Demand for data center capacity is rising at a speed the supply chain was never designed to match. Cloud providers, AI labs, and enterprises want to deploy compute faster than utilities can deliver power, manufacturers can ship equipment, and contractors can complete builds. The result is a widening gap between planned capacity and operational capacity. Forecasts now point to demand roughly doubling within a few years, while the physical inputs that data centers depend on stay in short supply. This article looks at the scale of that demand, the reasons supply lags behind it, and what the gap means for the companies racing to build.

How fast is data center demand growing?

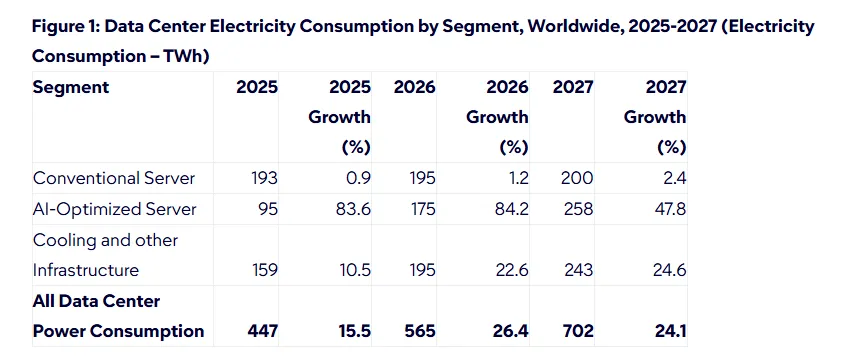

Data center demand is growing on two fronts at once: electricity and physical capacity. Gartner forecasts global data center electricity consumption will reach 565 terawatt hours in 2026, up 26% from 447 in 2025, and 702 the following year.

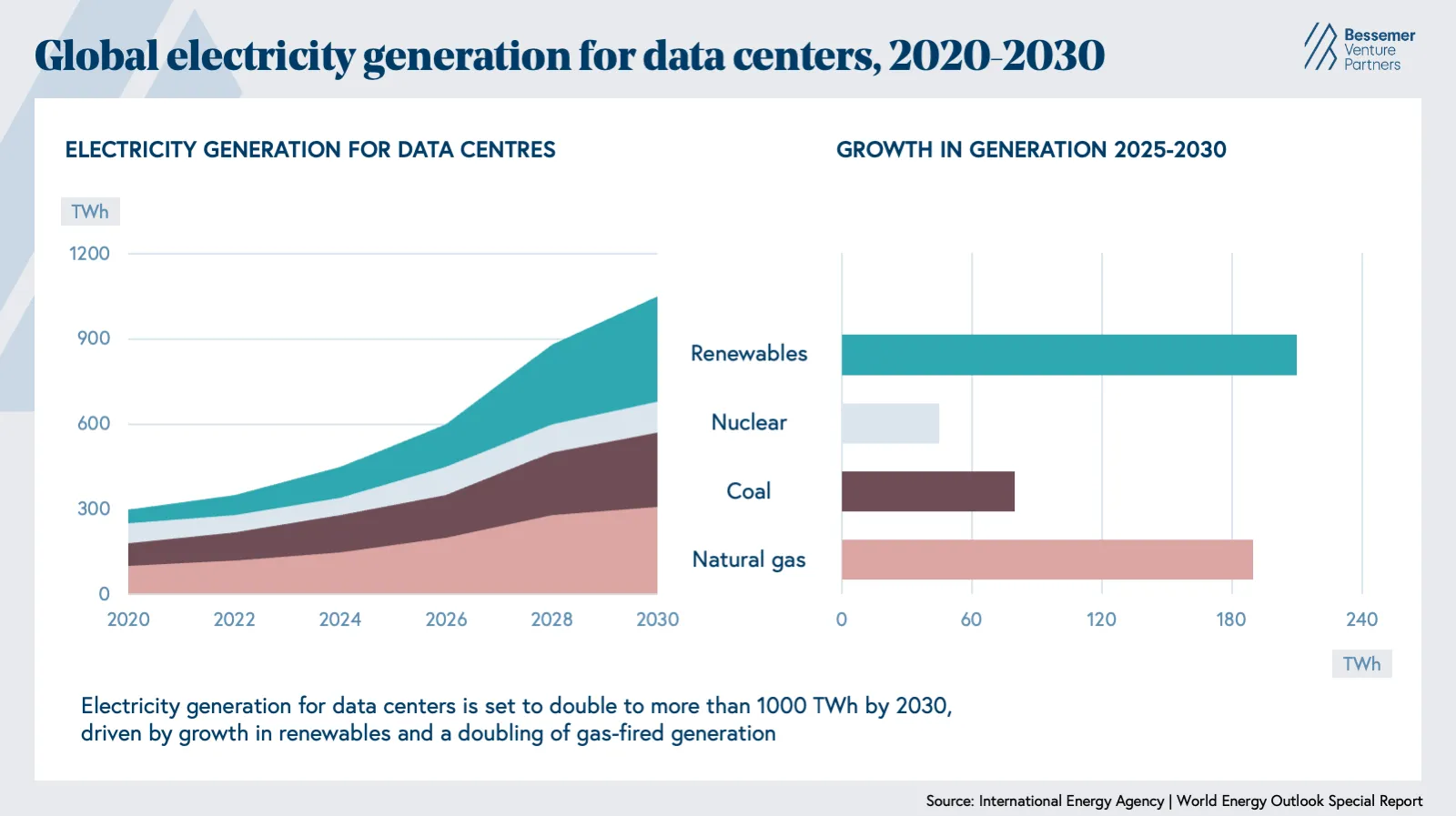

By 2030 the figure is expected to pass 1,200 terawatt hours. In the United States, power demand from data centers is expected to climb from 31 gigawatts in 2025 to 41 in 2026 and 66 in 2027, more than double in two years. Over the same period, data centers are expected to grow from 4.1% of US peak summer power demand to 8.5%.

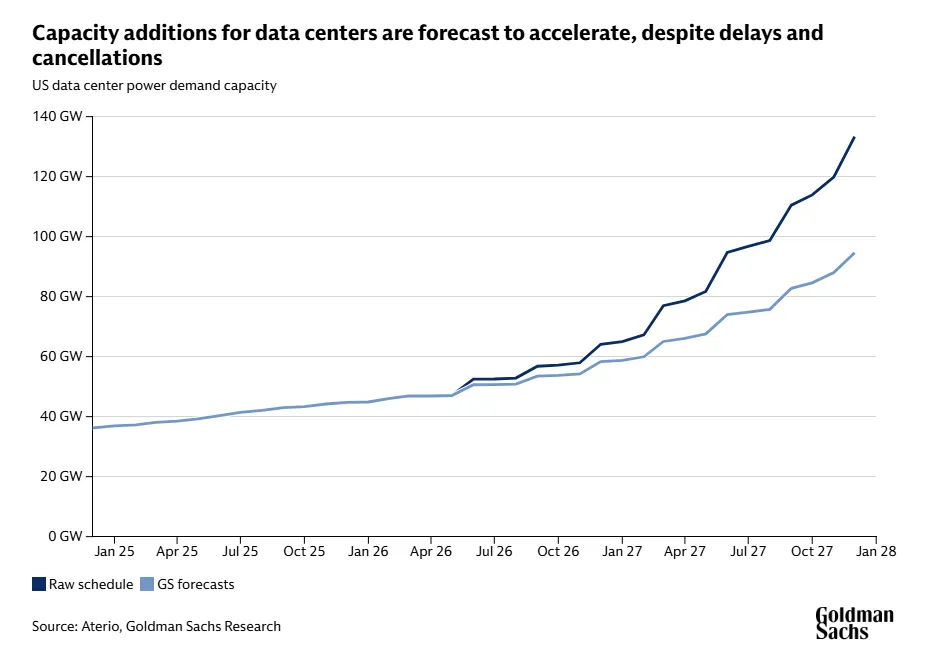

The pipeline of announced projects points the same way. Roughly 190 gigawatts of hyperscale capacity announced across 777 projects as of early 2026, of which only about 12 gigawatts is operational today. In the United States, data centers are on track to consume more electricity than all energy-intensive manufacturing combined.

AI workloads are driving the increase

The growth traces directly to AI. Gartner estimates AI-optimized servers will account for 31% of data center power consumption in 2026, and their consumption will surpass that of conventional servers in 2027. Training and inference for large models draw far more power per rack than traditional cloud workloads. Cloud-era racks ran at 20 to 40 kilowatts. Some current AI training clusters run at 500 to 600 kilowatts per rack, and chip makers are designing toward 1 megawatt. Each step up in density raises both the power and the cooling load of every new facility. Global spending on data centers could reach 7 trillion dollars by 2030.

Why is supply struggling to keep up?

The constraint is physical rather than financial. Capital is available, and valuations across the sector are high. The problem is the set of inputs that turn capital into working facilities. Three bottlenecks stand out: power and grid access, critical equipment, and skilled labor. Each runs on a timeline measured in years, which is the source of the mismatch with demand.

Power and grid connections set the pace

A data center can be built in 12 to 18 months and connecting it to the grid currently takes five to seven years. That gap is now the main limit on AI capacity. Interconnection queues are long because utilities must study each new load, plan generation, and build out transmission before a facility can draw power at scale. Gartner describes power availability as the new constraint on scaling AI and on protecting margins across the industry. Only about 50 to 60% of capacity is scheduled for the next one to two years to come online on time, after adjusting for delays and cancellations.

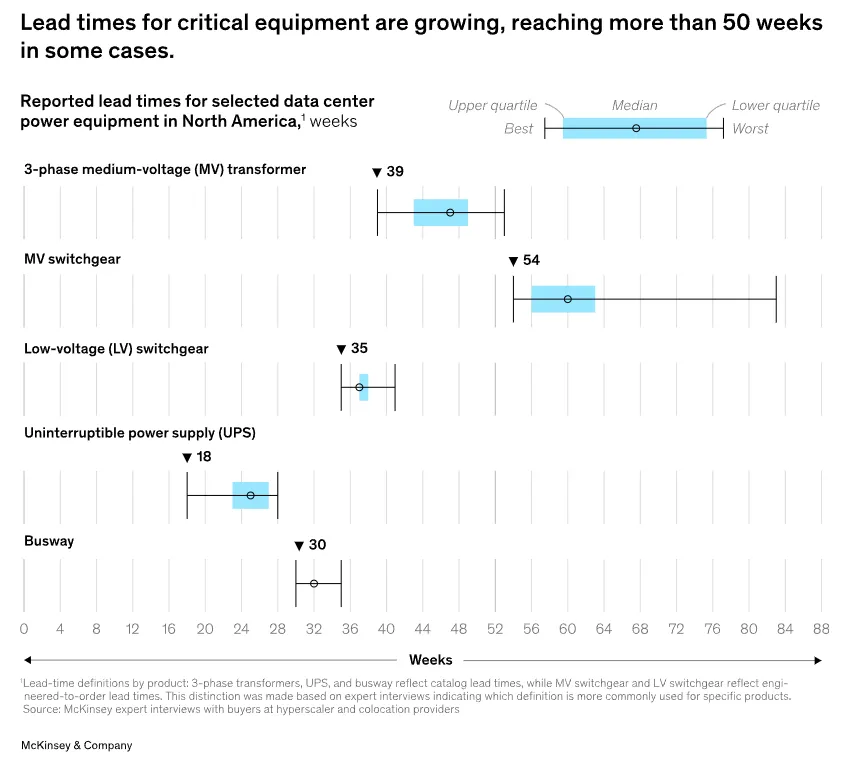

Critical equipment carries multi-year lead times

Even where power is available, the hardware to deliver it is back-ordered. The table below shows how far order books have stretched for the components that move and convert electricity inside a facility.

Critical equipment | Lead time now | Before the pandemic |

High-voltage transformers | Up to 5 years | About 1 year |

Medium-voltage switchgear | Up to 80 weeks | Far shorter |

Transformers (distribution) | Up to 50 weeks | Far shorter |

Sources: McKinsey, Bessemer Venture Partners, Siemens Energy.

Transformer demand rose 119% between 2019 and 2025, while manufacturing capacity lagged, pushing lead times from incumbent suppliers to as long as five years. These are large, highly engineered devices built to order by a small number of manufacturers, which makes the bottleneck slow to clear. Switchgear and high-voltage cable face similar backlogs. The shift to higher-density, 800-volt direct current architectures adds further pressure, since it forces suppliers to redesign and requalify products on shorter cycles.

The skilled workforce is shrinking

Construction and electrical labor is the third constraint. The construction industry faced a shortage of roughly 439,000 workers in late 2025. Peak crew sizes on data center sites have grown from about 750 during the cloud era to between 4,000 and 5,000 today. The average age of the data center workforce is 53, and 60% of providers report difficulty filling open roles. Labor is now as likely to delay a project as power or permitting, which puts a hard limit on how many builds can run at once.

What does the gap look like in the market?

The shortage shows up clearly in real estate. In North America, the primary market vacancy rate fell to a record low of 1.4% at the end of 2025, down from 1.6% at mid-year, according to CBRE. About 74% of capacity under construction is already preleased, which means most new supply is committed before it opens. Asking rates for larger requirements have moved above 200 dollars per kilowatt per month. Supply is expanding at record rates, and demand still absorbs it faster than it arrives.

Delays compound the tightness. Of 110 data center projects slated to come online in 2025, more than a quarter slipped due to power, permitting, and construction constraints. The pressure is uneven across regions. The Mid-Atlantic, Mid-Continent, and Northwest power markets are facing elevated reliability risk, because planned generation there is limited relative to incoming demand. Texas and Georgia are expected to tighten less, since both have significant new power generation in the pipeline. Some of the tightest markets may have to turn future projects away.

Who feels the squeeze, and why does it matter?

The gap has consequences beyond the firms that build the facilities. Three groups feel it most directly.

Hyperscalers and AI developers carry the timing risk

When power, transformers, or skilled crews become roadblocks, an entire build slips, and capital that has already been committed sits idle. Delivery delays can strand billions in deployed capital and can derail long-term business objectives well beyond a single project. This is why large occupiers now prelease space and reserve equipment production slots years ahead of delivery. It is also why they increasingly select suppliers on the strength of their future road maps rather than the products available today.

Electricity users share the load

As data centers take a larger share of peak demand, they tighten regional power markets for everyone connected to the same grid. The data center share of US peak summer demand will roughly double to 8.5% by 2027, which feeds through to prices and reliability for other users. In the tightest regions, utilities and regulators face hard choices about which new loads to connect first and which to defer.

Suppliers and new entrants see an opening

The same shortage that slows builders creates room for new suppliers. Manufacturers from automotive and aerospace moving into the equipment market, drawing on their work in electronic and thermal components. Bessemer tracks startups that compress transformer lead times, automate permitting, and build software to make power use more flexible. For these players, the supply gap is the market opportunity.

Where does the gap go from here?

Companies are responding by working around the slowest parts of the chain. Many are turning to on-site generation, often called Bring Your Own Power, to avoid the interconnection queue. Roughly 50 gigawatts of behind-the-meter gas generation projects were announced in 2025 alone. Governments are involved as well. In April 2026, the United States invoked Section 303 of the Defense Production Act to designate large-scale grid infrastructure as essential to national defense and to expand domestic supply of key components. On the software side, developers are testing tiered service agreements that let flexible AI workloads shift to off-peak hours and return capacity to the grid during stress events.

These measures help at the margin, and they do not change the core arithmetic. Demand is set by chip road maps and AI investment, which move in months. Supply is set by power plants, transformers, and transmission lines, which move in years. The outlook is uncertain in both directions: delays could pull activated capacity below current projections, while new projects could push it higher. The gap between what the market wants and what it can build is likely to persist until the supply chain catches up with the pace of demand.

How is the gap playing out in China and the rest of Asia?

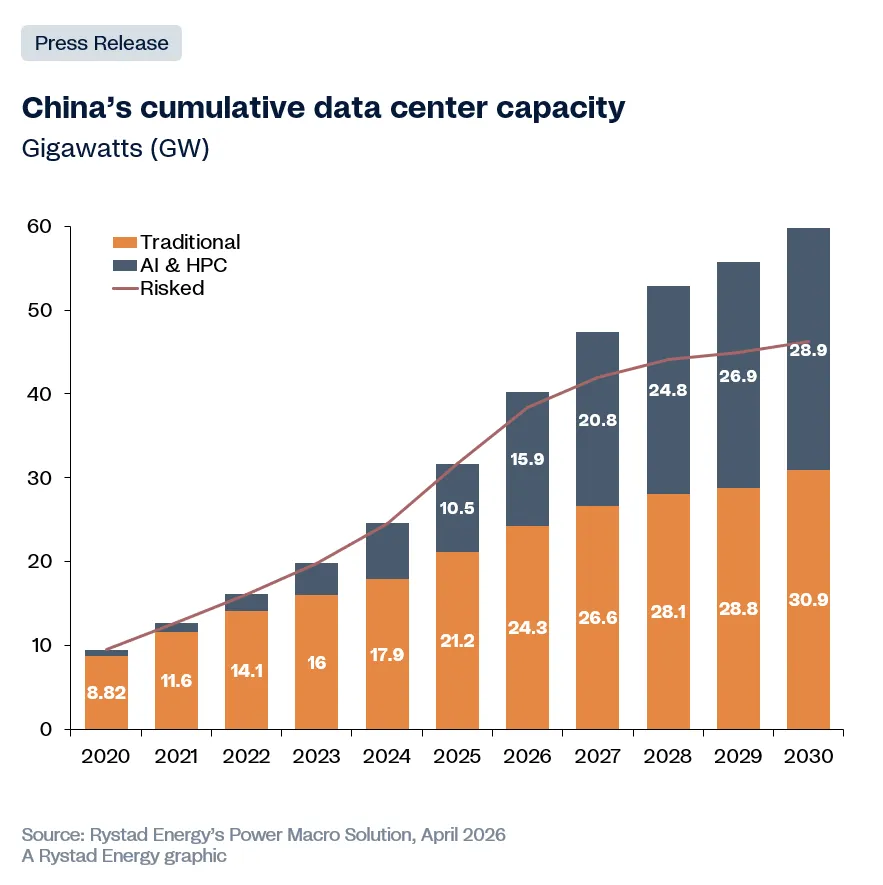

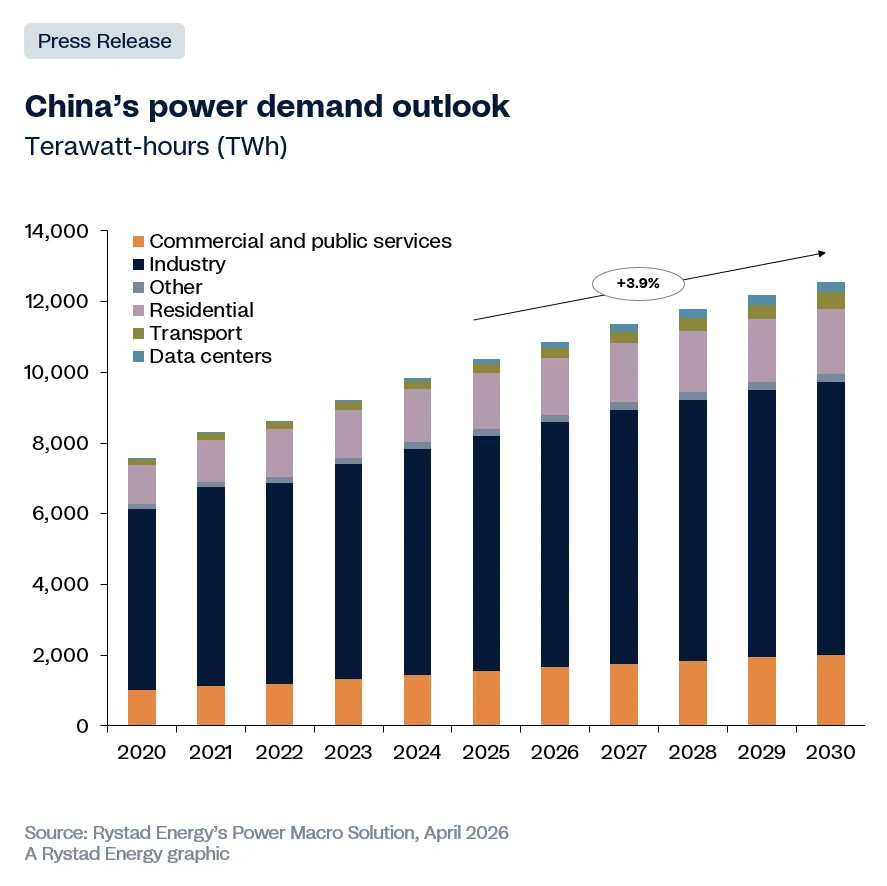

China is the region's largest market. Installed capacity stood at about 32 gigawatts at the end of 2025 and is on track to reach 40 gigawatts in 2026 and around 60 gigawatts by 2030, according to Rystad Energy. Data center power consumption is set to more than double to about 289 terawatt hours by 2030, roughly 2.3 percent of national electricity demand, and data centers are now the country's fastest-growing source of power demand, rising at about 19 percent a year. AI and high-performance computing facilities drive the trend, accounting for about 39 percent of capacity in 2026 and a projected 48 percent by 2030.

China's response to its supply constraints is geographic. The Eastern Data, Western Computing strategy, launched in 2022, channels new capacity toward renewable-rich western provinces, easing pressure on the congested eastern coastal grid where construction approvals are limited. Eight national computing hubs anchor the plan, and the Ulanqab cluster in Inner Mongolia alone has secured around 10 gigawatts of projects. Regulators also enforce efficiency, requiring large data centers to keep power usage effectiveness below 1.3 and to use at least 30 percent renewable energy in eastern regions.

Across the wider Asia-Pacific region, demand is outrunning supply. Regional capacity is projected to roughly double to about 30 gigawatts by 2027 or 2028, and a supply shortfall of 15 to 25 gigawatts is expected over that period, according to White & Case. Investment reached a record 11.6 billion dollars in the region in 2025, per CBRE, with Malaysia, Australia, and India drawing the most interest as power constraints push activity beyond the established hubs.

Market | Operational capacity | Defining feature |

Mainland China | About 32 GW | Largest market; capacity shifting west |

India | About 1.7 GW | Among the fastest-growing in the region |

Singapore | About 1.5 GW | Growth slowed on efficiency grounds |

Johor, Malaysia | About 0.5 GW | Absorbing demand redirected from Singapore |

Sources: Rystad Energy; CBRE; BMI; White & Case. Capacity figures are approximate, year-end 2025.

The Singapore to Johor corridor shows the pattern clearly. Singapore, with about 1.5 gigawatts of operational capacity, has slowed new approvals to prioritize energy efficiency, redirecting demand across the strait to Johor in Malaysia, which now holds close to 500 megawatts of live capacity. Even there, power bottlenecks have delayed some projects by 24 to 36 months. In Japan, CBRE identifies access to grid power as the single biggest constraint on growth in 2026. Build costs have risen across the region, from about 7.7 million dollars per megawatt in 2020 to roughly 10.7 million dollars per megawatt in 2025.

How is the supply gap playing out in India?

India is one of Asia-Pacific's fastest-growing data center markets. Total operational capacity crossed about 1,700 megawatts at the end of 2025, after a record 440 megawatts of new supply during the year, a 160 percent jump over 2024, according to CBRE. Capacity is projected to grow about 30 percent in 2026 on roughly 500 megawatts of fresh supply. Investment commitments reached 56.4 billion dollars in 2025, bringing the cumulative total to about 126 billion dollars, and are expected to pass 180 billion dollars in 2026. The demand comes from cloud adoption, AI workloads, data localization rules, the 5G rollout, and rising digital consumption.

India data center market | 2025 | 2026 outlook |

Total operational capacity | About 1,700 MW | About 2,200 MW |

New supply added | 440 MW (up 160%) | About 500 MW |

Cumulative investment commitments | About $126 billion | Above $180 billion |

Vacancy rate (primary markets) | About 4.3% | Supply-constrained |

Sources: CBRE India Alternate Sectors Outlook 2026; JLL India Data Centre Market Dynamics H1 2025. Mumbai holds roughly 54% of operational capacity.

Supply is concentrated in a few cities. Mumbai holds more than half of operational capacity, and together with Chennai, Delhi-NCR, and Bengaluru it accounts for close to 90 percent of the national total. Demand is running ahead of new supply. JLL recorded 97.9 megawatts of net absorption in the first half of 2025, up 48 percent year over year, with vacancy compressed to about 4.3 percent. Activity is starting to spread to tier-II cities such as Ahmedabad, Visakhapatnam, and Kochi, helped by land availability and supportive state policies.

The constraints mirror the global pattern, with local specifics. Power availability and grid readiness determine whether projects are delivered on time, so operators are signing large renewable agreements to lock in supply, including a roughly 2 gigawatt renewable partnership between CtrlS and NTPC Green Energy. Water for cooling is an added concern, which is pushing new facilities toward liquid cooling. Policy support is strong: data centers carry infrastructure status, and a 20-year tax holiday framework extends incentives to 2047.

Forecasts for 2030 range from about 4 to 5 gigawatts in base scenarios to 8 to 9 gigawatts under AI-accelerated demand. Whether supply keeps pace will depend on power procurement, grid upgrades, and the ability to build beyond the established metros.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox