As the subscribers are growing in our high risk high return momentum portfolio, there are increasing number of investor queries and concerns about what happens to these portfolios in the times of risk.

In this post we try to address your queries,

The momentum portfolio is composed of stocks that are trending. Investors herd towards trending stocks and that creates a lasting trend. But in bad times, investors quit these high valued trending stocks the quickest and a momentum portfolio is prone to as much drawdown as the market at bad times. Even though it may rise back up much more quickly than the market.

There is always momentum somewhere or the other in equity markets. Sometime cyclicals shine and other times defensives. Sometimes value works, other times growth. But there are those times like March 2020 when nothing seems to work.

At Wright Research we handle the risk in momentum investing using a methodology called systematic deallocation. What that means in simple words is that we reduce the stocks in the portfolio by selling a certain percentage and buying liquid ETF instead of that.

Our deallocation policy

It's quite simple.

- Deallocate 10% of the portfolio to liquidbees if there is a 10% drawdown in the short term (a month or so). If there is 10% more drawdown, deallocate 10% more and so on.

- Once the portfolio recovers from this short term drawdown - reallocate in a similar fashion

Also, like all markets are not the same, similarly all drawdowns are not the same. A drawdown in a high risk environment is more lethal than one in a low risk environment. So we deallocate more aggressively when we see high risk.

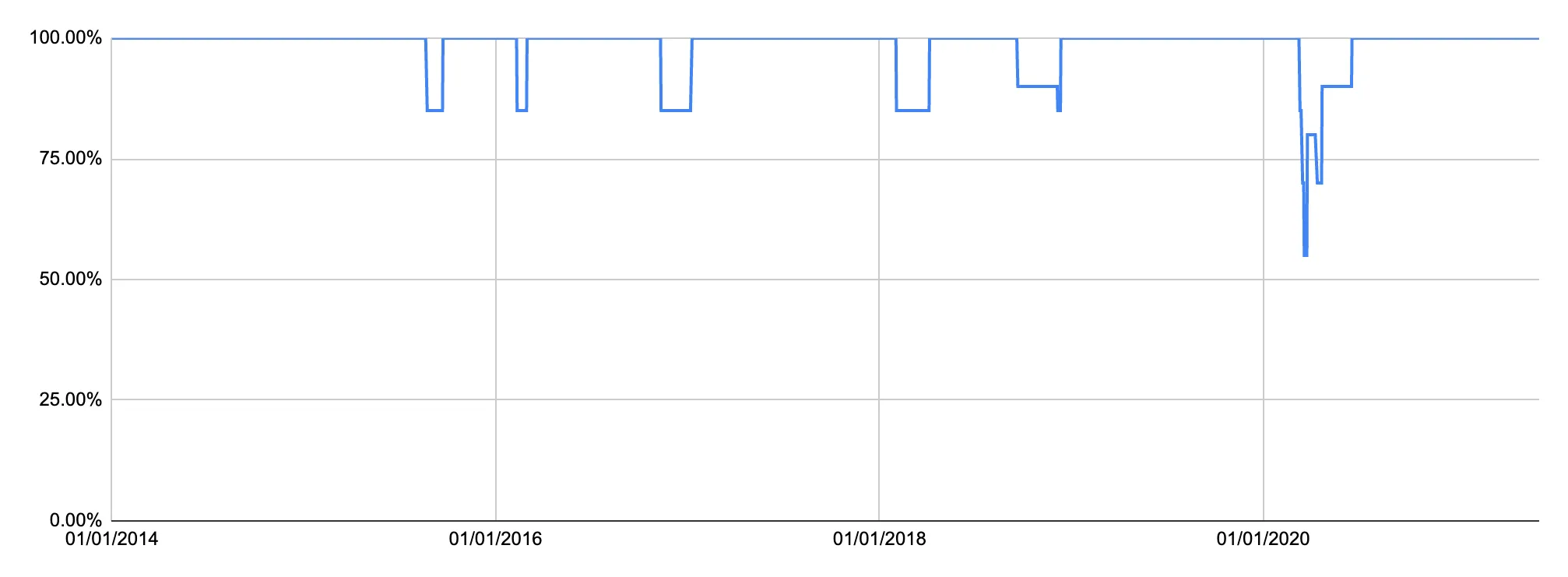

How does that look in practise?

Since 2014, this is how our deallocation schedule would have kicked in. There are short periods in 2018-19 and the famous March 2020 crash where there would be deallocation.

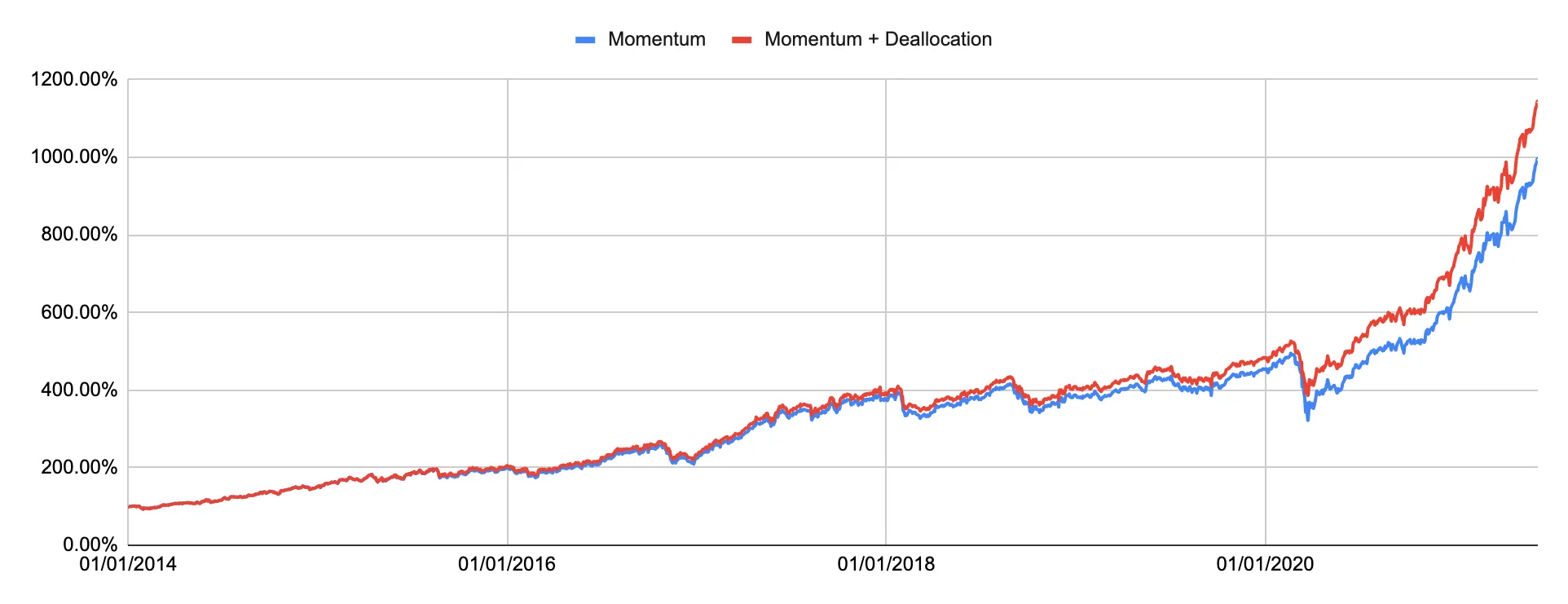

How it affects the performance of momentum strategy?

By a fair bit! Here's the performance of momentum portfolio before & after deallocation.

Systematic deallocation has

- improved the historical CAGR from 35% to 37.5%

- reduced the drawdown from 35% to 26%

While we like to show you pure momentum returns in our backtested data, rest assured that we have a well defined methodology to reduce risk in times of trouble for the portfolio!

I hope this post gives you the reassurance that there are tight safeguards in place for bad times in your Wright momentum portfolio.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox