Iranian oil sat in floating storage near Chinese ports, representing a tangible flow of crude settled in yuan.

Saudi Arabia has also engaged in petroyuan discussions. The Saudi Minister of Economy indicated openness to non-dollar oil pricing, and Riyadh has experimented with yuan payments for infrastructure projects. China’s exports surged 21.8% year-on-year in the first two months of 2026, providing the deep reservoir of yuan liquidity needed to finance large-scale oil purchases.

The Gulf War accelerated the petroyuan’s rise. With the Strait of Hormuz partially closed, Iranian oil continued flowing to China through alternative channels, settled entirely in yuan and processed through mBridge, bypassing SWIFT and the US banking system. In March 2026 alone, mBridge handled over $55 billion in trade.

BNP Paribas estimated that if $600 billion to $1 trillion of oil trade shifted to renminbi settlement, the yuan’s share of global payments through SWIFT would rise to 3% or more, surpassing the Japanese yen to become the fourth most widely used global currency. Gold prices breached $5,400 per ounce in March 2026, reflecting declining confidence in fiat currencies and increased demand for the gold-backed yuan settlement mechanism.

The petroyuan faces real constraints. The dollar still accounts for roughly 80% of global oil transactions. The yuan’s limited convertibility and Beijing’s capital controls make it less attractive as a reserve asset than the dollar. Deep, liquid US financial markets, legal stability, and decades of institutional trust cannot be replicated quickly.

The US has also responded. The Trump administration introduced the concept of the “Petro-AI-Dollar,” attempting to link access to American artificial intelligence hardware and software to continued use of the dollar in trade. Washington is leveraging its dominance in AI to create new structural demand for the currency.

Most analysts assess that while the petroyuan will gain ground, it is unlikely to fully supplant the petrodollar in the near term. The more probable outcome is a multipolar currency system where dollar-denominated and yuan-denominated oil trades coexist.

The petrodollar system that has underpinned American financial dominance since 1974 is weakening. Gulf states are diversifying away from US Treasuries into equities and non-dollar assets. Saudi Arabia is no longer exclusively tied to the dollar. The 2026 Gulf War has fractured the security-for-currency bargain that sustained the system. China, as the world’s largest oil importer with a $1.189 trillion trade surplus, is building the financial infrastructure via CIPS, mBridge, Shanghai INE futures and gold convertibility, to support an alternative.

The petroyuan is not replacing the petrodollar overnight. But the era of unchallenged dollar dominance in global oil trade is ending. What is emerging is a fragmented, multipolar system where the dollar and the yuan compete alongside digital currencies and gold-backed settlement mechanisms. For the United States, this means higher borrowing costs and diminished leverage. For China and the broader BRICS bloc, it means greater economic sovereignty at the cost of increased volatility and complexity.

The structure of global power is shifting. The petrodollar was both a product and a pillar of American hegemony. Its erosion signals a deeper realignment of the international economic order.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart