by Naman Agarwal

Published On March 21, 2026

Battery Energy Storage Systems (BESS) are moving from buzzword to backbone in India’s power sector. In 2025, the country had less than 1 GWh of installed grid‑scale battery storage; by 2033, new analysis projects are expected to jump to around 346 GWh, with 92–102 GWh of projects already in the pipeline and 69 new tenders floated in just the last year. In 2026, BESS is rapidly becoming the “missing link” that makes a high‑renewable, 24x7 reliable power system actually work.

India has already surpassed 250 GW of installed renewable capacity and is targeting 500 GW of non‑fossil capacity by 2030. Solar and wind are now the cheapest new sources of bulk power, but they come with a basic problem: they don’t always generate when India needs electricity most.

Solar peaks in the middle of the day and vanishes after sunset; wind is seasonal and often strongest at night or in specific regions. This mismatch between when renewables generate and when homes, factories, metros, and data centres want power creates challenges:

Midday surpluses that can force curtailment of solar.

Sharp evening peaks when demand spikes but solar is gone.

Frequency and voltage fluctuations if variable power swings quickly.

Studies estimate that India may need between 41 GW/208 GWh and 61 GW/230+ GWh of storage by 2030 to back its 500 GW clean power goal and ensure grid stability. The Central Electricity Authority and other analyses suggest that batteries and pumped hydro together will be essential to balance the system.

Without storage, India either wastes cheap renewable power or keeps leaning on coal and gas plants as expensive, polluting balancing tools. That is exactly where BESS steps in.

A Battery Energy Storage System is essentially a big, grid‑connected rechargeable battery. Unlike the small UPS in your home, these are containerized or building‑scale systems, often made up of thousands of lithium‑ion (or similar) cells, plus inverters, transformers, cooling and control systems.

BESS does three simple things:

Charge: It absorbs electricity from the grid or from a solar/wind plant when power is cheap or surplus.

Store: It holds that energy for a few minutes to a few hours.

Discharge: It feeds power back when the grid needs it typically when demand is high or renewables dip.

In practice, grid‑scale BESS in India is being used (or planned) for:

Peak shaving: Charging at night or during solar surplus, discharging during evening peaks.

Renewable integration: Smoothing out solar/wind output and enabling “round‑the‑clock” or “peak power” tenders.

Frequency regulation: Providing very fast response (seconds or milliseconds) to keep grid frequency stable.

Backup for critical loads: Supporting data centres, metros, and industrial clusters during outages.

India’s early BESS market was dominated by small UPS and lead‑acid systems. From 2025 onwards, it has shifted sharply towards lithium‑ion based, grid‑scale projects and large industrial applications. Industry estimates say installed battery storage could jump from around 200 MWh in 2025 to roughly 5 GWh by the end of 2026, a nearly tenfold increase.

Multiple reports agree that 2026 is a breakout year for energy storage in India. A new whitepaper cited by PV Magazine India notes that cumulative installed stationary BESS is still under 1 GWh today, but the project pipeline already exceeds 92 GWh, with 69 new BESS tenders totaling 102 GWh issued over the past year alone.

On the policy and tender side, a few big moves stand out:

The Union Budget provided Viability Gap Funding (VGF) support for up to 4 GWh of standalone BESS, directly subsidizing capex for early projects.

SECI has launched multiple tenders combining solar with storage, as well as standalone BESS projects. Examples include:

A 150 MW/500 MWh standalone BESS tender in Kerala with up to 40% VGF support.

A 10 MW solar + 10 MW/20 MWh BESS project in Odisha, also under VGF‑based competitive bidding.

Hybrid and FDRE (firm, dispatchable renewable energy) tenders pairing gigawatts of solar with multi‑GWh storage.

The Ministry of New and Renewable Energy (MNRE) introduced an Energy Storage Obligation (ESO), requiring distribution companies to procure a minimum share of their power from storage‑backed resources rising gradually from 1% in FY24 to 4% by FY30.

