Asset Allocation is one of the most important tools to fight volatility.

It's like a recipe where you mix different ingredients in the right proportions to create a dish that's both tasty and healthy or like managing a cricket team where you need a healthy mix of batsmen like Virendra Sehwag with a patient one like Rahul Dravid to build a strong team.

The right asset allocation not only reduces the risk in our portfolios but also wins over a non-diversified portfolio in terms of returns in the long term.

Let’s understand the Wright way to asset allocation in this post.

Asset Allocation at Wright

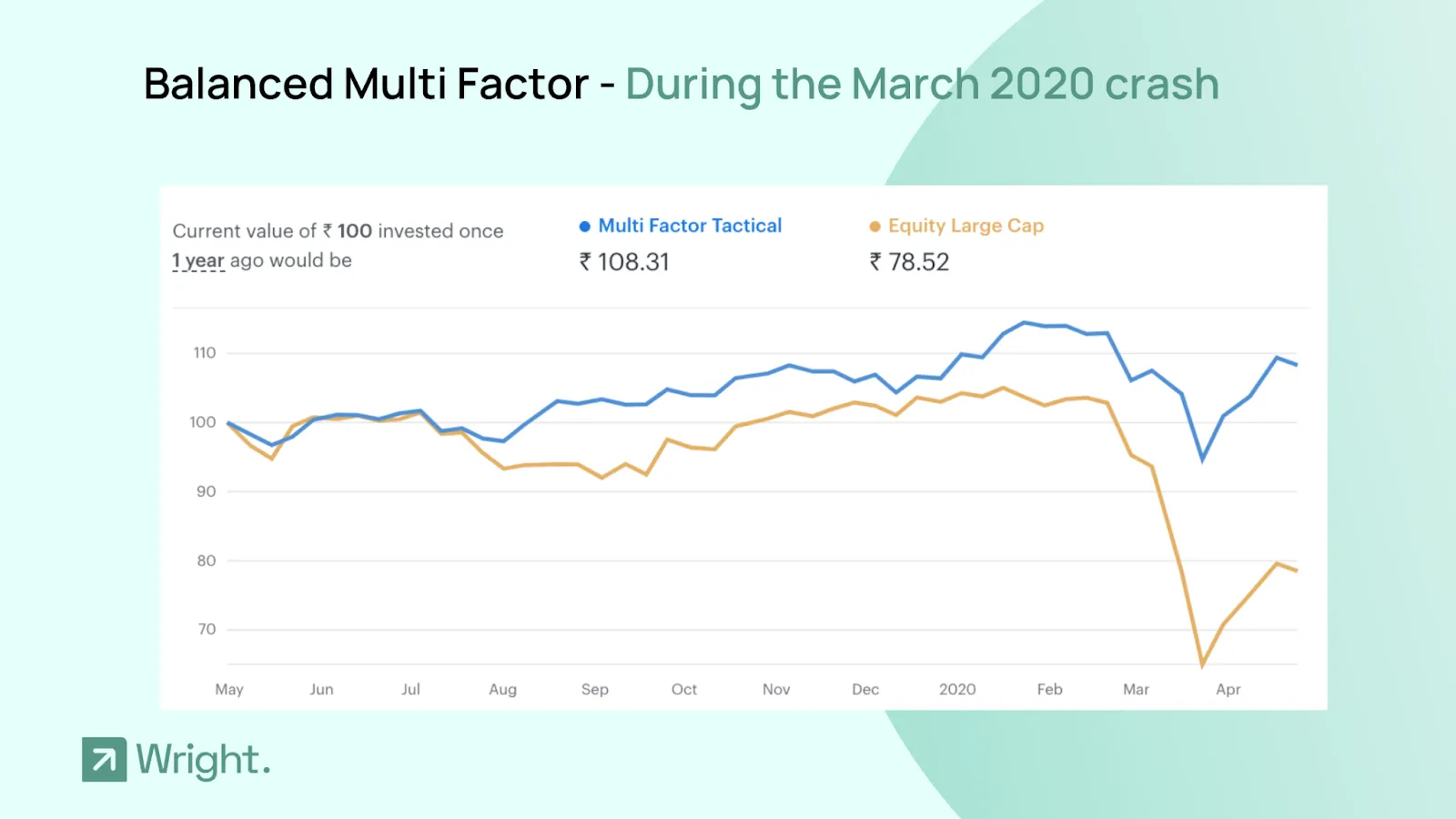

Before people knew us for Wright Momentum, people knew Wright due to our robust Asset Allocation during the 2020 Covid crash. Yes, that’s right!

When the market crashed 35%, our Balanced Multi-Factor, the flagship portfolio, only saw a drawdown of 15% and therefore built up a significant outperformance. This was the first instance when people recognised our philosophy, and while we thought that the March 2020 crash would decimate the then 8-month-old Wright, we saw our user base grow multifold in light of the crash! It was one of the moments that instilled the confidence to survive for team Wright.

Obviously, we did not do any magic to outperform. It was all the benefits of tactical asset allocation. Our portfolios has high bond and gold allocation even before the crisis and as the markets dipped we deallocated further to save up on the risk.

Regime Modeling for Asset Allocation

“The market does not stay the same all the time” - Wright Research, from the moment we started. And the different phases of the market are called market regimes.

One of the favourite areas of research that we are always tinkering with is Regime modelling. Market regimes refer to different periods when the market behaves in distinct ways due to changes in economic, political, or other factors. By understanding these different regimes, investors can make more informed decisions about allocating their assets and managing risk.

The underlying decision maker for our allocation models is a machine learning-driven predictive model that forecasts the regimes in the market.

Here are the predictions on the market regime that our regime model has made since 2018.

The average daily market return in the phases where we have forecasted the market to be bullish is 0.06% and in the bearish phases it is -0.01%. This hints at strength of the predictions made by the model.