On the commercial side, the India Energy Storage Alliance and market research firms estimate:

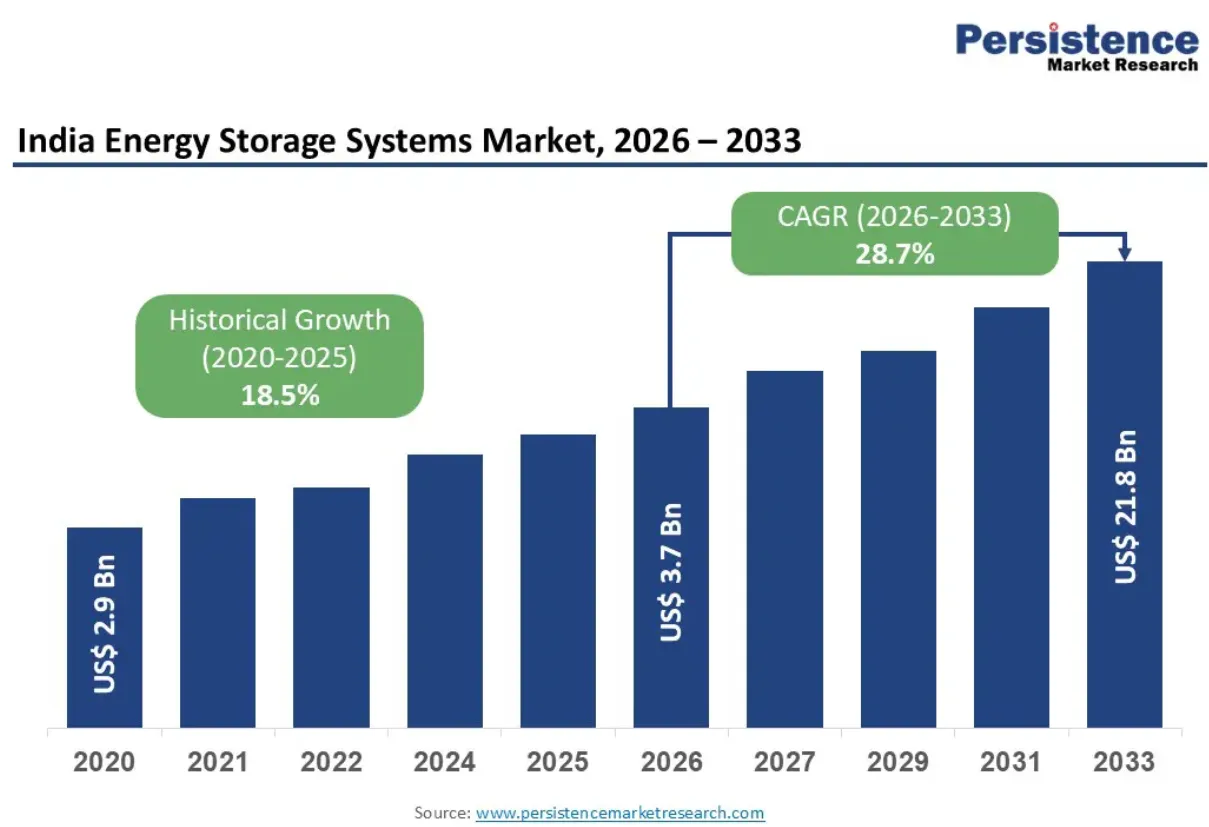

India’s overall energy storage systems market could be worth about USD 3.7 billion in 2026 and around USD 21–22 billion by 2033.

The BESS‑specific market grew to roughly USD 327–400 million by 2025 and is projected to reach USD 2.7 billion by 2034, at a CAGR of around 25%.

Wider BESS market value (including grid, C&I, and other applications) is expected to hit roughly USD 20 billion by 2035, growing at 29%+ annually.

One whitepaper projects India’s cumulative installed battery storage capacity could soar to about 346 GWh by 2033, from less than 1 GWh today. To put that in context, studies suggest India will need something like 230–336 GWh of storage by 2030–32 to integrate its renewables safely, so current tenders are finally starting to match what the grid actually needs.

In simple terms, battery storage fixes three chronic pain points in India’s power system:

Solar and wind have driven down daytime and bulk power prices, but they can’t guarantee electricity at 7 p.m. on a windless evening. BESS lets a solar plant store noon‑time energy and deliver it in the evening, converting “as‑available” renewable energy into a firm, dispatchable resource.

That’s why SECI’s latest tenders increasingly talk about:

“Round‑the‑clock renewable power” (RTC).

“Peak power” blocks backed by storage.

Firm and flexible renewable energy, instead of just MW installed.

Without storage, discoms are forced to keep coal plants spinning for backup, even if they are running inefficiently just to be available for peaks. With storage, they can rely more on renewables, reduce curtailment, and still meet evening and morning peaks.

As renewables reach higher shares, grids get more sensitive to sudden changes: a cloud bank can drop solar output sharply, or a wind lull can reduce generation in a region. BESS reacts much faster than thermal plants often in less than a second to inject or absorb power and keep frequency within safe limits.

Aspect | Without BESS | With BESS |

Midday solar surplus | Often curtailed (wasted) | Stored for evening demand |

Evening peak | Met by coal/gas | Partly met by stored solar/wind |

RE share in mix | Hard‑capped by grid limits | Can rise significantly |

Coal plant role | Baseload + peaker | More flexible, less peaker dependence |

This makes BESS valuable for:

Frequency regulation and ancillary services.

Voltage support and congestion management.

Black start support in case of major outages.

India’s National Electricity Plan and other studies explicitly highlight battery storage as a critical tool for grid reliability as the country steps up renewable penetration.

On the demand side, India is also adding new types of loads:

EV fast‑charging corridors along highways.

Large hyperscale data centres in cities like Mumbai, Chennai, Hyderabad and Noida.

Electrolyzers for green hydrogen production.

Many of these loads are peaky and sensitive to power quality. BESS can be installed at substations, industrial parks, or even behind the meter to shave peaks, ensure clean, uninterrupted supply, and reduce stress on distribution networks.

In short, batteries tie together intermittent generation, stressed grids, and new kinds of power‑hungry consumers hence the “missing link” label.

Despite the booming tender pipeline, India’s BESS roll‑out faces challenges.

Even though lithium‑ion prices have fallen globally, grid‑scale BESS still requires heavy upfront capex. Without VGF or clever tariff structures, early projects can look expensive compared to coal peakers or simple solar.

The government has tried to bridge this gap via:

VGF for 4 GWh of standalone BESS.

Production‑linked incentives (PLI) for advanced cell manufacturing to localize and reduce costs.

Factor | BESS Today | Coal/Gas Peakers |

Capex | High upfront | Lower per MW but fuel‑intensive |

Operating cost | Low variable cost (no fuel) | High fuel cost (coal/gas) |

Response speed | Very fast (seconds) | Slower |

Emissions | Zero at point of use | High CO₂ and local pollution |

Tariff familiarity | New, evolving frameworks | Well understood |

But discoms and regulators still need comfort on how to value storage correctly both for energy (MWh) and power (MW), and for services like frequency support. Tariff frameworks are evolving, but not yet uniform across states.

Storage is not just “generation” or “load”. It behaves as both. That makes it tricky to slot into existing rules on:

Open access.

Grid charges.

Transmission and distribution losses.

Scheduling and dispatch.

If regulations treat storage as both a generator and a consumer and double‑charge it on grid fees, economics suffer. Many stakeholders are working with regulators to ensure a fair framework that encourages, rather than penalizes, storage adoption.

Most grid‑scale projects today are based on lithium‑ion chemistries. There are questions around:

Degradation over time: How many cycles can a system deliver before useful capacity drops?

Safety and thermal management: How to prevent and manage fire risks at multi‑MWh scale?

Recycling and second life: What happens to cells at the end of their first life?

India is also exploring alternatives like sodium‑ion and flow batteries, but lithium‑ion dominates in the near term. Scaling up domestic cell and pack manufacturing, plus a robust recycling ecosystem, will be important to avoid simply swapping fuel import dependence for battery import dependence.

For companies, investors, and even policymakers, BESS opens several opportunity buckets across the value chain.

On the utility side, there is a surge in tenders for:

Standalone grid‑scale BESS providing peak power and ancillary services (like SECI’s Kerala project).

Solar + storage hybrids under central and state schemes (e.g., the Odisha 10 MW + 20 MWh project).

Pumped storage plants (PSP) at multi‑GWh scales, often tendered alongside battery projects as complementary technologies.

On the commercial and industrial (C&I) side, large energy users data centres, IT parks, metro rail, EV charging operators are beginning to look behind‑the‑meter or distribution‑connected BESS to manage peak demand, improve power quality, and enable higher renewable use. Many will combine rooftop or open‑access solar with storage to reduce grid dependence and hedge tariffs.

Upstream, the opportunity lies in:

Cell manufacturing under PLI schemes.

Pack integration, inverters, and power electronics.

Energy management software, forecasting, and optimization tools.

Downstream, there is room for innovative business models: storage‑as‑a‑service, shared neighbourhood batteries, or aggregator models where one player bids multiple small BESS assets into grid services markets.

Segment | Role for BESS | Who Benefits |

Grid‑scale | Peak shaving, ancillary services | Discoms, system operators |

RE developers | Firm, dispatchable renewable supply | IPPs, utilities |

C&I consumers | Lower peak charges, better reliability | Data centres, metros, factories |

Manufacturing | Cells, packs, inverters | Battery OEMs, EPCs, PLI beneficiaries |

Software/Services | Optimisation, aggregation | Tech firms, aggregators |

Looking ahead, the trajectory is clear even if the exact numbers vary by study. India’s storage requirement ranges from around 200–400 GWh by early 2030s to make its 500 GW clean power target deliver reliable electricity. Current projections of 346 GWh installed BESS by 2033 suggest that, for once, planning and market reality might actually converge.

By 2030:

Coal will still be in the mix but will increasingly act as a flexible resource rather than inflexible baseload.

Pumped hydro and BESS will together provide backbone balancing.

Solar, wind, and hybrid projects with storage will be standard in the procurement mix.

Data centres, EV corridors, and industrial clusters will use BESS not just for backup, but as active tools to manage energy costs and emissions.

By 2035, if India hits a USD 20 billion BESS market and moves towards several hundred GWh of installed battery storage, storage will no longer be a niche add‑on; it will be as fundamental as transmission lines or substations.

In that sense, Battery Energy Storage Systems are not just another clean‑tech trend. They are the critical missing link that turns India’s massive renewable build‑out into a truly modern, flexible, and resilient power ecosystem keeping the lights on, the grid stable, and the economy powered, even when the sun isn’t shining and the wind isn’t blowing.

Discover investment portfolios that are designed for maximum returns at low risk.

Learn how we choose the right asset mix for your risk profile across all market conditions.

Get weekly market insights and facts right in your inbox

It depicts the actual and verifiable returns generated by the portfolios of SEBI registered entities. Live performance does not include any backtested data or claim and does not guarantee future returns.

By proceeding, you understand that investments are subjected to market risks and agree that returns shown on the platform were not used as an advertisement or promotion to influence your investment decisions.

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Skip Password

By signing up, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with Password →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Log in with OTP →

By logging in, you agree to our Terms and Privacy Policy

"I was drawn to Wright Research due to its multi-factor approach. Their Balanced MFT is an excellent product."

By Prashant Sharma

CTO, Zydus

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

Answer these questions to get a personalized portfolio or skip to see trending portfolios.

(You can choose multiple options)

Investor Profile Score

We've tailored Portfolio Management services for your profile.

View Recommended Portfolios Restart