In our Balanced Multi-Factor model, we tactically shift allocation to less volatile factors and bond and gold ETFs when the market regimes look bearish and we shift back to more risky and high performing equity factors when the markets are bullish.

In our momentum model as well we shift allocation to less volatile momentum factors when markets are risky and we shift to more aggressive ones when market is bullish. Same goes for our smallcaps, innovation and new-india models as well.

Deallocation Policy

The markets can actually go through deep corrections also, At Wright Research we handle the risk in investing using a methodology called systematic deallocation. What that means in simple words is that we reduce the stocks in the portfolio by selling a certain percentage and buying liquid ETF instead.

It's quite simple.

Deallocate 10% of the portfolio to liquidbees if there is a 10% drawdown in the short term (a month or so). If there is 10% more drawdown, deallocate 10% more and so on.

Once the portfolio recovers from this short term drawdown - reallocate in a similar fashion

Also, like all markets are not the same, similarly all drawdowns are not the same. A drawdown in a high risk environment is more lethal than one in a low risk environment. So we deallocate more aggressively when we see high risk.

This is how the deallocation policy looks in action. There are not deallocation triggers in any of our portfolios at the moment.

Ideal Asset Allocation

The latest balanced multi-factor portfolio has allocations to stocks that have strong management quality and exposure to North American markets. Our portfolio also has sizable gold allocation and some bond exposure. We would see the allocations suitable for bearish markets continue in the upcoming period as well.

How to Invest in Asset Allocation by Wright?

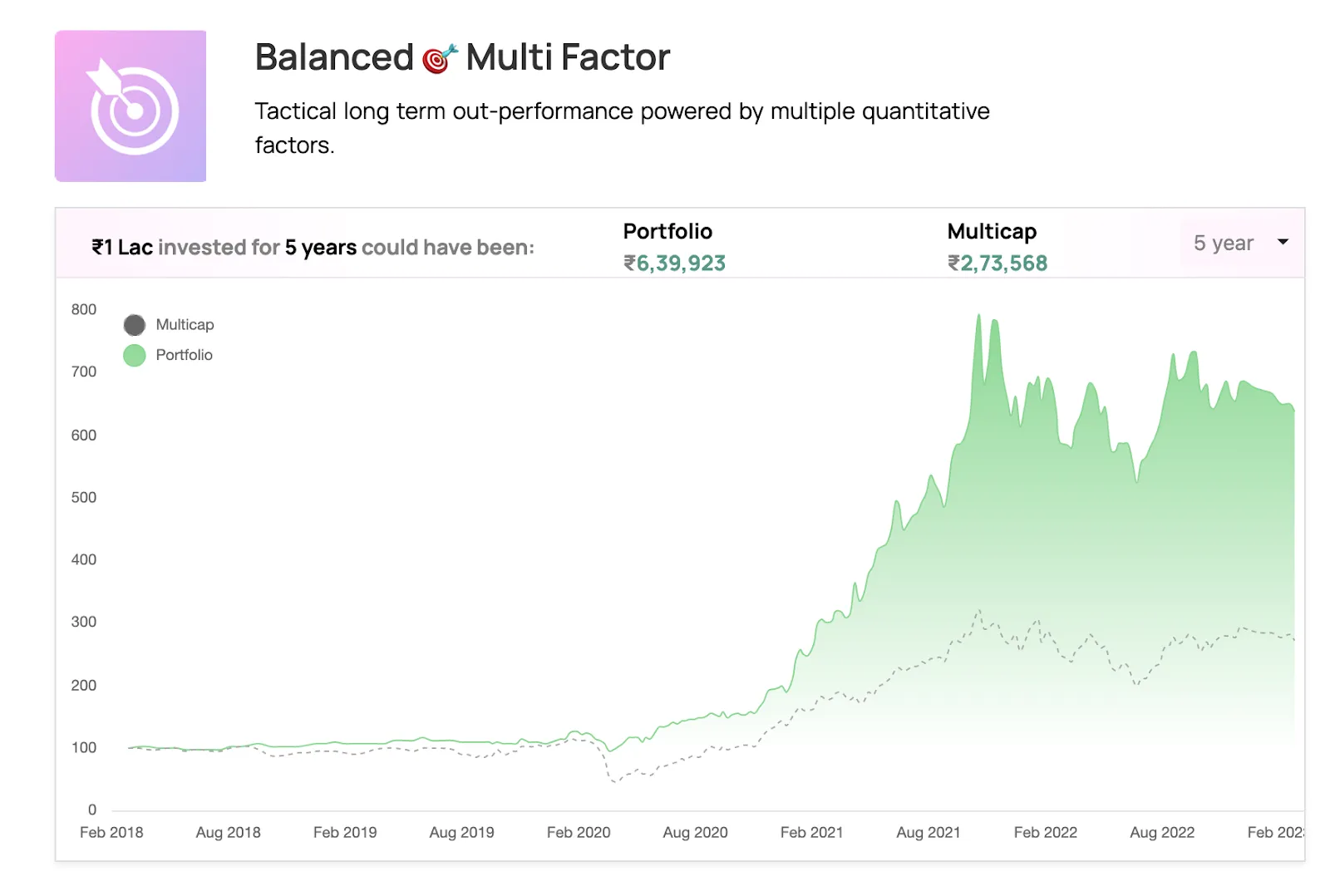

Check out the Balanced Multi Factor strategy, this strategy is a moderate risk strategy which aims to outperform in all stages of the market cycle using dynamic allocation to various factors and asset classes based on the changing market regime.

About the author

Our Investment Philosophy

Learn how we choose the right asset mix for your risk profile across all market conditions.

Subscribe to our Newsletter

Get weekly market insights and facts right in your inbox